Sorry for my painting skills, I will try to give you the following intuition.

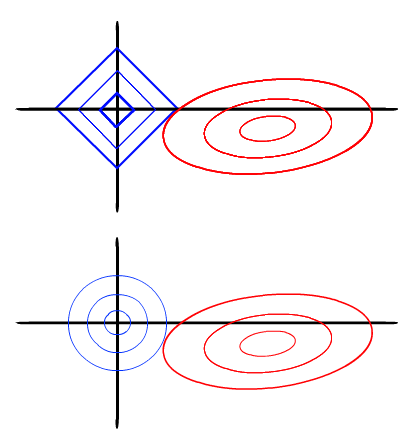

Let $f(\beta)$ be the objective function (for example, MSE in case of regression). Let's imagine the contour plot of this function in red (of course we paint it in the space of $\beta$, here for simplicity $\beta_1$ and $\beta_2$).

There is a minimum of this function, in the middle of the red circles. And this minimum gives us the non-penalized solution.

Now we add different objective $g(\beta)$ which contour plot is given in blue. Either LASSO regularizer or ridge regression regularizer. For LASSO $g(\beta) = \lambda (|\beta_1| + |\beta_2|)$, for ridge regression $g(\beta) = \lambda (\beta_1^2 + \beta_2^2)$ ($\lambda$ is a penalization parameter). Contour plots shows the area at which the function have the fixed values. So the larger $\lambda$ - the faster $g(x)$ growth, and the more "narrow" the contour plot is.

Now we have to find the minimum of the sum of this two objectives: $f(\beta) + g(\beta)$. And this is achieved when two contour plots meet each other.

The larger penalty, the "more narrow" blue contours we get, and then the plots meet each other in a point closer to zero. An vise-versa: the smaller the penalty, the contours expand, and the intersection of blue and red plots comes closer to the center of the red circle (non-penalized solution).

And now follows an interesting thing that greatly explains to me the difference between ridge regression and LASSO: in case of LASSO two contour plots will probably meet where the corner of regularizer is ($\beta_1 = 0$ or $\beta_2 = 0$). In case of ridge regression that is almost never the case.

That's why LASSO gives us sparse solution, making some of parameters exactly equal $0$.

Hope that will explain some intuition about how penalized regression works in the space of parameters.