P.S. Now I'm trying to write the JAGS code and any help would be much appreciated! ( http://stackoverflow.com/questions/40528715/runtime-error-in-jagshttps://stackoverflow.com/questions/40528715/runtime-error-in-jags )

I found a reference which answered my question: https://arxiv.org/pdf/1405.3738.pdf.

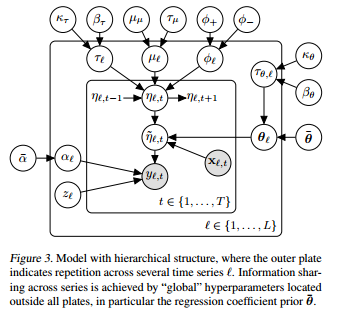

The model is quite complicated, here is the state space representation:

So, let's say I have L different products I'm studying across 1,..,T time periods.

$Y_{l,t} \sim z*\delta_0 + (1-z)NB(exp(\widetilde{\eta}_{l,t}),alpha_l)$ is the distribution for product l at time t

$\widetilde{\eta}_{l,t} = \eta_{l,t} + X_{l,t}\theta_l$ this is the Log of the mean of product l sales at time t, guaranteeing that it is positive.

$\eta_{l,t} = \mu_l + \phi_l(\eta_{l,t-1}-\mu) + \epsilon_{l,t}$

$\epsilon_{l,t} \sim N(0,\frac{1}{\tau_l})$

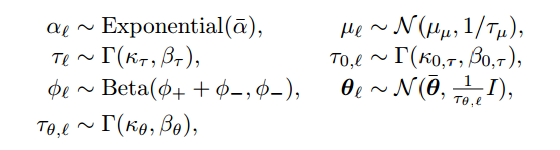

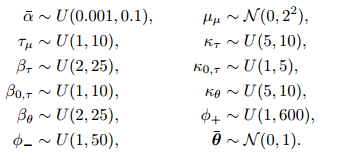

The other priors and hyperpriors are in the next images:

P.S. Now I'm trying to write the JAGS code and any help would be much appreciated! ( http://stackoverflow.com/questions/40528715/runtime-error-in-jags )

I found a reference which answered my question: https://arxiv.org/pdf/1405.3738.pdf.

The model is quite complicated, here is the state space representation:

So, let's say I have L different products I'm studying across 1,..,T time periods.

$Y_{l,t} \sim z*\delta_0 + (1-z)NB(exp(\widetilde{\eta}_{l,t}),alpha_l)$ is the distribution for product l at time t

$\widetilde{\eta}_{l,t} = \eta_{l,t} + X_{l,t}\theta_l$ this is the Log of the mean of product l sales at time t, guaranteeing that it is positive.

$\eta_{l,t} = \mu_l + \phi_l(\eta_{l,t-1}-\mu) + \epsilon_{l,t}$

$\epsilon_{l,t} \sim N(0,\frac{1}{\tau_l})$

The other priors and hyperpriors are in the next images:

P.S. Now I'm trying to write the JAGS code and any help would be much appreciated!

I found a reference which answered my question: https://arxiv.org/pdf/1405.3738.pdf.

The model is quite complicated, here is the state space representation:

So, let's say I have L different products I'm studying across 1,..,T time periods.

$Y_{l,t} \sim z*\delta_0 + (1-z)NB(exp(\widetilde{\eta}_{l,t}),alpha_l)$ is the distribution for product l at time t

$\widetilde{\eta}_{l,t} = \eta_{l,t} + X_{l,t}\theta_l$ this is the Log of the mean of product l sales at time t, guaranteeing that it is positive.

$\eta_{l,t} = \mu_l + \phi_l(\eta_{l,t-1}-\mu) + \epsilon_{l,t}$

$\epsilon_{l,t} \sim N(0,\frac{1}{\tau_l})$

The other priors and hyperpriors are in the next images:

P.S. Now I'm trying to write the JAGS code and any help would be much appreciated! ( http://stackoverflow.com/questions/40528715/runtime-error-in-jags )