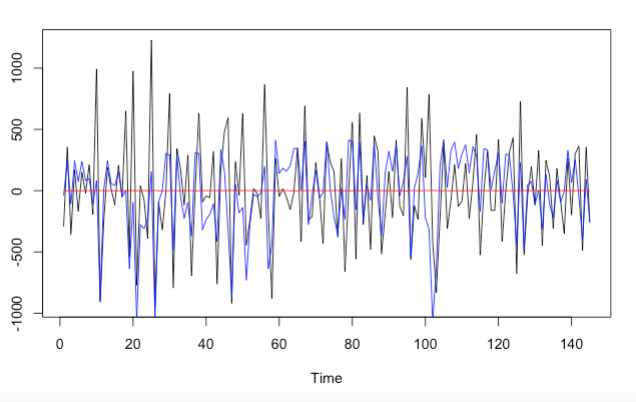

I am doing a rolling window out-of-sample forecast and have fitted an ARIMA(0,0,1) model to a first difference time series. People argue that sometimes simpler models are better than more complicated oncePeople argue that sometimes simpler models are better than more complicated ones and therefore I should try to fit a ARIMA(0,0,0) model with non-constant mean (the intercept) to the same differenced series. But the outcome of the arima (0,0,0) is so bad and I dont understand why? (see picture, blue line = ARIMA(0,0,1) and red line = ARIMA(0,0,0))

Why do not the mean in ARIMA(0,0,0) get updated with the rolling window? Or does that depend on the training set size?(80% training data and 20% test data on 727 observations)

Is it a general thing that an ARIMA(0,0,0) becomes a MA(1) when the series is differenced? I have some signs of that

How do you know if a coefficient is significant (ARIMA) when doing rolling window forecast and the training set gets updated all the time?

Thanks