library(ggplot2)

set.seed(2023)

N <- 1000

R <- 10000

p <- rep(NA, R)

for (i in 1:R){

x <- rnorm(N) # Simulate the distribution

p[i] <- t.test(x, mu = 0)$p.value # Calculate the t-test p-value

}

d0 <- data.frame(

p_value = p,

CDF = ecdf(p)(p),

Distribution = "p-value Distribution"

)

d1 <- data.frame(

p_value = p,

CDF = qunif(p, 0, 1),

Distribution = "U(0,1) Distribution"

)

d <- rbind(d0, d1)

ggplot(d, aes(x = p_value, y = CDF, col = Distribution)) +

geom_line() +

theme(legend.position="bottom")

library(ggplot2)

set.seed(2023)

N <- 1000

R <- 10000

p <- rep(NA, R)

for (i in 1:R){

x <- rnorm(N) # Simulate the distribution

p[i] <- t.test(x, mu = 0)$p.value # Calculate the t-test p-value

}

d0 <- data.frame(

p_value = p,

CDF = ecdf(p)(p),

Distribution = "p-value Distribution"

)

d1 <- data.frame(

p_value = p,

CDF = qunif(p, 0, 1),

Distribution = "U(0,1) Distribution"

)

d <- rbind(d0, d1)

ggplot(d, aes(x = p_value, y = CDF, col = Distribution)) +

geom_line() +

theme(legend.position="bottom")

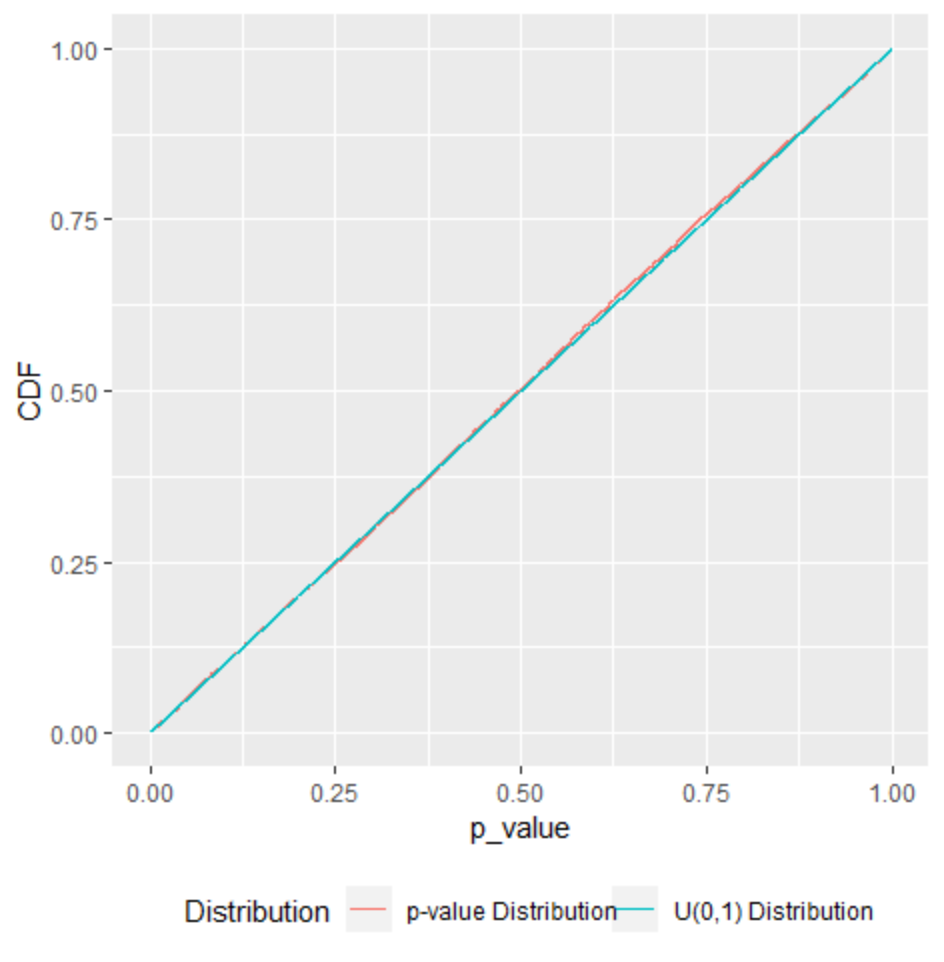

In general, for a $U(0,1)$ distribution, if $0\le\alpha\le 1$, $P(p\le\alpha)=\alpha$. That's really the defining characteristic of the $U(0,1)$ distribution. In that sense, by picking the $\alpha$-level for the test, you pick your tolerance for rejecting when the null hypothesis is true.

However, note that rejecting in this case is a mistake. By the simulation, the null hypothesis is correct, and rejecting the null hypothesis is a so-called type I error. Errors are bad, and we like to minimize them. Consequently, it is typical to set $\alpha$ low, often around $0.05$ or lower, in order to keep from having a bunch of false positives.

You can take it it to the extreme to see why we don't want a high $\alpha$-level: if you set $\alpha = 1$, your test always rejects. Is a rejection from a statistical hypothesis test that always rejects, no matter what, real evidence of a scientific (economic, whatever) discovery? I say it is not. That is equivalent to the function below that makes absolutely no use of the data.

worthless.test <- function(input_data){

print("Reject the null hypothesis!")

}