Explaining The Problem

Important question in data analysis is testing observed relationships for confounding factors. Partial Correlation is a metric designed to do specifically that. The general idea is as follows. If random variables $X$ and $Y$ are correlated, but that correlation is linearly explained by another random variable $Z$, the the partial correlation between $X$ and $Y$ conditioned on $Z$, namely, $PCorr[X,Y|Z]$ should be small. More precisely, it is my intuition that partial correlation assumes the following underlying interaction model

$$X = \alpha_x Z + \nu_x$$

$$Y = \alpha_y Z + \nu_y$$

where $\alpha$ and $\beta$ are some unknown coefficients, and $\nu_x$ and $\nu_y$ are some random variables unrelated $Z$, which can be interpreted as noise or unrelated effects within $X$ and $Y$. If $\nu_x$ and $\nu_y$ were 0, then we would observe 100% correlation, and no partial correlation.

However, in realistic scenarios it frequently happens that the estimate of the confounding variable itself is a noisy function of the true confounding variable. Frequently, the actual interaction model looks something like this

$$X = \alpha_x Z + \nu_x$$

$$Y = \alpha_y Z + \nu_y$$

$$Z' = \alpha_z Z + \nu_z$$

The researcher only has access to $X, Y$ and $Z'$ but not $Z$. I decided to test if partial correlation is useful at detecting conditional independence between $X$ and $Y$ in this scenario.

Simulation

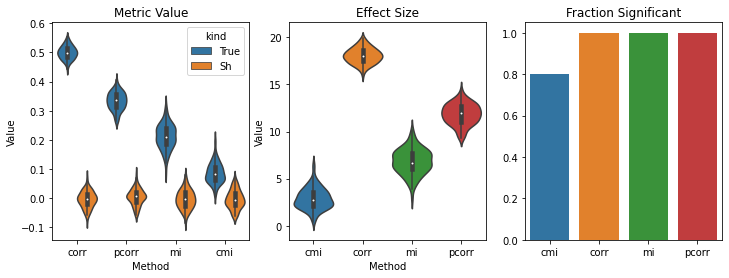

I ran a trivial simulation with $\alpha_x=\alpha_y=\alpha_z=1$, $X, Y, Z \sim \mathcal{N}(0,1)$ and $\nu_x, \nu_y, \nu_z \sim \mathcal{N}(0,1)$. I calculated correlation and partial correlation, as well as their non-linear extensions - mutual information (mi) and conditional mutual information (cmi).

I repeated the simulation 100 times, and used 1000 samples for each of the random variables $X$, $Y$ and $Z'$ for each simulation. For each simulation I computed 1 value of the metric for the simulated data, and one value for shuffled $Y$-values. The first plot shows the values of each metric for true and shuffled data - each violin is an empirical distribution over 100 points. For the second plot I estimated the effect size of each of the true datapoints using the mean and the variance of the shuffled datapoints. For the third plot, I approximated the fraction of simulations one would typically consider significant by counting the fraction of effect sizes above 2.

It is expected that correlation and mutual information would result in highly significant effects, since $X$ is indeed correlated to $Y$. However, it is unexpected (at least to me) that partial correlation and conditional mutual information are still very significant, even though their effect sizes are lower than those of correlation and mutual information respectively.

My Questions:

- Is this behaviour expected? Most literature I have seen on partial correlation does not explicitly mention that the conditional variable is not allowed to be noisy (please correct me if I'm wrong).

- Why does this happen? Can PCorr or CMI deal with this scenario at least asymptotically?

- Is the problem of discriminating between true and conditional linear dependence asymptotically solvable at all?

Jupyter notebook of the calculation is available, I will find a way to share it if there is demand

Edit 1: Theoretical Analysis

I have just performed the theoretical analysis for the noisy model, and it seems that indeed it behaves really badly even in the asymptotic case.

Residual is a linear fit of variable $Z'$ to variable $X$, namely $$X_{res} = X + kZ'$$ for some constant $k$, typically obtained using linear regression.

Partial correlation is the normalized covariance between $X_{res}$ and $Y$. We can calculate this covariance. For simplicity assume that all random variables have zero mean.

$$ \begin{eqnarray} Cov(X_{res}, Y) &=& \langle (X + kZ) Y \rangle \\ &=& \langle (\alpha_x Z + \nu_x + k(\alpha_z Z + \nu_z)) (\alpha_y Z + \nu_y) \rangle \\ &=& \langle ( (\alpha_x + k \alpha_z) Z + \nu_x + k\nu_z) (\alpha_y Z + \nu_y) \rangle \\ &=& \alpha_y (\alpha_x + k \alpha_z) Var(Z) + Cov(\nu_x, \nu_y) + kCov(\nu_z, \nu_y) \end{eqnarray} $$

Naively, we would have expected only the 2nd term in this equation, namely, the covariance between the parts of $X$ and $Y$ that are independent of $Z$. This indeed would be the case if $\nu_z$ was zero. However, we are interested to estimate what is the impact of non-zero $\nu_z$ on our estimate. There are two glaring problems. Firstly, as soon as $k$ is something different from zero, the partial correlation gets contaminated by the third term - covariance between $\nu_y$ and $\nu_z$. This is logical - by fitting $Z'$ to $X$, we to some extent remove redundant commonalities between $X$ and $Y$, but instead contaminate result with commonalities between $X$ and $Z$ that weren't there before. The second problem is the actual value of $k$. Naively, we would expect that the linear regression would be able to find the coefficient $k = -\frac{\alpha_x}{\alpha_z}$. Instead, we can estimate the asymptotic value of $k$ by minimizing the expected variance

$$L^2(k) = \langle|X_{res}|\rangle = ... = Var(\nu_x) + k Var(\nu_y) + (\alpha_x + k \alpha_z)^2 Var(S)$$

MLE estimator of $k$ for this loss function (the quantity estimated by partial correlation) can be shown to be:

$$k_{MLE} = -\frac{Cov(\nu_x, \nu_z) + \alpha_x \alpha_z Var(Z)}{Var(\nu_z) + \alpha_x^2 Var(Z)}$$

Again, if $\nu_z = 0$, the asymptotic estimate for $k_{MLE}$ converges to the expected $k = -\frac{\alpha_x}{\alpha_z}$. However, in presence of noise in $Z'$ or unique correlants between $X$ and $Z'$ the linear regression estimate for the residual is further biased.

Conclusion:

Currently this looks very bad. Guaranteeing zero noise covariate is unfeasible in many cases. Any extra components in the covariate will likely cause partial correlation to spuriously report statistically significant result for a relationship between two variables controlled for the 3rd variable, when in reality the result is redundant over all three variables and should disappear when controlled for. Please tell me that this result is well-known and I just overlooked it. The ramifications of this on already existing experimental applications of partial correlations may be huge.