What would a bayesian do if she wanted to do inference for the mean with a large sample but has no idea of the underlying distributions?

A frequentist statitician would use the sample mean as a point estimate and CLT for the distribution of the estimator. All she has to assume is finite variance.

I have found Bernstein Von-Mises Theorem which states that given a random sample $X_1, \ldots, X_n$ and

- a prior $p(\mu)$ for the mean

- a distribution for the sample given the parameter $f_{x | \mu}$

Then if the sample size is sufficiently large the posterior distribution of the mean given the sample is approximately normal, i.e

$$ \mu_{|_{X_1, \ldots X_n}} \approx \mathcal{N}\left( \hat{\mu}_{ml}\, ; \, \frac{1}{I(\mu_0) n}\right)$$

Where the mean is the maximum likelihood estimator and $I(\mu_0)$ is Fisher information number for the true mean.

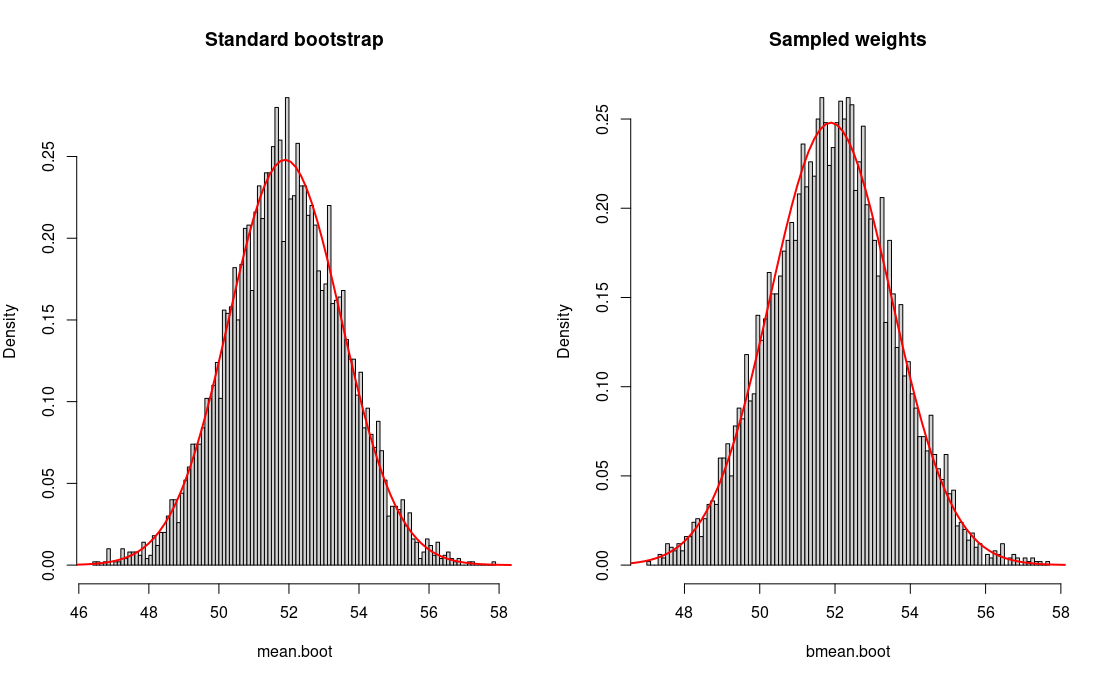

In the case where we have no knowledge of $f_{x | \mu}$ there is the problem that maximum likelihood nor fisher information number can be calculated. But what can be done? Becuase even if we do not know it the distribution exists and it will be approximately normal.

Intentions:

Some buisness woman has to take an action based on the true sign of the mean. A decision has to be made so she will use the sign of the sample mean but she needs some measure of the potential cost that arise in case of making the wrong decistion.

So, if the sample mean is positive things like

$$ P\left( \mu < 0 | X_1 \ldots X_n \right) = \int_{-\infty}^0 f_{\mu |x_1 \ldots x_n}( t) \, dt.$$ or

$$ E \left( \mu I_{(-\infty, 0)}| X_1 \ldots X_n \right) = \int_{-\infty}^0 t f_{\mu |x_1 \ldots x_n}( t) \, dt.$$

would make a lot of (buisness) sense for her.

In the frequentist context she is stuck with affirmations of the kind: With $95\%$ confidence the mean is greater than a certain value.