I want to see if I am on the right track analysing my ACF and PACF plots:

Background: (Reff: Philip Hans Franses, 1998)

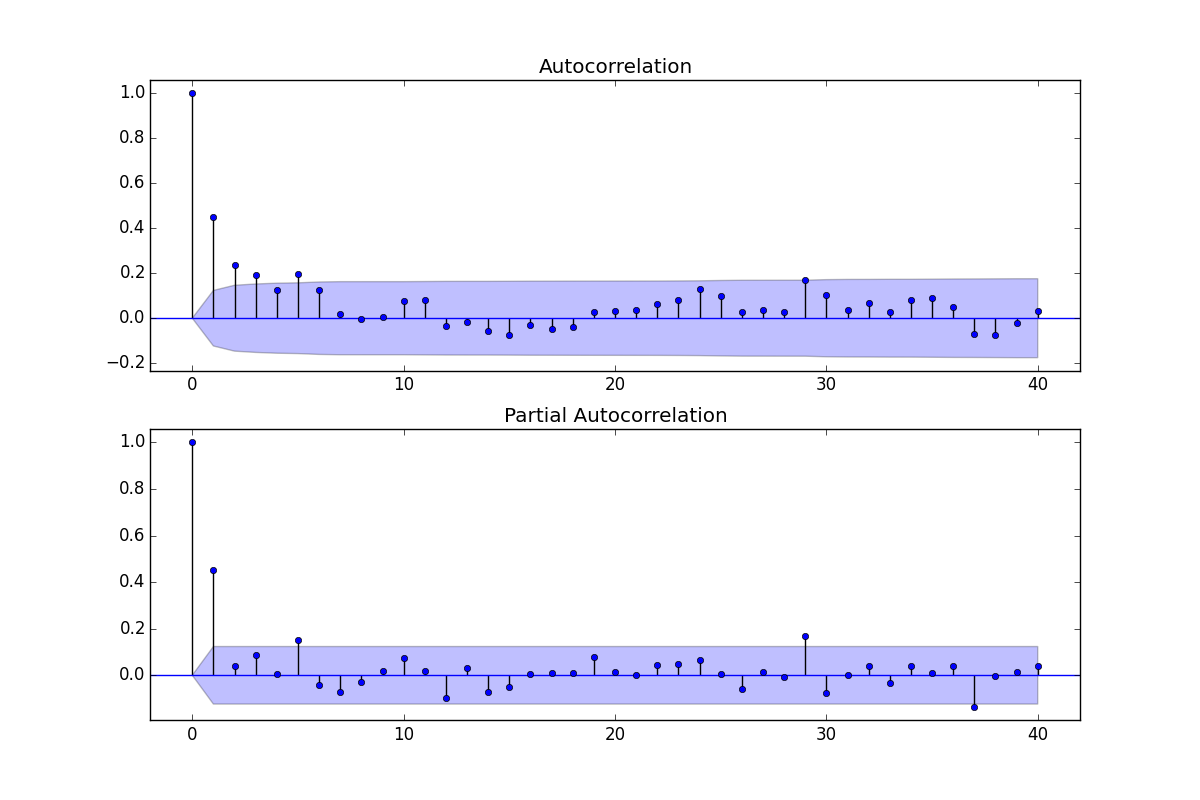

As both ACF and PACF show significant values, I assume that an ARMA-model will serve my needs

The ACF can be used to estimate the MA-part, i.e q-value, the PACF can be used to estimate the AR-part, i.e. p-value

To estimate a model-order I look at a.) whether the ACF values die out sufficiently, b.) whether the ACF signals overdifferencing and c.) whether the ACF and PACF show any significant and easily interpretable peaks at certain lags

ACF and PACF might suggest not only one model but many from which I need to choose after considering other diagnostic tools

Having that in mind, I would go ahead and say that the most obvious model seems to be ARMA (4,2) as ACF values die out at lag 4 and PACF shows spikes at 1 and 2.

Another way to analyze would be an ARMA(2,1) as I see two significant spikes in my PACF and one significant spike in my ACF (after which the values die out starting from a much lower point (0.4)).

Looking at my in-sample-forecast results (using a simple Mean Absolute Percentage Error) ARMA (2,1) delivers much better results then ARMA(4,2). So I use ARMA(2,1)!

Can you confirm my method and findings of analyzing ACF and PACF plots?

Help appreciated!

EDIT:

Descriptive Statistics:

count 252.000000

mean 29.576151

std 7.817171

min -0.920000

25% 26.877500

50% 30.910000

75% 34.915000

max 47.430000

Skewness of endog_var: [-1.35798399]

Kurtsosis of endog_var: [ 5.4917757]

Augmented Dickey-Fuller Test for endog_var: (-3.76140904255411, 0.0033277703768345287, {'5%': -2.8696473721448728, '1%': -3.4487489051519011, '10%': -2.5710891239349585}

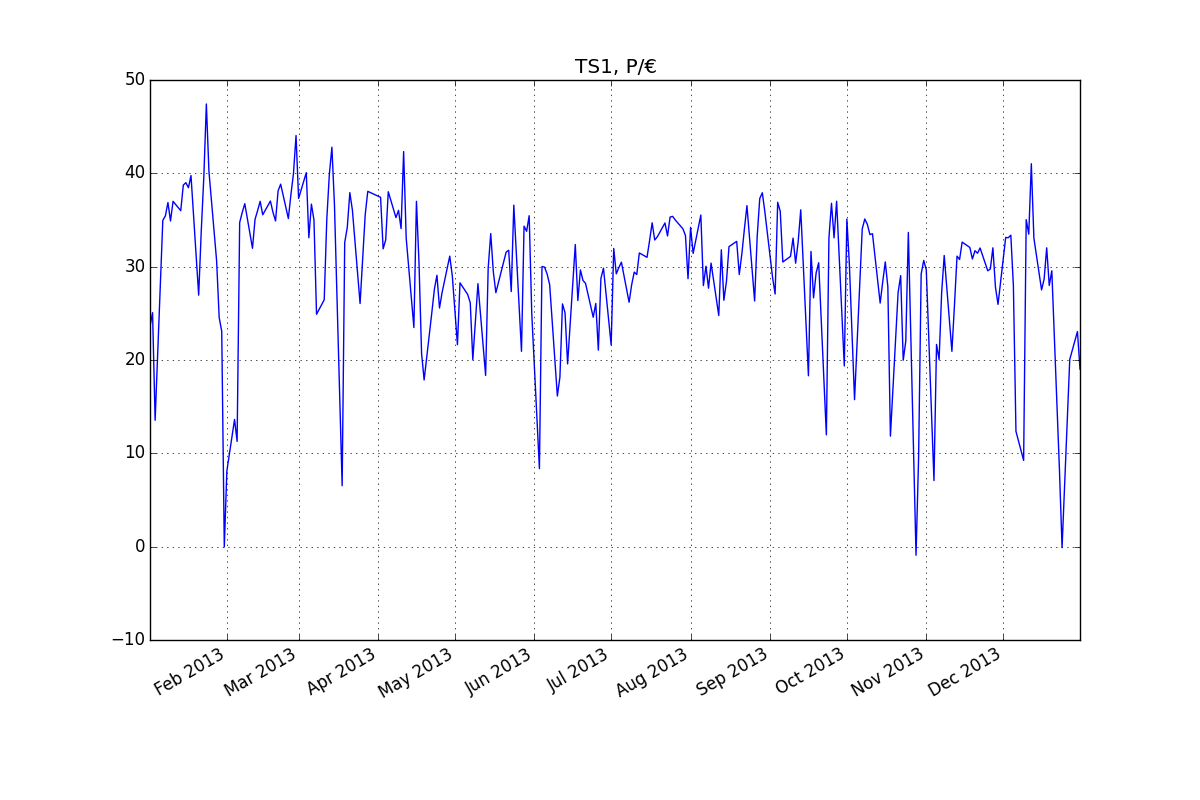

Time-Series:

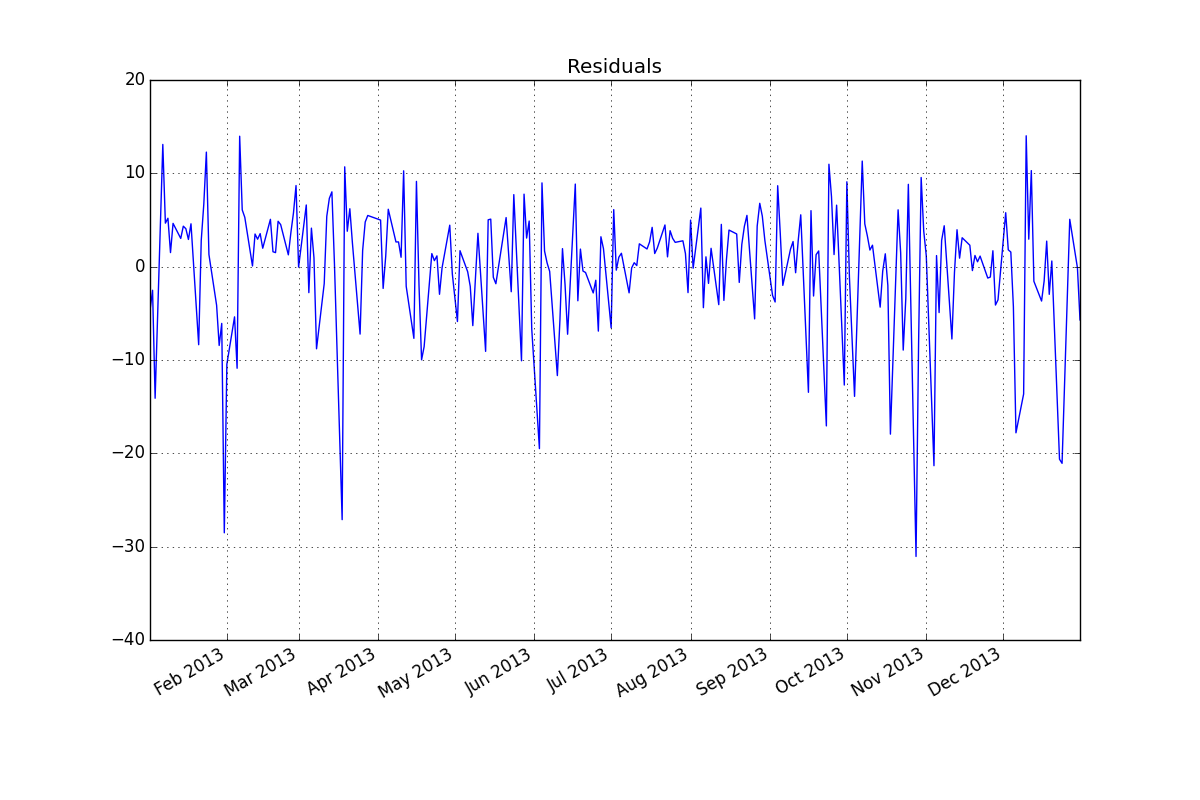

Residuals (ARMA (2,1):

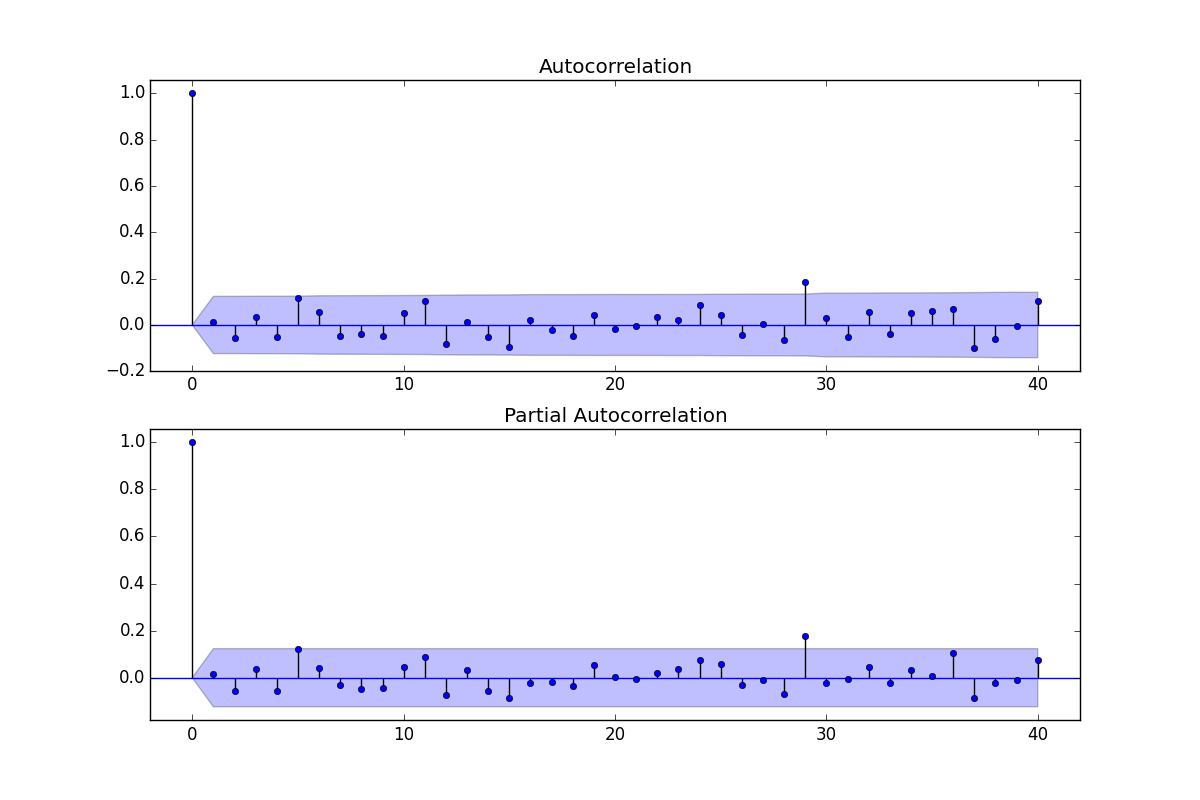

ACF/PACF of Residuals:

EDIT II:

Data:

14.37561

23.95561

25.41561

13.88561

23.31561

33.12561

35.30561

35.78561

37.21561

35.23561

37.34561

38.28561

39.03561

36.34561

39.08561

39.34561

38.80561

40.10561

34.13561

35.42561

27.29561

34.13561

39.89561

47.77561

40.57561

36.15561

33.66561

30.97561

24.90561

23.41561

0.31561

8.45561

37.36561

33.40561

13.97561

11.62561

35.07561

36.15561

37.09561

36.95561

37.85561

32.31561

35.41561

36.35561

37.34561

35.90561

37.40561

36.44561

37.37561

36.16561

35.24561

38.47561

39.18561

39.61561

29.55561

35.50561

38.05561

40.32561

44.39561

37.65561

46.27561

29.41561

40.41561

33.44561

37.04561

35.34561

25.24561

30.23561

15.40561

26.79561

35.38561

40.22561

43.14561

36.96561

41.93561

11.30561

6.87561

32.92561

34.54561

38.27561

36.40561

25.44561

37.26561

26.39561

31.13561

35.90561

38.41561

33.66561

33.16561

31.96561

30.34561

37.77561

32.25561

33.21561

38.37561

36.63561

40.78561

35.60561

36.37561

34.42561

42.67561

33.40561

31.49561

24.81561

23.82561

37.34561

30.73561

21.04561

18.20561

27.36561

18.49561

25.41561

27.92561

29.42561

25.91561

27.56561

28.69561

29.89561

31.47561

29.34561

25.35561

21.98561

28.61561

33.87561

20.07561

27.36561

26.48561

20.37561

22.33561

28.52561

21.24561

10.77561

18.69561

30.19561

33.89561

29.81561

27.55561

22.37561

20.32561

22.43561

31.89561

32.10561

27.67561

36.93561

36.51561

26.96561

21.27561

34.68561

34.13561

35.80561

25.38561

33.42561

9.28561

8.70561

30.36561

30.29561

29.56561

28.41561

33.40561

18.47561

16.48561

18.51561

26.35561

25.40561

19.92561

21.26561

10.90561

32.71561

26.71561

29.99561

28.87561

28.55561

14.07561

10.97561

24.92561

26.40561

21.40561

29.08561

30.18561

30.27561

16.15561

21.96561

32.29561

29.57561

30.24561

30.82561

28.83561

27.30561

26.53561

28.39561

29.76561

29.50561

31.81561

34.79561

24.14561

31.34561

33.14561

35.04561

33.20561

33.53561

35.28561

29.84561

35.02561

33.63561

35.65561

35.73561

35.35561

37.18561

27.38561

34.40561

33.69561

29.05561

34.55561

31.76561

30.91561

34.70561

35.87561

28.31561

30.39561

28.03561

30.72561

30.57561

23.93561

25.11561

32.15561

26.74561

28.76561

32.49561

34.79561

27.90561

33.05561

29.50561

31.67561

34.36561

36.88561

32.31561

26.24561

26.66561

33.59561

37.64561

38.26561

36.20561

33.27561

29.94561

29.19561

27.41561

37.24561

36.26561

30.84561

35.46561

32.24561

31.44561

33.40561

30.71561

33.03561

36.43561

33.44561

22.32561

18.65561

31.97561

27.00561

29.66561

30.76561

33.44561

29.19561

12.32561

33.41561

37.13561

33.43561

37.35561

40.17561

29.38561

19.70561

35.44561

30.48561

30.72561

16.09561

30.82561

30.55561

34.38561

35.45561

34.87561

33.78561

33.87561

29.83561

26.35561

26.44561

28.72561

30.85561

28.18561

12.18561

31.82561

18.01561

27.57561

29.38561

20.32561

22.36561

34.01561

34.40561

20.23561

-0.57439

9.87561

29.55561

31.01561

30.00561

28.12561

13.47561

7.42561

22.01561

20.38561

27.57561

31.54561

29.90561

16.40561

21.27561

26.22561

31.47561

31.11561

32.97561

32.34561

29.36561

32.40561

31.16561

32.05561

31.78561

32.34561

33.87561

31.80561

29.90561

30.09561

32.36561

28.15561

26.30561

15.32561

31.03561

33.47561

33.44561

33.71561

28.30561

12.70561

10.17561

43.96561

9.58561

35.38561

33.82561

41.37561

33.40561

33.64561

20.30561

27.85561

29.01561

32.36561

28.33561

29.90561

27.19561

0.39561

8.40561

0.24561

11.87561

29.15561

20.40561

0.42561

29.29561

23.39561

19.36561

. note that this had been a popular guess . The residuals from this model are plotted here

. note that this had been a popular guess . The residuals from this model are plotted here . There is a suggestion of variance hetero-scedasticity but this is a symptom and one needs to find the correct cure which we will ultimately find. Proceeding the acf of the residuals shown here

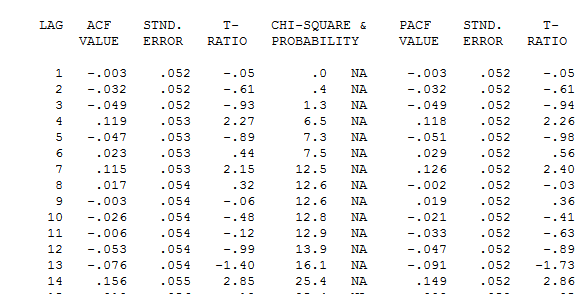

. There is a suggestion of variance hetero-scedasticity but this is a symptom and one needs to find the correct cure which we will ultimately find. Proceeding the acf of the residuals shown here  exhibits a suggestion of model inadequacy. A closer look at the table of the acf of the residuals is here

exhibits a suggestion of model inadequacy. A closer look at the table of the acf of the residuals is here  suggesting structure at lags 7 and 14. Putting the the two clues together ( sample size of 365 and significant weekly i.e. lag 7 structure ) I decided to investigate whether or not this was indeed daily data. New users often omit very important information when they define their data on the mistaken premise that the computer should be smart enough to figure everything out. Note that the lag 7 and lag 14 clues were swamped in the OP'S ACF and PACF plots. The presence of deterministic structure in the residuals increase the error variance thus suppressing the acf. Once the outliers/pulses/level shifts were identified the acf revealed the presence of an autoregressive structure /daily indicators which then needed to be accounted for.

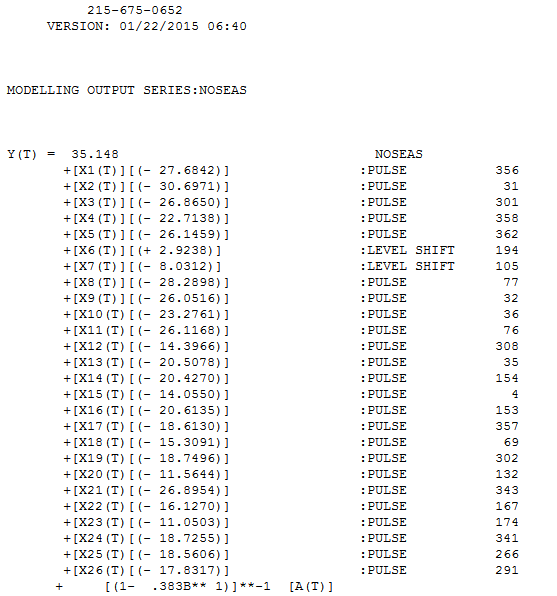

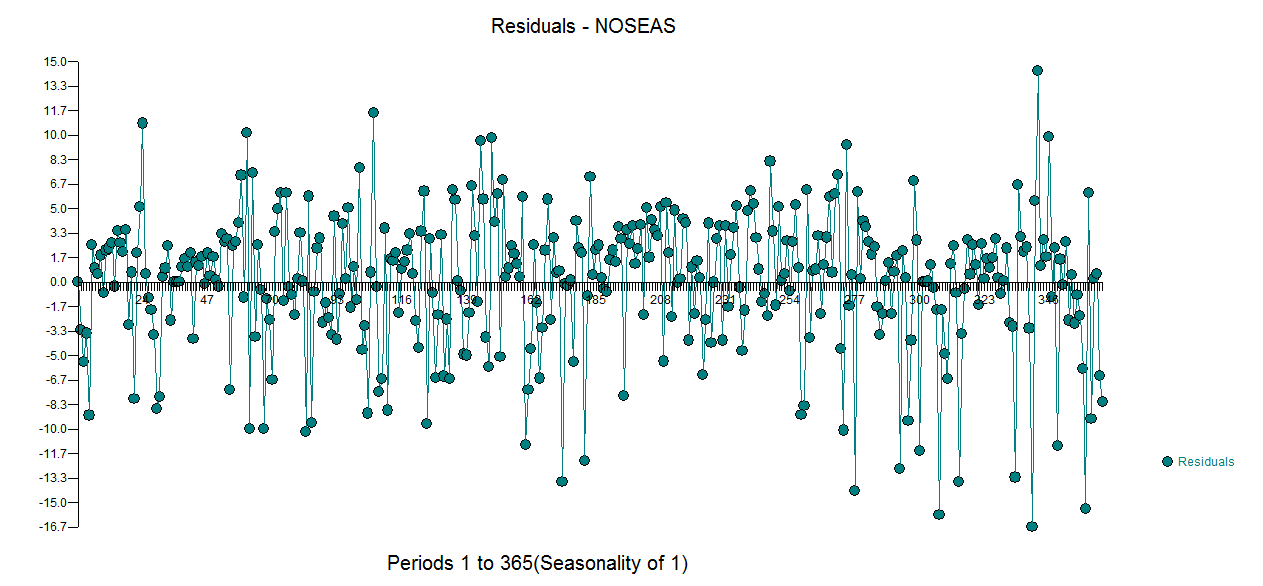

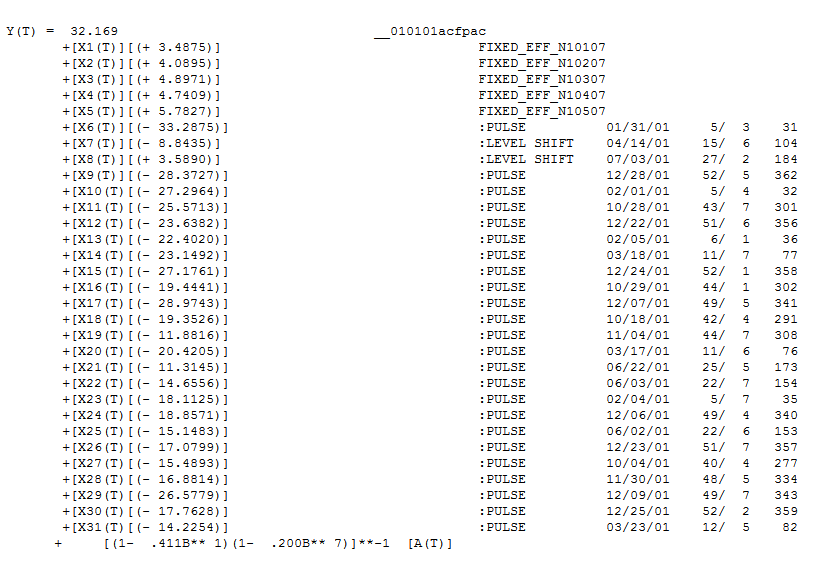

suggesting structure at lags 7 and 14. Putting the the two clues together ( sample size of 365 and significant weekly i.e. lag 7 structure ) I decided to investigate whether or not this was indeed daily data. New users often omit very important information when they define their data on the mistaken premise that the computer should be smart enough to figure everything out. Note that the lag 7 and lag 14 clues were swamped in the OP'S ACF and PACF plots. The presence of deterministic structure in the residuals increase the error variance thus suppressing the acf. Once the outliers/pulses/level shifts were identified the acf revealed the presence of an autoregressive structure /daily indicators which then needed to be accounted for. containing 5 daily dummies , two Level Shifts , a number of pulses and an arima model of the form (1,0,0)(1,0,0) . The plot of the residuals no longer evidences the non-constancy structure as a better model is in place.

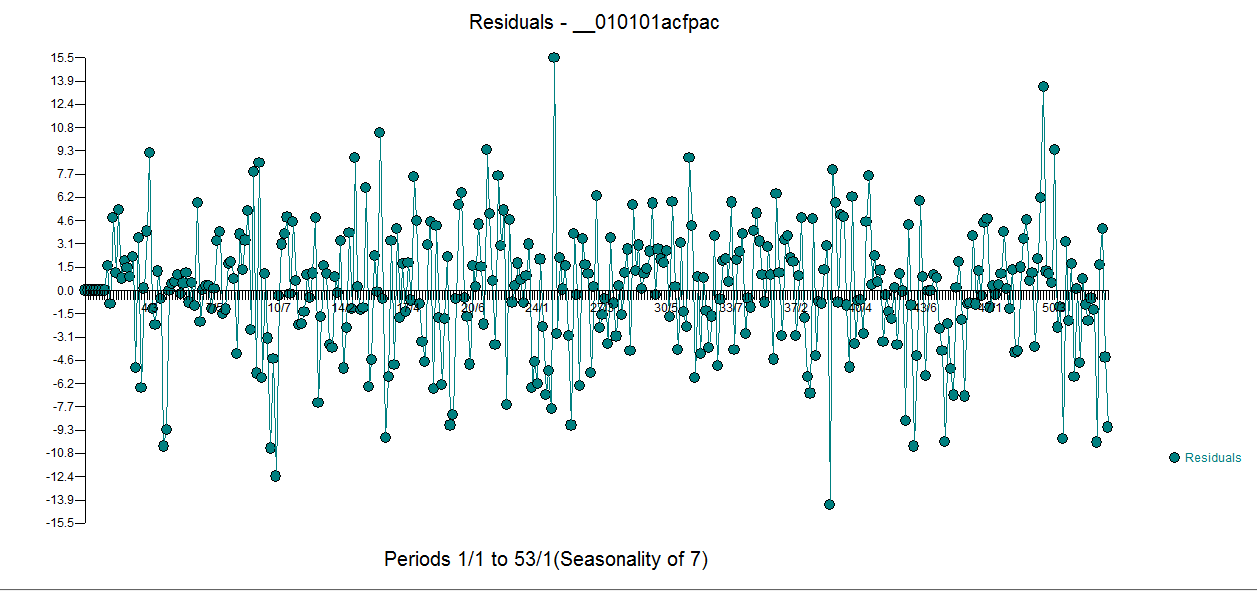

containing 5 daily dummies , two Level Shifts , a number of pulses and an arima model of the form (1,0,0)(1,0,0) . The plot of the residuals no longer evidences the non-constancy structure as a better model is in place. . Th

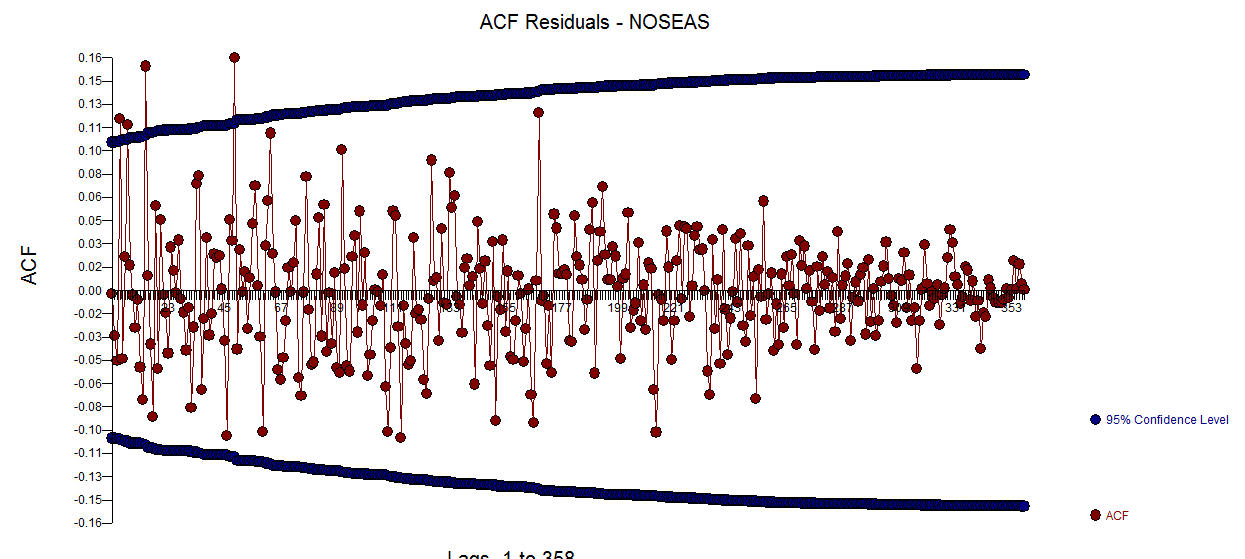

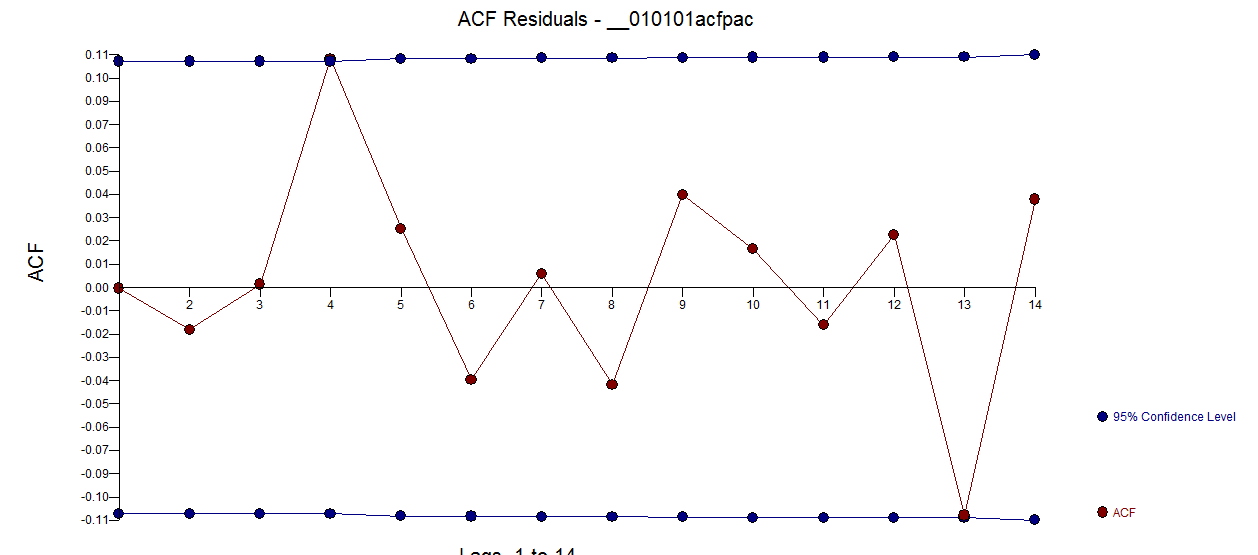

. Th e acf of the residuals is much cleaner . The Actual /Cleansed graph highlights the unusual pulse points.

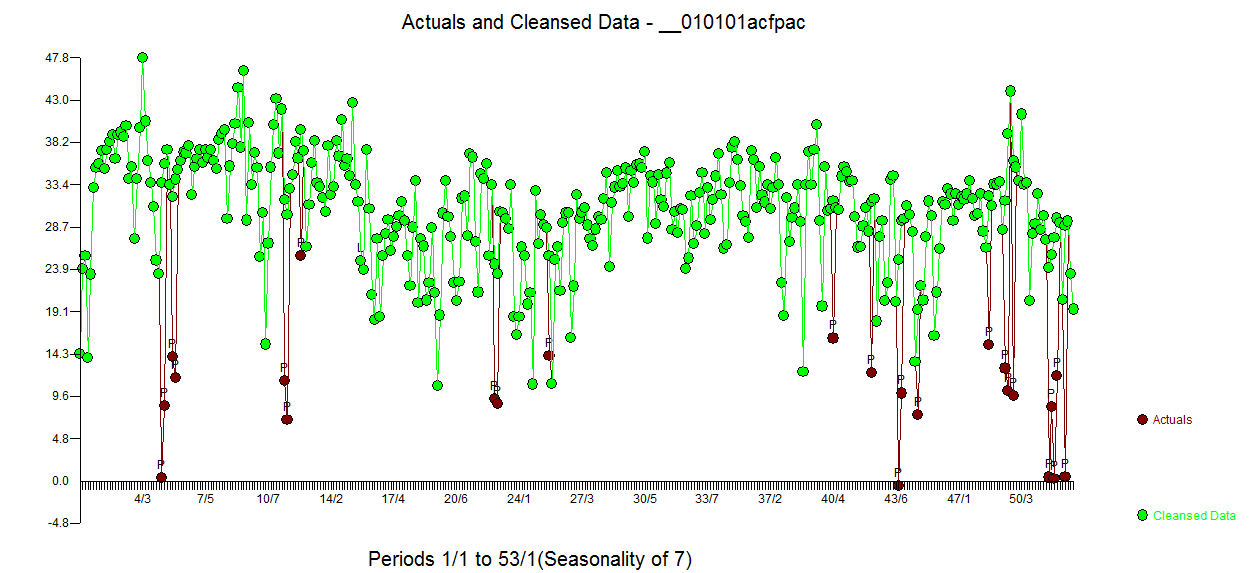

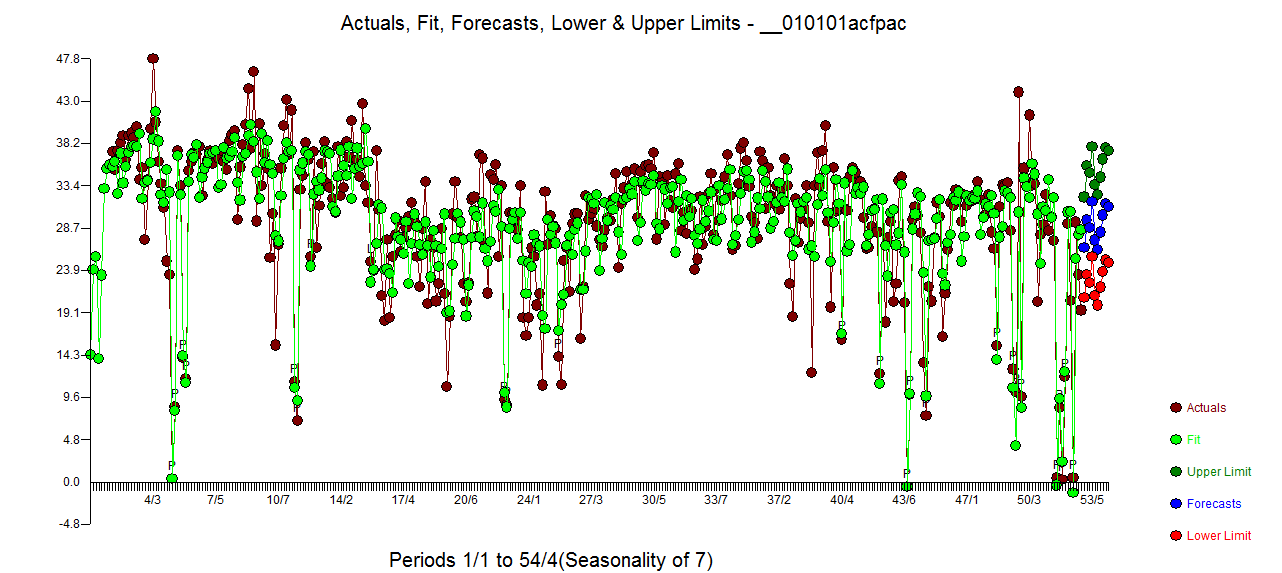

e acf of the residuals is much cleaner . The Actual /Cleansed graph highlights the unusual pulse points.  . THe lesson here is that when one analyzed the data without the critical piece of information that it was a daily time series there were a ton of pulses reflecting an inadequate representation (or perhaps the advanced knowledge of the daily clue ) . The Actual/Fit and Forecast is presented here

. THe lesson here is that when one analyzed the data without the critical piece of information that it was a daily time series there were a ton of pulses reflecting an inadequate representation (or perhaps the advanced knowledge of the daily clue ) . The Actual/Fit and Forecast is presented here .

.