Suppose we have $n$ paired observations $(x_1,y_1),(x_2,y_2),\ldots,(x_n,y_n)$, where $y$ is the response variable and $x$ is the covariate. Consider a simple linear regression model $$y_i=\alpha+\beta x_i+\varepsilon_i\,,$$

where $\varepsilon_i$'s are i.i.d with distribution function $F$. Here $F$ has median $0$, it is absolutely continuous and unknown. We also have $x_1\le x_2\le \cdots\le x_n$, where $x_i$'s are not all equal.

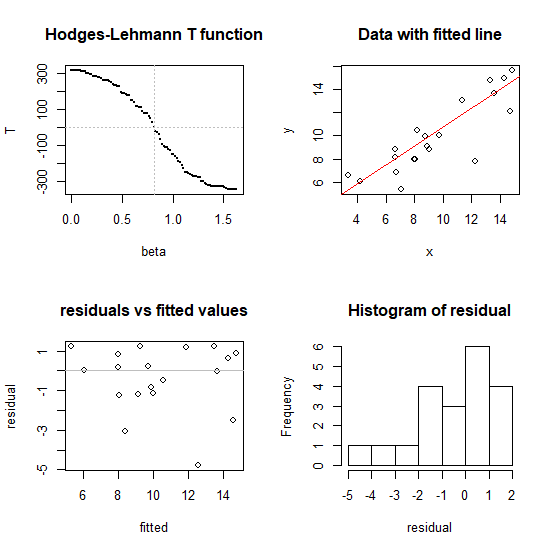

Define $$T(\beta)=\sum_{i=1}^n (x_i-\overline x)R_i(\beta)\,,$$ where $R_i(\beta)$ is the rank of $y_i-\beta x_i$ for every $i$.

Hodges-Lehmann estimator of the slope $\beta$ is then $$\hat\beta_{HL}=\frac{\hat{\overline\beta}+\hat{\underline\beta}}{2}\,,$$

where $\hat{\overline\beta}=\sup\{\beta: T(\beta)>0\}$ and $\hat{\underline\beta}=\inf\{\beta : T(\beta)<0\}$.

Is there a way to calculate $\hat\beta_{HL}$ given a dataset $(x_i,y_i)$, possibly using R? The only possible way seems to be through iteration where I get an approximate solution $\hat\beta_{HL}$ (if it exists) from $T(\hat\beta_{HL})\approx 0$. This is because $T$ is actually a test statistic for testing $H_0:\beta=0$, and under $H_0$, distribution of $T$ is symmetric about $0$. But even then, I am not sure how to actually implement this.

Edit.

Consider the following data with some potential outliers:

x=c(4.37, 4.56, 4.26, 4.56, 4.3, 4.46, 3.84, 4.57, 4.26, 4.37,

3.49, 4.43, 4.48, 4.01, 4.29, 4.42, 4.23, 4.42, 4.23, 3.49,

4.29, 4.29, 4.42, 4.49, 4.38, 4.42, 4.29, 4.38, 4.22, 3.48,

4.38, 4.56, 4.45, 3.49, 4.23, 4.62, 4.53, 4.45, 4.53, 4.43,

4.38, 4.45, 4.5, 4.45, 4.55, 4.45, 4.42)

y=c(5.23, 5.74, 4.93, 5.74, 5.19, 5.46, 4.65, 5.27, 5.57, 5.12,

5.73, 5.45, 5.42, 4.05, 4.26, 4.58, 3.94, 4.18, 4.18, 5.89,

4.38, 4.22, 4.42, 4.85, 5.02, 4.66, 4.66, 4.9, 4.39, 6.05, 4.42, 5.10, 5.22, 6.29, 4.34, 5.62, 5.1, 5.22, 5.18, 5.57, 4.62, 5.06, 5.34, 5.34, 5.54, 4.98, 4.5)

Based on this, the least squares estimate of $\beta$ comes out as $\hat\beta_{LS}=-0.41$, whereas the robust Theil-Sen estimate is $\hat\beta_{TS}=1.73$. I thought the Hodges-Lehmann estimator is also robust to outliers. However, following @Glen_b's approach, I seem to be getting $\hat\beta_{HL}\approx -0.48$ which is close to the non-robust LS estimate. Does this have to do with the number of outliers present in the data? Or is the Hodges-Lehmann estimator defined here supposed to be close to the usual LS estimator?