I would like to conduct a forecast based on a multiple time series ARIMA-model with multiple exogeneous variables. Since I am not that skillfull with regards to neither statistics nor R I want to keep is as simple as possible (Trend forecast for 3 months is sufficient).

I have 1 dependent time series and 3-5 predictor time series, all monthly data, no gaps, same time "horizon".

I encountered the auto.arima function and asked myself if this would be a suitable solution for my problem. I have different commodity prices and prices of products made from them. All raw-data are non-stationary but via first-order differencing they all become stationary data. ADF, KPSS indicate this. (This means that I have tested for integration, right?).

My question now is: How do I apply this with the auto.arima function AND is ARIMA the right approach anyways? Some ppl already adviced me to use VAR, but is it possible with ARIMA too?

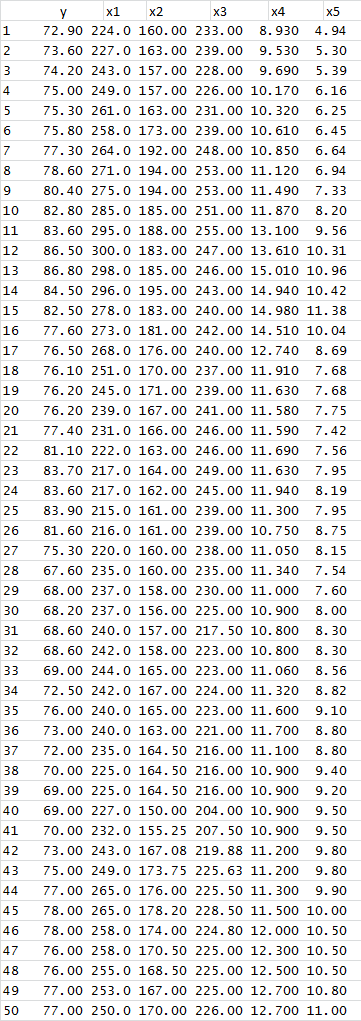

The following table is my data. Actually the data-set goes up til 105 observations, but the first 50 will do. Trend as well as seasonality are obviously of interest here.

Thanks for any advices and help! Georg