I have almost the same questions like this: How can I efficiently model the sum of Bernoulli random variables?

But the setting is quite different:

$S=\sum_{i=1,N}{X_i}$, $P(X_{i}=1)=p_i$, $N$~20, $p_i$~0.1

We have the data for the outcomes of Bernoulli random variables: $X_{i,j}$ , $S_j=\sum_{i=1,N}{X_{i,j}}$

If we estimate the $p_i$ with maximum likelihood estimation (and get $\hat p^{MLE}_i$), it turns out that $\hat P\{S=3\} (\hat p^{MLE}_i)$ is much larger then expected by the other criteria: $\hat P\{S=3\} (\hat p^{MLE}_i) - \hat P^{expected} \{S=3\}\approx 0.05$

So, $X_{i}$ and $X_{j}$ $(j>k)$ cannot be treated as independent (they have small dependence).

There are some constrains like these: $p_{i+1} \ge p_i$ and $\sum_{s \le 2}\hat P\{S=s\}=A$ (known), which should help with the estimation of $P\{S\}$.

How could we try to model the sum of Bernoulli random variables in this case?

What literature could be useful to solve the task?

UPDATED

There are some further ideas:

(1) It's possible to assume that the unknown dependence between ${X_i}$ begins after 1 or more successes in series. So when $\sum_{i=1,K}{X_i} > 0$, $p_{K+1} \to p'_{K+1}$ and $p'_{K+1} < p_{K+1}$.

(2) In order to use MLE we need the least questionable model. Here is an variant:

$P\{X_1,...,X_k\}= (1-p_1) ... (1-p_k)$ if $\sum_{i=1,k}{X_i} = 0$ for any k $P\{X_1,...,X_k,X_{k+1},...,X_N\}= (1-p_1) ... p_k P'\{X_{k+1},...,X_N\}$ if $\sum_{i=1,k-1}{X_i} = 0$ and $X_k = 1$, and $P'\{X_{k+1}=1,X_{k+2}=1,...,X_N=1\} \le p_{k+1} p_{k+2} ... p_N$ for any k.

(3) Since we interested only in $P\{S\}$ we can set $P'\{X_{k+1},...,X_N\} \approx P''\{\sum_{i=1,k}{X_i}=s' ; N-(k+1)+1=l\}$ (the probability of $\sum_{i=k+1,N}{X_i}$ successes for N-(k+1)+1 summands from the tail). And use parametrization $P''\{\sum_{i=k,N}{X_i}=s' ; N-k+1=l\}= p_{s',l}$

(4) Use MLE for model based on parameters $p_1,...,p_N$ and $p_{0,1}, p_{1,1}; p_{0,2}, p_{1,2}, p_{2,2};...$ with $p_{s',l}=0$ for $s' \ge 6$ (and any $l$) and some other native constrains.

Is everything ok with this plan?

UPDATED 2

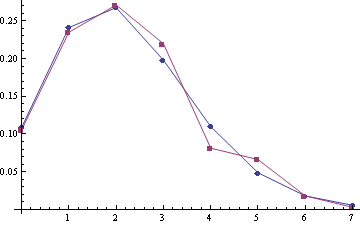

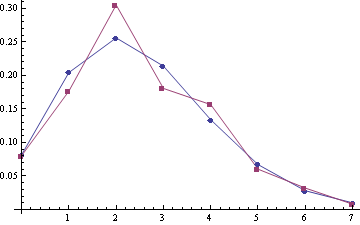

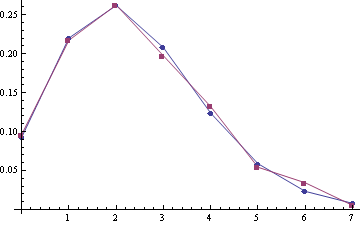

Some examples of empirical distribution $P\{S\}$ (red) compared with Poisson distribution (blue) (the poisson means are 2.22 and 2.45, sample sizes are 332 and 259):

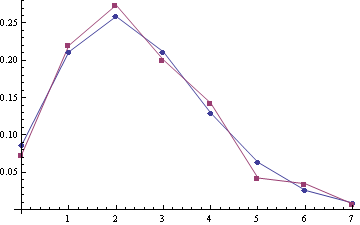

For samples (A1, A2) with the poisson means 2.28 and 2.51 (sample sizes are 303 and 249):

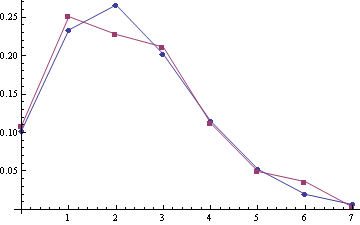

For joined samlpe A1 + A2 (the sample size is 552):

Looks like some correction to Poisson should be the best model :).