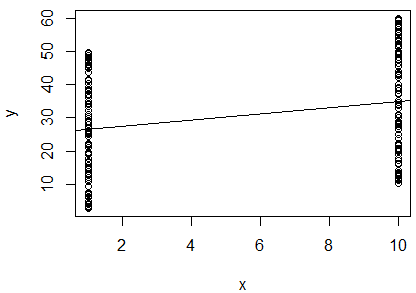

I have run a simple linear regression of the natural log of 2 variables to determine if they correlate. My output is this:

R^2 = 0.0893

slope = 0.851

p < 0.001

I am confused. Looking at the $R^2$ value, I would say that the two variables are not correlated, since it is so close to $0$. However, the slope of the regression line is almost $1$ (despite looking as though it's almost horizontal in the plot), and the p-value indicates that the regression is highly significant.

Does this mean that the two variables are highly correlated? If so, what does the $R^2$ value indicate?

I should add that the Durbin-Watson statistic was tested in my software, and did not reject the null hypothesis (it equalled $1.357$). I thought that this tested for independence between the $2$ variables. In this case, I would expect the variables to be dependent, since they are $2$ measurements of an individual bird. I'm doing this regression as part of a published method to determine body condition of an individual, so I assumed that using a regression in this way made sense. However, given these outputs, I'm thinking that maybe for these birds, this method isn't suitable. Does this seem a reasonable conclusion?