Which of the Gauss-Markov assumptions is violated in this picture?

If all other Gauss-Markov assumptions are satisfied, is the OLS estimator for $\beta_1$ unbiased and consistent? Why?

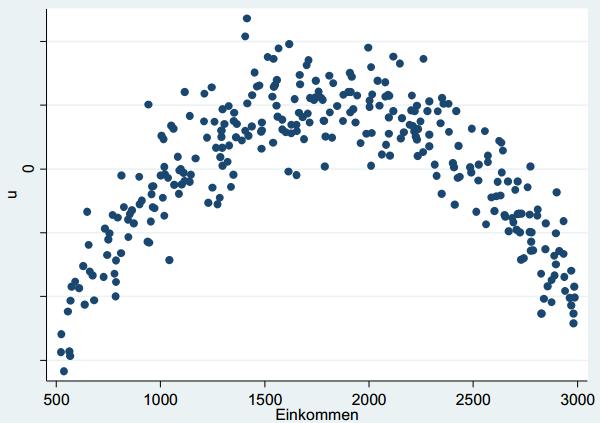

In the diagram, u is the error term, Einkommen is income (an explanatory variable).

The model is specified as follows:

$y = \beta_0 + \beta_1 \text{einkommen} + u$

The problem is taken from an exam.

My thoughts (x is einkommen):

the figure shows a quadratic function

the Gauss-Markov assumptions are:

(1) linearity in parameters

(2) random sampling

(3) sampling variation of x (not all the same values)

(4) zero conditional mean E(u|x)=0

(5) homoskedasticity

I think (4) is satisfied, because there are residuals above and below 0

(5) is satisfied, since the variation seems to be constant over all x (3) satisfied , since einkommen is not the same value for all observations (2) random sampling is satisfied, dont ask me why. so only (1) is left, the model is not linear in parameters.

I hope I am not totally wrong with my thoughts.

Einkommenand the model: is it a covariate? The dependent variable? The predicted value? A variable not in the model at all? $\endgroup$[self-study]tag & read its wiki, then tell us what you understand thus far, & where you are stuck. We will provide hints to help you get unstuck. $\endgroup$