I was wondering if there is a way to tell the probability of something failing (a product) if we have 100,000 products in the field for 1 year and with no failures? What is the probability that one of the next 10,000 products sold fail?

$\begingroup$

$\endgroup$

8

-

4$\begingroup$ Something tells me this is not the real reliability problem. There are no products with such a low failure rates. $\endgroup$– AksakalCommented Jan 23, 2015 at 1:08

-

1$\begingroup$ You need a model for the distribution of possible success/failure rates before you can infer anything from the statistics to the probabilities for actual success/failure rates. Your description gives very little basis from which to infer/assume such a distribution. $\endgroup$– RBarryYoungCommented Jan 23, 2015 at 16:57

-

1$\begingroup$ @RBarryYoung please check the answers provided - they provide few interesting and valid approaches to the problem. If you don't agree with those approaches feel free to comment them or to provide your own answer. $\endgroup$– TimCommented Jan 23, 2015 at 18:42

-

4$\begingroup$ @Aksakal - such a low failure rate doesn't seem impossible if it's a simple product with high value and such a high risk in the event of failure (like a surgical instrument) that it goes through levels of testing and inspection (and possibly independent certification) before release. Of course, the opposite could be true, the product could have such a low value that end users just aren't reporting problems with defective products (surely gumball manufactures have less than a 1/100000 reported defect rate?), the consumer just discards it and tries a new one. $\endgroup$– JohnnyCommented Jan 24, 2015 at 5:49

-

2$\begingroup$ I described estimating lower bounds for survival using a parametric failure distribution on this post. The approach, median unbiased estimation, has not been discussed in any of the comments or posts on this page. $\endgroup$– AdamOCommented Feb 21, 2018 at 22:37

|

Show 3 more comments

9 Answers

$\begingroup$

$\endgroup$

$\endgroup$

14

The probability that a product will fail is surely a function of time and use. We don't have any data on use, and with only one year there are no failures (congratulations!). Thus, this aspect (called the survival function), cannot be estimated from your data.

You can think of failures within one year as draws from a binomial distribution, however. You still have no failures, but this is now a common problem. A simple solution is to use the rule of 3, which is accurate with large $N$ (which you certainly have). Specifically, you can get the upper bound of a one-sided 95% confidence interval (i.e., the lower bound is $0$) on the true probability of failure within one year as $3/N$. In your case, you are 95% confident that the rate is less than $0.00003$.

You also asked how to compute the probability that one or more of the next 10k fails. A quick and simple (albeit extreme) way to extend the above analysis is to just use the upper bound as the underlying probability and use the corresponding binomial CDF to get the probability that there won't be $0$ failures. Using R code, we could do: 1-pbinom(0, size=10000, prob=0.00003), which yields a 0.2591851 chance of seeing one or more failures in the next 10k products. By having used the upper bound, this is not the optimal point estimate of the probability of having at least one failure, rather you can say it is very unlikely that the probability of $\ge 1$ failure is more than $\approx 26\%$ (recognizing that this is a somewhat 'hand-wavy' framing). Another possibility is to use @amoeba's suggestion of the estimate from Laplace's rule of succession. The rule of succession states that the estimated probability of failure is $(F+1)/(N+2)$, where $F$ is the number of failures. In that case, $\hat p = 9.9998\times 10^{-06}$, and the calculation for the predicted probability of $1^+$ failures in the next 10,000 is 1-pbinom(0, size=10000, prob=9.9998e-06), yielding 0.09516122, or $\approx 10\%$.

answered Jan 21, 2015 at 18:50

-

3$\begingroup$ +1. I have not heard about the "rule of 3" before. I wonder if there is any connection between the rule of 3 and "Laplace's rule of succession"? According to the latter (if I apply it correctly), probability of failure can be estimated as $1/(N+2)$. $\endgroup$– amoebaCommented Jan 21, 2015 at 19:01

-

16$\begingroup$ @amoeba This rule of 3 is a 95% one-sided confidence limit. Assume the failure count has a Binomial$(n,p)$ distribution. Then the chance of seeing no failures is $(1-p)^n$. To make that greater than $5\%$, solve $(1-p)^n\ge 0.05$ for $p$. Using $\log(1-p)\approx -p$ for small $p$, the solution is $p\le -\log(0.05)/n$. Since $0.05=1/20\approx e^3$, we obtain $p\le 3/n$. That's the "rule of 3." It's worth knowing because now you know how to vary the "3" if you want to adjust the confidence level and you also can invert it to find the minimum $n$ needed to detect a rate of $p$ or greater. $\endgroup$– whuber ♦Commented Jan 21, 2015 at 19:25

-

1$\begingroup$ @amoeba as I mentioned, I took a uniform prior over the failure probability. I believe that a different prior would have lead to considerably different results. $\endgroup$ Commented Jan 22, 2015 at 13:06

-

1$\begingroup$ Your edit is good progress (+1). However, it raises issues of interpretation. We are not "sure" the chance is not more than $26\%$ because we are not completely certain of the true underlying chance. We do not have an "upper bound" on $p$, but only an upper confidence limit. When you give a prediction for a future event, you need to (a) estimate it and (b) provide bounds on it. Look at it like this: give us bounds on $Y$ when $X\sim\text{Binomial}(n,p)$, $Y\sim\text{Binomial}(m,p)$ independently, conditional on $X=0$. Those bounds are a prediction interval for $Y$ based on $X$. $\endgroup$– whuber ♦Commented Jan 22, 2015 at 17:27

-

3$\begingroup$ Yay for the "Rule of three". I fist saw it many years ago in a short note to the "Journal of the American Medical Association" jama.jamanetwork.com/article.aspx?articleid=385438 $\endgroup$– DWinCommented Jan 25, 2015 at 21:19

$\begingroup$

$\endgroup$

24

You can take a bayesian approach. denote the probability of failure by $\Theta$ and think of it as a random variable. A priori, before you see the results of the experiments, you might believe that $\Theta \sim U(0,1)$. If you trust the engineers to make this product reliable, maybe you can take $\Theta \sim U(0,0.1)$ or so. This is up to you. Then, you can use Bayes' theorem to calculate the posterior distribution of $\theta$. Denote $A$ the event that you've observed ($n$ experiments with zero failures).

$$ p(\Theta = \theta | A) = \frac{p (A | \Theta = \theta) p(\Theta = \theta )}{p(A)} = \frac{p (A |\theta) p(\theta )}{\int p (A |\theta) p(\theta )d\theta}. $$ Everything is simple: $\Theta$ is uniform, so $p(\theta)$ is some constant. Since you run $n$ experiments, $p(A | \theta)$ is just the probability of no failures in $n$ bernouli trials with probability of failure $\theta$.

Once you have $p(\theta | A)$ you're gold: you can calculate the probability of any event $B$ by integrateion: $\mathbb{P}(B) = \int p(B |\theta) p(\theta |A) d\theta$

Below, I work through a detailed solution, following the above approach. I'll take a few standard shortcuts.

Let the prior be $U(0,1)$. Then: $$ p(\theta |A)\propto p(A|\theta) \cdot 1 = (1-\theta)^n. $$ The normalization constant $p(A) = \int p(A|\theta)p(\theta) d\theta$ is found to be $B(1,n+1)$ - see wikipedia pages beta function and beta distribution. So, $p(\theta |A) = \frac{(1-\theta)^n}{B(1,n+1)}$, which is a beta distribution with parameters $1, n+1$.

Denote the probability of no failures in $m$ products in the next year by $B$. The probability of at least one failure is $1 -\mathbb{P}( B )$. Then $$ 1- \mathbb{P}(B) =1 - \int (1-\theta)^m\frac{(1-\theta)^n}{B(1,n+1)}d\theta = \frac{B(1,n+m+1)}{B(1,n+1)} $$

which is roughly $0.1$, using $n= 100,000, m = 10,000$. Not very impressive? I took a uniform distribution on the probability of failure. Perhaps you have better prior faith in your engineers.

-

3$\begingroup$ It seems strange to fall so short of an actual solution for such a simple problem, especially when the method looks so promising. Are you suggesting the calculations are difficult? $\endgroup$– whuber ♦Commented Jan 21, 2015 at 19:52

-

2$\begingroup$ @whuber I did not forget it, I thought this last step is obvious. What I meant by "unumpressive" is that 10% probability of failure is still big, when compared to no failures in the first 100,000 runs. Also, thanks for the comment regarding conjugate pairs, I thought it would might confuse the OP and distract them from what's important, hence omitted it. $\endgroup$ Commented Jan 21, 2015 at 21:25

-

3$\begingroup$ Obvious, yes--but when you end up with a value of 0.9, that's the number people will see, almost no matter what you say about it in the preceding text. So that you are not misunderstood, it is always helpful to be explicit about what answer you are offering. (+1 for the improved answer, BTW) $\endgroup$– whuber ♦Commented Jan 21, 2015 at 21:27

-

3$\begingroup$ Indeed, regardless of your faith in your engineers, it's not really very surprising that, if you observe $n \gg 1$ trials with no failure, you should on average expect about $k$ failures within the next $kn$ trials, and thus should expect at least one failure with probability $1-e^{-k}$, which is approximately $k$ for small $k$. Thus, 100,000 successful trials yields a roughly 10% expected probability of at least one failure within the next 10,000 trials. $\endgroup$ Commented Jan 22, 2015 at 14:41

-

2$\begingroup$ @whuber Your assumption that the prior does not matter is not true in the case of zero-failures. It depends heavily on the slope near zero, for example the flat uniform prior (beta 1,1) and Jeffreys prior (beta 0.5, 0.5) will give a substantially different posterior. $\endgroup$– ErikCommented Jan 23, 2015 at 7:24

$\begingroup$

$\endgroup$

8

Rather than computing a probability, why not predict how many products might fail?

Modeling the Observations

There are $n=100000$ products in the field and another $m=10000$ under consideration. Assume their failures are all independent and constant with probability $p$.

We may model this situation by means of a Binomial experiment: out of a box of tickets with an unknown proportion $p$ of "failure" tickets and $1-p$ "success" tickets, draw $m+n=110000$ tickets (with replacement, so that the chance of failure stays the same). Count the failures among the first $n$ tickets--let that be $X$--and count the failures among the remaining $m$ tickets, calling that $Y$.

Framing the Question

In principle, $0\le X \le n$ and $0 \le Y\le m$ could be anything. What we are interested in is the chance that $Y = u$ given that $X+Y=u$ (with $u$ any number in $\{0,1,\ldots, m\}$). Since the failures could occur anywhere among all $n+m$ tickets, with every possible configuration having the same chance, it is found by dividing the number of $u$-subsets of $m$ things by the number of $u$-subsets of all $n+m$ things:

$$p(u;n,m) = \Pr(Y = u\,|\, X+Y=u) = \frac{\binom{m}{u}}{\binom{n+m}{u}} \\= \frac{m(m-1)\cdots(m-u+1)}{(n+m)(n+m-1)\cdots(n+m-u+1)}.$$

Comparable formulas can be used for the calculation when $X=1, 2, \ldots.$

An upper $1-\alpha$ prediction limit (UPL) for the number of failures in those last $m$ tickets, $t_\alpha(X;n,m)$, is given by the smallest $u$ (depending on $X$) for which $p(u;n,m) \le \alpha$.

Interpretation

The UPL should be interpreted in terms of the risk of using $t_\alpha$, as evaluated before either $X$ or $Y$ is observed. In other words, suppose it is one year ago and you are being asked to recommend a procedure to predict the number of failures in the next $m$ products once the first $n$ have been observed. Your client asks

What is the chance that your procedure will underpredict $Y$? I don't mean in the future after you have more data; I mean right now, because I have to make decisions right now and the only chances I will have available to me are the ones that can be computed at this moment."

Your response can be,

Right now the chance is no greater than $\alpha$, but if you plan to use a smaller prediction, the chance will exceed $\alpha$.

Results

For $n=10^5$, $m=10^4$, and $X=0$ we may compute that

$$p(0,n,m)=1;\ p(1,n,m)=\frac{1}{11}\approx 0.091;\ p(2,n,m)=\frac{909}{109999}\approx 0.0083; \ldots$$

Thus, upon having observed $X=0$,

For up to $1-\alpha=90.9\%$ confidence (that is, when $9.1\%\le \alpha$), predict there is at most $t_\alpha(0;n,m)=1$ failure in the next $10,000$ products.

For up to $99.2\%$ confidence (that is, when $0.8\%\le \alpha \lt 9.1\%$), predict there are at most $t_\alpha(0;n,m)=2$ failures in the next $10,000$ products.

Etc.

Comments

When and why would this approach apply? Suppose your company makes lots of different products. After observing the performance of $n$ of each one in the field, it likes to produce guarantees, such as "complete no-cost replacement of any failure within one year." By having prediction limits for the number of failures you can control the total costs of having to back those guarantees. Because you make many products, and expect failures to be due to random circumstances beyond your control, the experience of each product will be independent. It makes sense to control your risk in the long run. Every once in a while you might have to pay more claims than expected, but most of the time you will pay fewer. If paying more than announced could be ruinous, you will set $\alpha$ to be extremely small (and you likely would use a more sophisticated failure model, too!). Otherwise, if the costs are minor, then you can live with low confidence (high $\alpha$). These calculations show how to balance confidence and risks.

Note that we don't have to compute the full procedure $t$. We wait until $X$ is observed and then just carry out the calculations for that particular $X$ (here, $X=0$), as shown above. In principle, though, we could have carried out the calculations for all possible values of $X$ at the outset.

A Bayesian approach (described in other answers) is attractive and will work well provided the results do not depend heavily on the prior. Unfortunately, when the failure rate is so low that very few (or no failures) are observed, the results are sensitive to the choice of prior.

-

$\begingroup$ +1, but $p(0,n,m)=1$ doesn't seem to be correct. $\endgroup$– amoebaCommented Jan 22, 2015 at 22:34

-

1$\begingroup$ @COOLSerdash, because $\sum_u p(u,n,m)=1$, and the terms for $u=1,2...$ are not equal to zero. $\endgroup$– amoebaCommented Jan 22, 2015 at 23:18

-

1$\begingroup$ The reason you're getting $\sum_u p(u;n,m) > 1$, as @amoeba notes, is because your $p(u;n,m) = \frac{m \choose u}{n+m \choose u}$ isn't really ${\rm Pr}(Y=u|X=0)$, but rather ${\rm Pr}(Y=u|X+Y=u)$ $=$ ${\rm Pr}(X=0|X+Y=u)$ (and should thus really be denoted e.g. as $p(0;n,m,u)$ or something like that). I'm having some trouble following exactly what you do with that later on, but I'm pretty sure that, whatever it is, it's unfortunately not a correct solution to the problem as asked. $\endgroup$ Commented Jan 24, 2015 at 18:12

-

1$\begingroup$ @IlmariKaronen Thank you for your comments. You are right that I should have characterized $p(u;n,m)$ a little more clearly, because it is not a probability distribution over $u$--it is a conditional probability--but I believe the answer itself nevertheless is correct and I am very confident that this approach to computing prediction limits is both correct and conventional. I will edit this post to clarify these points. $\endgroup$– whuber ♦Commented Jan 25, 2015 at 19:08

-

1$\begingroup$ @Ilmari I already made the edit--you can see it in the edit history. I assume no priors and only apply the definition of a prediction interval to this problem. If you wish to challenge whether that is "statistically meaningful," then you will find yourself quixotically challenging this standard construct. See, for instance, Hahn & Meeker, Statistical Intervals (J. Wiley 1991). $\endgroup$– whuber ♦Commented Jan 25, 2015 at 20:56

$\begingroup$

$\endgroup$

1

The following is a Bayesian answer to "Out of 10,000 new products, how many are expected to fail if all the former 100,000 produced didn't fail?", but you should consider the sensitivity to different priors.

Suppose that $X_1,\dots,X_n$ are conditionally independent and identically distributed, given $\Theta=\theta$, such that $X_1\mid\Theta=\theta\sim\mathrm{Bernoulli}(\theta)$, and use the conjugate prior $\Theta\sim\mathrm{Beta}(a,b)$, with $a,b>0$.

For $m<n$, we have $$ \mathrm{E}\left[\sum_{i=m+1}^n X_i\;\Bigg\vert\; X_1=0,\dots X_m=0 \right] = \sum_{i=m+1}^n \mathrm{E}\left[ X_i\mid X_1=0,\dots X_m=0 \right] \, . $$

For $m+1\leq i\leq n$, we have $$ \begin{align} \mathrm{E}\left[X_i\mid X_1=0,\dots X_m=0\right] &= \Pr(X_i=1\mid X_1=0,\dots X_m=0) \\ &= \int_0^1 \Pr(X_i=1\mid \Theta=\theta) \,f_{\Theta\mid X_1,\dots,X_m}(\theta\mid 0,\dots,0) \,d\theta \\ &= \frac{\Gamma(m+a+b)}{\Gamma(m+a+b+1)} \frac{\Gamma(a+1)}{\Gamma(a)} = \frac{a}{m+a+b}\, , \end{align} $$ in which we used $\Theta\mid X_1=0,\dots,X_m=0\sim \mathrm{Beta}(a,m+b)$.

Plugging in your numbers, with an uniform prior ($a=1,b=1$) you expect a failure rate around $10\%$, while a Jeffreys-like prior ($a=1/2,b=1/2$) gives you a failure rate close to $5\%$.

This predictive expectation doesn't look like a good summary, because the predictive distribution is highly skewed. We can go further and compute the predictive distribution. Since $$ \sum_{i=m+1}^n X_i \;\Bigg\vert\; \Theta=\theta \sim \mathrm{Bin}(n-m+2,\theta) \, , $$ conditioning as we did before we have $$ \begin{align} \Pr&\left(\sum_{i=m+1}^n X_i=t \;\Bigg\vert\; X_1=0,\dots X_m=0\right) = \\ &\qquad\qquad\qquad\qquad\binom{n-m+2}{t} \frac{\Gamma(m+a+b)}{\Gamma(a)\Gamma(m+b)} \frac{\Gamma(t+a)\Gamma(n-t+2)}{\Gamma(n+a+2)} \, , \end{align} $$ for $t=0,1,\dots,n-m+2$.

I'll finish it later computing a $95\%$ predictive interval.

-

3$\begingroup$ +1 for demonstrating that the result is sensitive to the shape of the prior near 0. (It's worth noting that, since the likelihood function is strongly concentrated near zero when $m$ is large, that's the only part of the prior that really matters. For example, for a $\mathrm{Beta}(a,b)$ prior, the expectation $\frac{a}{m+a+b}\approx\frac am$ is approximately proportional to $a$, but almost independent of $b$. Similarly, for a uniform prior, it doesn't really matter much whether the prior is $U(0,1)$ or $U(0,0.01)$, but things would change dramatically if we assumed a prior like $U(0.01,1)$.) $\endgroup$ Commented Jan 24, 2015 at 17:30

$\begingroup$

$\endgroup$

2

Several good answers were provided for this question, but recently I had a chance to review few resources on this topic and so I decided to share the results.

There are multiple possible estimators for zero-failures data. Let's denote $k=0$ as number of failures and $n$ as sample size. Maximum likelihood estimator for probability of failure given this data is

$$ P(K = k) = \frac{k}{n} = 0 \tag{1} $$

Such estimate is rather unsatisfactory since the fact that we observed no failures in our sample hardly proves that they are impossible in general. Out out-of-data knowledge suggests that there is some probability of failure even if non were observed (yet). Having a priori knowledge leads us to using Bayesian methods reviewed by Bailey (1997), Razzaghi (2002), Basu et al (1996), and Ludbrook and Lew (2009).

Among simple estimators "upper bound" estimator that assumes (Bailey, 1997)

that it would not be logical for an estimator for P in the zero-failure case to yield a probability in excess of that predicted by the maximum likelihood estimator in the one-failure case, a reasonable upper bound

defined as

$$ \frac{1}{n} \tag{2} $$

can be mentioned. As reviewed by Ludbrook and Lew (2009), other possibilities are "rule of threes" (cf. here, Wikipedia, or Eypasch et al, 1995)

$$ \frac{3}{n} \tag{3} $$

or other variations:

$$ \frac{3}{n+1} \tag{4} $$

"rule of 3.7" by Newcombe and Altman (or by 3.6):

$$ \frac{3.7}{n} \tag{5} $$

"new rule of four":

$$ \frac{4}{n+4} \tag{6} $$

but as concluded by Ludbrook and Lew (2009) "rule of threes" is "next to useless" and "rule of 3.6" (and 3.7) "have serious limitations – they are grossly inaccurate if the initial sample size is less than 50" and they do not recommend methods (3)-(6), suggesting rather to use proper Bayesian estimators (see below).

Among Bayesian estimators several different can be mentioned. First such estimator suggested by Bailey (1997) is

$$ 1 - 0.5^\frac{1}{n} \tag{7} $$

for estimating median under uniform prior

$$ 1 - 0.5^\frac{1}{n+1} \tag{8} $$

or for estimating mean under such prior

$$ \frac{1}{n+2} \tag{9} $$

yet another approach assuming exponential failure pattern with constant failure rate (Poisson distributions) yields

$$ \frac{1/3}{n} \tag{10} $$

if we use beta prior with parameters $a$ and $b$ we can use formula (see Razzaghi, 2002):

$$ \frac{a}{a+b+n} \tag{11} $$

that under $a = b = 1$ leads to uniform prior (9). Assuming Jeffreys prior with $a = b = 0.5$ it leads to

$$ \frac{1}{2(n+1)} \tag{12} $$

Generally, Bayesian formulas (7)-(12) are recommended. Basu et al (1996) recommends (11) with informative prior, when some a priori knowledge is available. Since no single best method exists I would suggest reviewing the literature prior to your analysis, especially when $n$ is small.

Bailey, R.T. (1997). Estimation from zero-failure data. Risk Analysis, 17, 375-380.

Razzaghi, M. (2002). On the estimation of binomial success probability with zero occurrence in sample. Journal of Modern Applied Statistical Methods, 1(2), 41.

Ludbrook, J., & Lew, M. J. (2009). Estimating the risk of rare complications: is the ‘rule of three’good enough?. ANZ journal of surgery, 79(7‐8), 565-570.

Eypasch, E., Lefering, R., Kum, C.K., and Troidl, H. (1995). Probability of adverse events that have not yet occurred: A statistical reminder. BMJ 311(7005): 619–620.

Basu, A.P., Gaylor, D.W., & Chen, J.J. (1996). Estimating the probability of occurrence of tumor for a rare cancer with zero occurrence in a sample. Regulatory Toxicology and Pharmacology, 23(2), 139-144.

-

1$\begingroup$ Excellent review of what is out there! $\endgroup$– AlefSinCommented Jan 14, 2016 at 21:10

-

$\begingroup$ For the comments starting w/ "Among Bayesian estimators several...", it isn't generally clear whether a given comment pertains to the formula above it or below it. Can you make that clearer? $\endgroup$ Commented Dec 28, 2016 at 17:19

$\begingroup$

$\endgroup$

4

Using Laplace's sunrise problem approach, we get the probability that a product would fail within a year $$p=\frac{1}{100000+1}$$. Next, the probability that of $n$ new products none fails within a year is $$(1-p)^n$$ Hence, the probability that at least one product of $n$ will fail in next year is $$1-\left(1-\frac{1}{100001}\right)^{n}$$ For $n=10000$ the value is $P_{10000}\approx 0.095$. In whuber's case $P_{200000}\approx 0.87$, quite high, in fact.

Of course, you should keep updating your data while more products are sold, eventually one will fail.

-

$\begingroup$ This answer appears to be incorrect: the calculation for one future sunrise does not extend simply via multiplication. After all, suppose the number $10,000$ were replaced by $200,000$. Would you assert the probability of failure is $200000/100001\approx 2$?? You should compare your answer to the analysis in Yair Daon's answer and to the related comments. $\endgroup$– whuber ♦Commented Jan 22, 2015 at 22:13

-

-

1$\begingroup$ (1) Either you miscalculated or your "200000" is a typo for "20000". (You should obtain about $0.865$.) (2) Your analysis now reproduces a part of Yair Daon's conclusions, but without the benefit of producing the full posterior distribution. $\endgroup$– whuber ♦Commented Jan 22, 2015 at 22:30

-

$\begingroup$ @whuber, yes it was one less zero $\endgroup$– AksakalCommented Jan 22, 2015 at 22:31

$\begingroup$

$\endgroup$

You really need to go back to the designers of your products. It is a fundamental engineering problem not an observational statistical one. They will have an idea of the failure probability of each component and from that the net failure probabilty of the total assembled product. They can give you the expected number of failures over the whole design life of the product.

A civil engineer designs a bridge to have a design life of 120 years. Each component of the bridge has a slight chance of failure. Each loading has a slight chance of being exceeded. To make the bridge economic to build, total collapse would only occur once in 2400 years which is far longer than the bridge will be maintained for. It is not surprising that the bridge does not fail in year 1, nor year 2 to year 120. That is has not collapsed tells you very little. Its various chances of failure with time can only be estimated by the original designers.

$\begingroup$

$\endgroup$

This is similar to a problem I faced when we introduced a new manufacturing process to eliminate a failure in production.

The new system produced no failures so people were asking the same question: how do we predict the failure rate? In your case, because you have stipulated a period over which the failure can occur with no concern for when the failure occurs within that period, the temporal effects have been removed. And it is simply a case of whether something failed or not. With that stipulated - on with my answer.

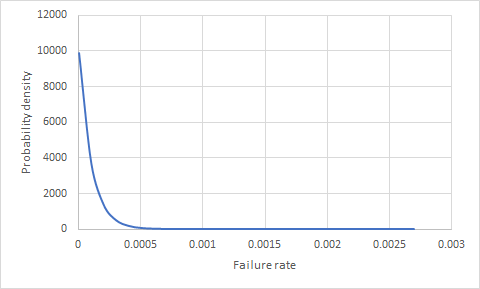

Intuitively, it seems we need at least one failure to be able to calculate the failure rate. However, this assumption has an implicit mistake within it. We will never calculate the failure rate. That is because we are dealing with a sample. Thus we can only estimate a range of probable failure rates. The way to do this is to find a distribution for the failure rate. The distribution that does the job in this instance is a Beta distribution where the parameters are: α = n + 1 and β = N - n + 1

Note: N is the sample size and n is the number of failures (in your case 0)

For your scenario, the distribution of the of the failure rate is shown below.

.

.

You would then feed that distribution into the respective binomial probability formula to get a distribution for the probability of one unit failing (could be done analytically or using Monte Carlo). I suspect that numbers will be very low.

Note that this process is applicable no matter the number of failures in your fist set.

$\begingroup$

$\endgroup$

Median unbiased estimates can be used to estimate sample proportions and (non-singular) 95% CIs in Bernoulli samples with no variability. In a sample with no positive cases, you can estimate the upper bound of a 95% confidence interval with the following formula:

$$ p_{1-\alpha/2} : P(Y=0)/2 + P(Y>y) > 0.975$$

that is we seek a value $p_{1-\alpha/2}$ as the upper bound of the CI so that the Bernoulli process with probability $p=p_{1-\alpha/2}$ gives the above probability inequality. In R this is solved with a NR-like uniroot application.

set.seed(12345)

y <- rbinom(100, 1, 0.01) ## all 0

cil <- 0

mupfun <- function(p) {

0.5*dbinom(0, 100, p) +

pbinom(1, 100, p, lower.tail = F) -

0.975

} ## for y=0 successes out of n=100 trials

ciu <- uniroot(mupfun, c(0, 1))$root

c(cil, ciu)

[1] 0.00000000 0.05357998 ## includes the 0.01 actual probability