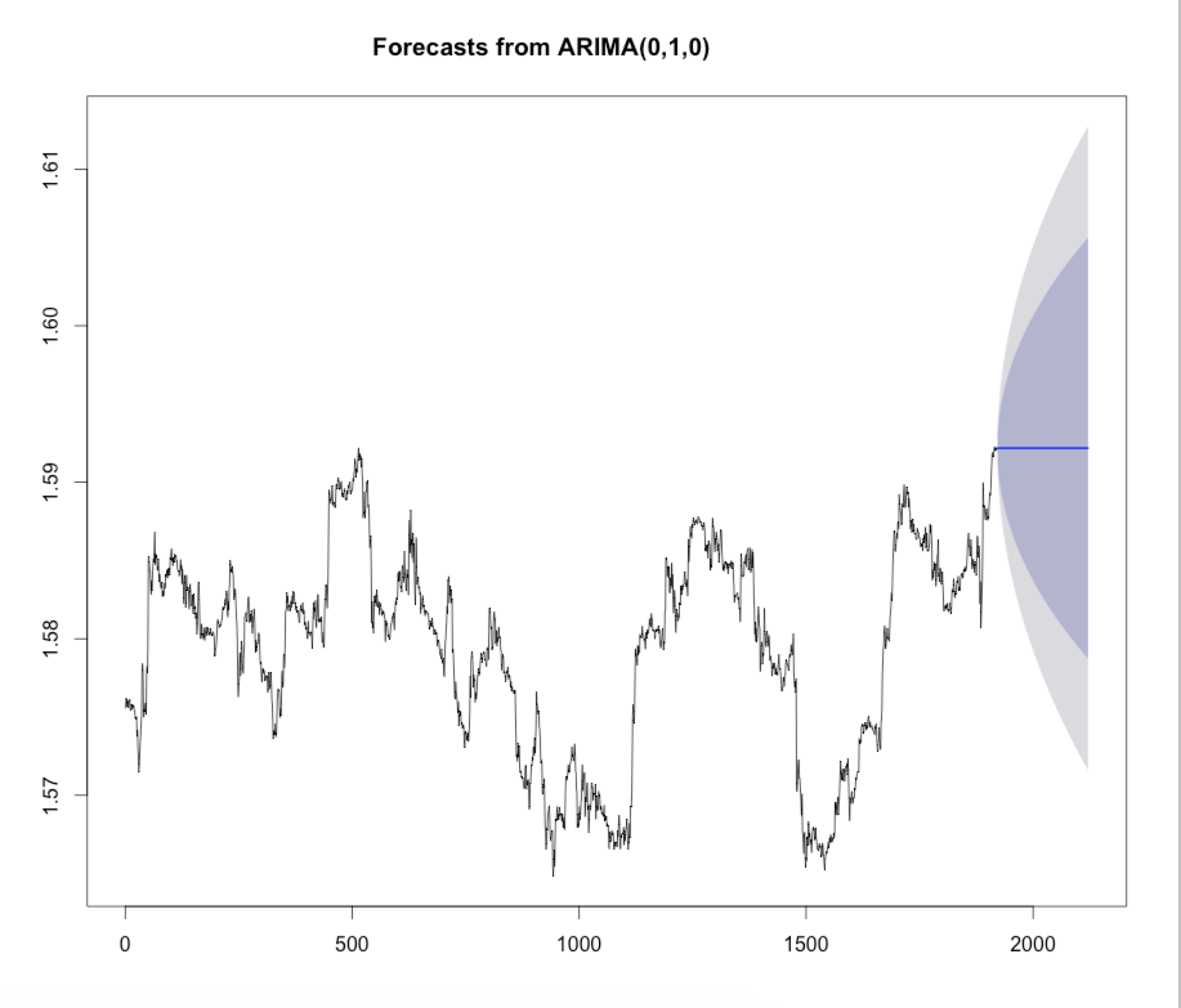

I've created an Arima model based on past forex closing prices using auto arima, which has generated a (0,1,0) ARIMA model.

> auto.arima(ma5)

Series: ma5

ARIMA(0,1,0)

sigma^2 estimated as 5.506e-07: log likelihood=11111.42

AIC=-22220.83 AICc=-22220.83 BIC=-22215.27

I next tried to plot the forecasted values, but as you can see all predictions are constant. Anyone know what I'm doing wrong?

include.driftinforecast::Arimaand applyforecaston the fitted model. $\endgroup$