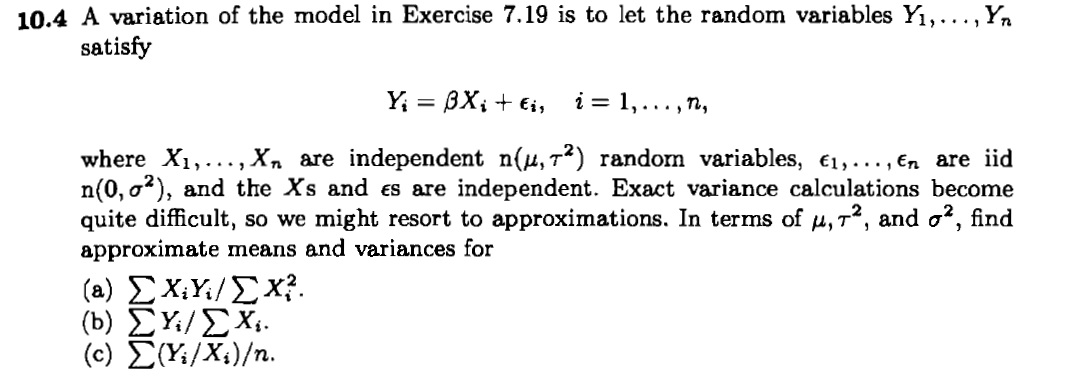

I've been slowly working my way through problems in Casella and Burger's Statistical Inference and I stumbled upon this problem:

I haven't been able to get past (a). I've tried using the approximation formulas derived from the Delta Method:

$$E[\frac{U}{V}] \approx \frac{E[U]}{E[V]}$$ $$\mathbb{and}$$ $$Var(\frac{U}{V}) \approx (\frac{E[U]}{E[V]})^{2}\cdot(\frac{Var(U)}{E(U)} - \frac{2Cov(U,V)}{E[U]\cdot E[V]} + \frac{Var(V)}{E[V]})$$ where U,V are random variables. Before I go on, observe that $$\frac{\sum(X_i Y_i)}{\sum X^{2}_i} = \beta + \frac{\sum(X_i \epsilon_i)}{\sum(X^{2}_i)}$$ Approximating our expectation, we obtain $$E[\beta + \frac{\sum(X_i \epsilon_i)}{\sum(X^{2}_i)}]=\beta$$ since $X_i$ and $\epsilon_i$ are independent of each other and $E[\epsilon_i]=0$. Now, if I proceed the following, I get variance of 0 using the approximation formula I have up top: $$Var(\beta + \frac{\sum(X_i \epsilon_i)}{\sum(X^{2}_i)})=Var(\frac{\sum(X_i \epsilon_i)}{\sum(X^{2}_i)})\approx 0$$ which seems remarkably unlikely. Thus, I am wondering if it is possible to have the following approximation given the independence of our samples:

$$Var(\frac{\sum(X_i \epsilon_i)}{\sum(X^{2}_i)})\approx\frac{Var(\sum(X_i \epsilon_i))}{Var(\sum(X^{2}_i))}$$

If this is indeed possible, would someone be kind enough to give an explanation as to why?