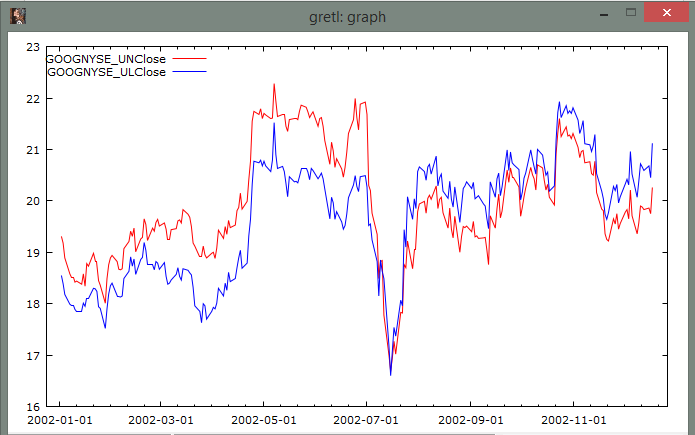

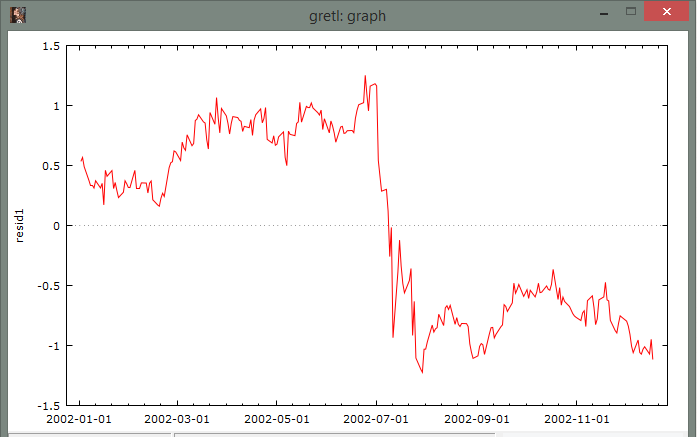

I have two series of daily close prices for UN and UL from 01/02/2002 to 12/31/2002. Both are for Unilever Co. When I conduct the Engle-Granger cointegration test, the MacKinnon $p$-value is high, meaning no cointegrating relationship. However, just by looking at a graph of the two series for that particular period, there appears to be a strong cointegrating relationship.

Does this happen because the UN series crosses over the UL series, causing the residuals from OLS on prices to appear nonstationary?

Below are graphs of the UN and UL close prices and the residual plot.