This seems to be a discrete optimization problem, where you have integer (some of the decision variables / parameters are discrete) constrains on the decision parameters. Comparing to continuous optimization, discrete optimization is much harder to solve: many continuous optimization problems can be solved in $P$ time but most real world discrete optimization problems are $NP$.

If your problem is not in large scale, you can run a brute-force search. For example, if you have $10$ parameters and each parameter has $3$ possible values, the search space is $3^{10}=59049$, which can be done in seconds with modern computer. On the other hand, please note, the search space grows exponentially, if you have $20$ parameters, the brute force is not feasible.

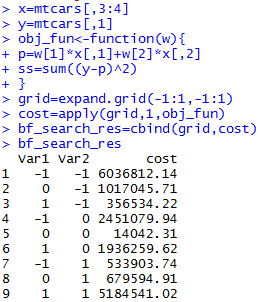

When I say search, I mean, try different configurations of parameters and calculate the loss/objective function. (for example, squared loss in regression). Check for the configurations with lowest loss. Here is an example on mtcars data with $2$ parameters, each of them takes $\{-1,0,1\}$. In this toy example, the optimal solution is $(0,0)$, and has minimal loss of $14042.31$.

As mentioned earlier, if you have more parameters, then, such approach is not feasible. You may want to do two things.

Integer programming one will give you exact answer with high computation cost, and local search is fast, but may give you sub-optimal answer. Each one is a huge topic you can explore and I think it is hard to explain them in detail here.

Edit: as Mark mentioned in the comment, comparing to general discrete optimization problem, the problem has a special structure: the problem is the objective function is quadratic, therefore Mixed Integer Quadratic Programming (MIQP) software can be used. In addition,

Another option would be to solve this as a (mixed) integer Second Order Cone Problem (SOCP), which may or may not be easier (faster) to solve, but requires more knowledge to formulate.