I am studying time series using regression analysis. I know that when using time series data the assumption that the errors are independent cannot be satisfied.

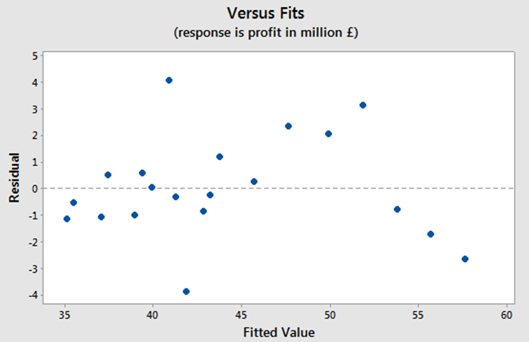

However, analysing the residual plot:

In my opinion, it does not have a positive autocorrelation because I cannot see a cyclic pattern. Also, it does not show a negative autocorrelation.

I think that there is a random pattern and it indicates that there is no autocorrelation or little autocorrelation.

I did a Durbin-Watson test to confirm the above ideas and the value for the test is 2.349. It is greater than 2 but very close to 2, so I assumed that there is no autocorrelation.

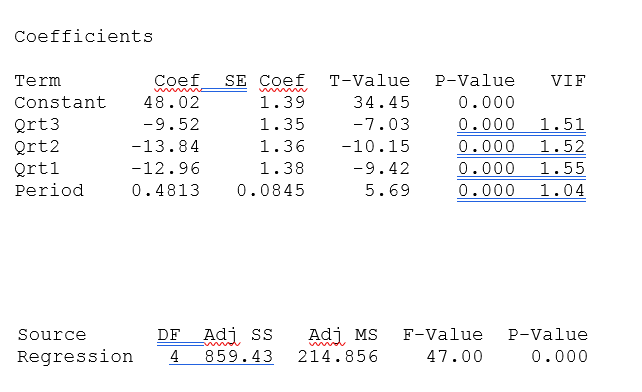

Additionally I checked that the p-values for the coefficients are very small, less than 5%. It means that they are all significant.

Also, the value for the F-test and p-values shows that the model is significant

All these, show that autocorrelation is not a problem in this case and that the assumption that the errors are independent are not being violated. However I am confused because I am using time series data where I used dummy variables for seasonality and according to what I read this assumption is not satisfied when using time series but in my case I think that there is no autocorrelation.

Can anyone help me on this?

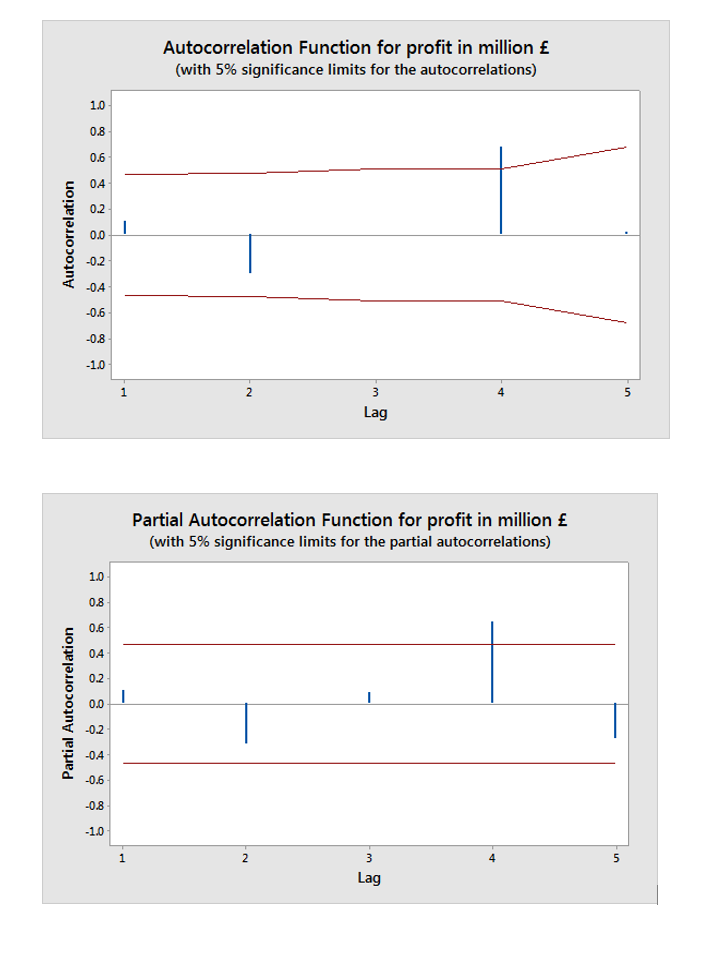

I edited my question to add the following plots of the ACF and PACF: