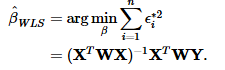

I am trying to manually calculate beta-coefficients using Weighted Least Squares, which are given by:

X should comprise only one variable and the coefficients should include an intercept. I tried it as follows:

set.seed(1)

x = as.matrix(mtcars$wt)

y = as.matrix(mtcars$mpg)

w = runif(length(x))

(t(cbind(1,x)) %*% diag(w) %*% cbind(1,x))^(-1) %*%

t(cbind(1,x)) %*% diag(w) %*% y

This leads to:

[,1]

[1,] 38.92461

[2,] 11.52764

However, the lm-Funktion leads to different results:

lm(y~x, weights = w)

Call:

lm(formula = y ~ x, weights = w)

Coefficients:

(Intercept) x

37.896 -5.437

I am quite sure it must have something to do with the cbind(1,x)-part, as (t(cbind(x)) %*% diag(w) %*% cbind(x))^(-1) %*% t(cbind(x)) %*% diag(w) %*% y leads to the same results as lm(y~x -1, weights = w). Does anyone see what I did wrong while trying to calculate the coefficients manually?