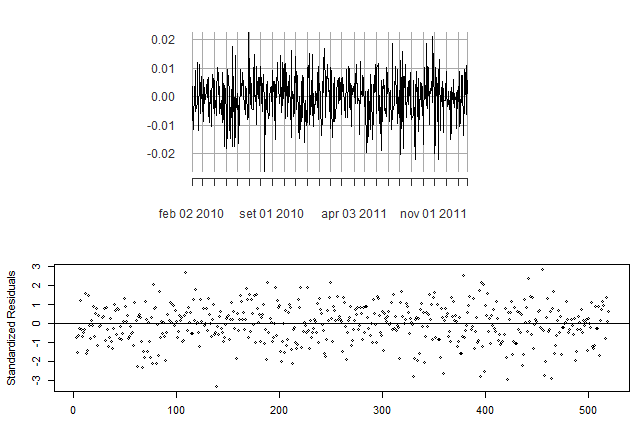

I'm not sure about the presence of a GARCH effect in this first differenced series. What do you suggest? I've fitted an ARIMA(0,1,0), so the original series is a random walk. I'm working with eurusd exchange rates.

Here you can found the initial plots https://ibb.co/m80N8H and here the squadre residuals of ARIMA(0,1,0) plus Mcleod Li test. https://ibb.co/dOgdbS . I've tried also an ARIMA(3,1,0) but it seems the original series is a random walk.