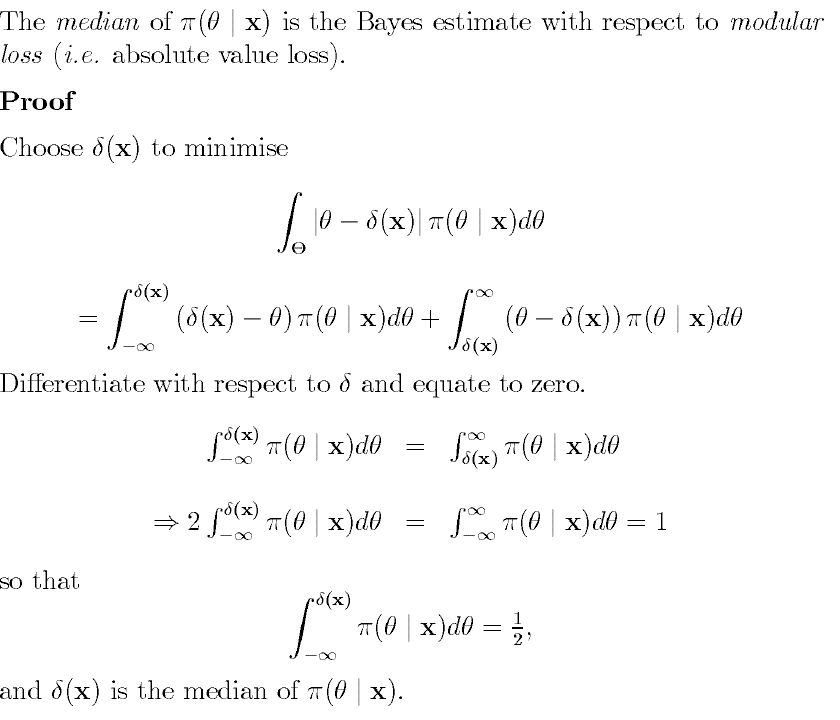

It is always argued that the posterior median is the Bayes estimate associated to the absolute loss function. The proofs I have come across rely on differentiating the conditional Bayesian risk and equating this to zero. However, this shows that this is an inflection point, but not that it is a minimum. How can one prove that the posterior median indeed minimizes the Bayesian risk?

Most, if not all, textbooks just go next level and just leave it as an exercise to the poor reader.