First, to address the issue of bell-shaped predictive values. This will be a heuristic explanation, to say the least. Let's take a linear regression as our "example" case. If you think of the predictor variables as being drawn from some 20+ - dimensional probability distribution (more on the "+" later), a prediction from a linear regression can be thought of as a weighted average of 20+ random variables... the distribution of which, under a wide range of conditions, will tend towards Normality as the number of random variables goes up. Hence the bell-shaped curve.

The "+" is present because, from a numerical standpoint, a categorical variable with 6 levels is equivalent to 6 binary variables (which, obviously, are not independent.) Note I'm not claiming that these 6 binary variables contribute to the asymptotic Normal distribution to the same degree as a continuous variable would.

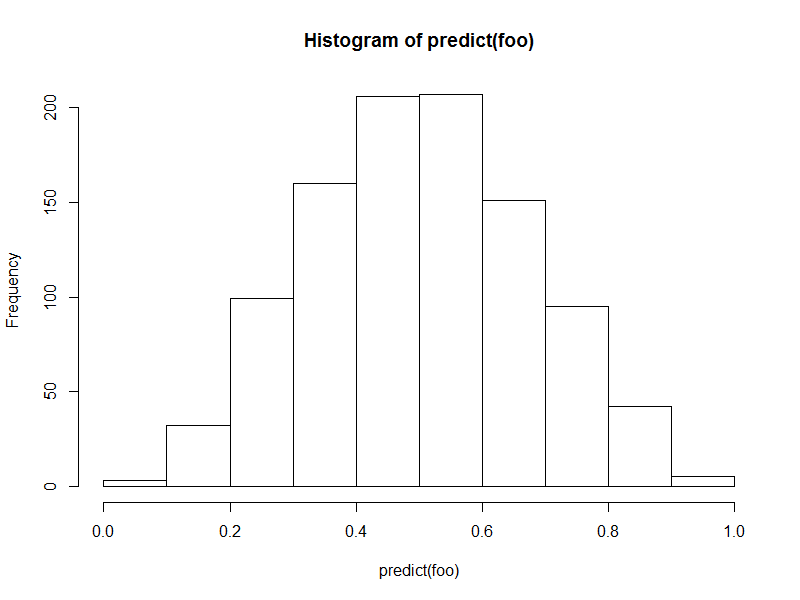

Insofar as other methodologies all have a "weighted average" flavor to them, something similar will occur, though mediated by the actual calculations involved. Here's an example using random forests; I have 10 predictors, independently distributed $U(0,1)$, and the target variable $y$ is the normalized rank of the sum of the square roots of the 10 predictors (so $y$ is in (0,1]).

U <- as.data.frame(matrix(runif(10000),1000))

y <- rowSums(sqrt(U))

U$y <- rank(y)/length(y)

foo <- randomForest(y~V1+V2+V3+V4+V5+V6+V7+V8+V9+V10, mtry=4, data=U)

hist(predict(foo))

As you can see, the bell-shaped histogram of the predicted values occurs in other contexts than yours.

Second, converting to a more uniformly-shaped prediction. One way would be to rank the predicted values from 1-38000, then scale down to 0-1, just as with the original rank-valued target variable.

Here's what happens when we continue the above example in this vein:

> u.predict <- rank(predict(foo))/length(predict(foo))

> mean((u.predict-U$y)^2)

[1] 0.007450796

> mean((predict(foo)-U$y)^2)

[1] 0.01875836

The mean squared error of the ranked predictions has decreased by a factor of roughly 2.5 relative to the "raw" predictions. My guess as to why this works, which I admit surprised me, is that the original variable is a normalized rank, not a true interval-valued variable (i.e., 0.002 is not 2 times 0.001, really,) and the ranked predictions are in a way correcting for the fact that the estimation procedures are all assuming that they are.