I am using a regression model that produces non-normal forecast errors. To produce different scenarios, I need to simulate the model error, I can bootstrap from historical errors, however, because the number of simulations I need might be more than then historical errors, I wonder if there is a way to get the empirical distribution and bootstrap from that to get more variety in sampled errors (for example getting the interpolation between different historical errors.)

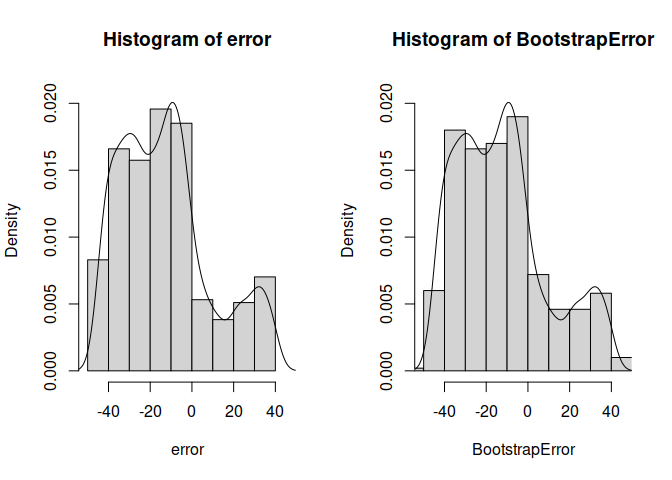

Here is an example of nonparametric error distribution.

x1 = runif(min = 1, max = 40, n = 100)

x2 = runif(min = -45, max = 0, n= 370)

error <- c(x1, x2)

BootstrapError <- sample(x = error, size = 500, replace = T)

I appreciate sharing your ideas.