I'm running a monte carlo simulation of a financial instrument, and I'm trying to understand why the final balance of each simulation gives me a skewed distribution rather than a normal distribution (given that I'm sampling out of a normal distribution using np.random.normal).

I assume average monthly return of 1%, standard deviation of 4 and projecting for 60 months. My method is to sample from a normal distribution using np.random.normal and create an array out of that. Then I take a starting balance and multiply that over each element and create a list. I append 500 of these simulations to a dataframe:

df = pd.DataFrame()

for i in range(1, 501): #500 simulations

pct = np.random.normal(loc = 1, scale = 4, size = 60) #mean 1%, std 4%, 60 month period

df['Simulation_' + str(i)] = balance_updater(100000, pct)

where the function balance_updater creates a list that documents every iteration (in this case, starting balance = 100000), coded as the following:

def balance_updater(starting_balance, pct):

balance = starting_balance

balance_list = []

for i in range(len(pct)):

balance = (balance + balance * pct[i] / 100).round(2)

balance_list.append(balance)

return balance_list

Then when I plot via:

sns.distplot(df.iloc[-1, bins=30) #Plot final balances only

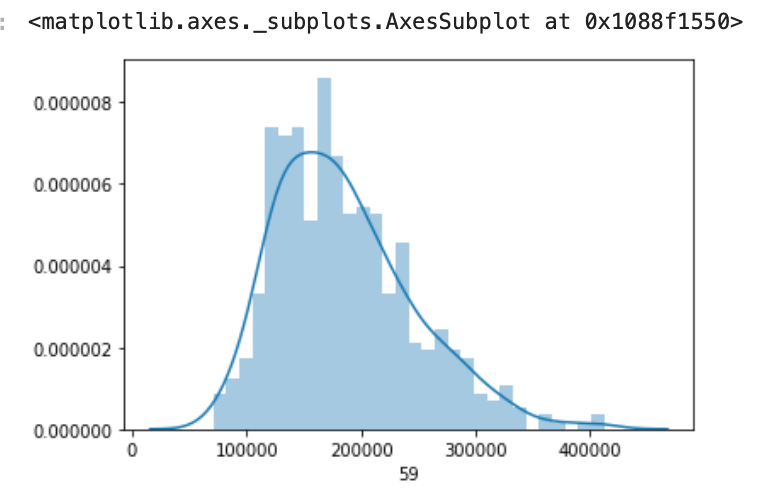

This is the resulted graph.

I expected this to be normally distributed but we can see it slightly skewed to the right.

What puzzles me more is that if I were to project for a longer period of time (let's say 30 years = 180 months) the results become even more skewed:

I'm trying to understand why a longer projected period produces a more skewed graph, which violates my understanding of the central limit theorem with more sampling (360 vs 60).

Thank you.