I have two different samples I need to test if they are drawn from the same population distribution. The two samples are of the volatility of an asset that I simulated. Since the data is simulated I know that both samples have the same data generating process. The only difference between the two samples are the days that I am using from the simulation.

A summary of the two samples is given below. It is also important to note that since this is simulated data the sample size is quite large. I have 249,281 observations in sample 1 and 254,453 in sample 2.

> summary(Sample1)

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.0128 0.0894 0.1194 0.1367 0.1627 0.9925

> summary(Sample2)

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.0141 0.0950 0.1263 0.1467 0.1724 1.1435

When I apply the Kolmogorov-Smirnov test the results reject the null hypothesis that the two samples are drawn from the same population.

ks.test(Sample1,Sample2)

Two-sample Kolmogorov-Smirnov test

data: Sample1 and Sample2

D = 0.053089, p-value < 2.2e-16

alternative hypothesis: two-sided

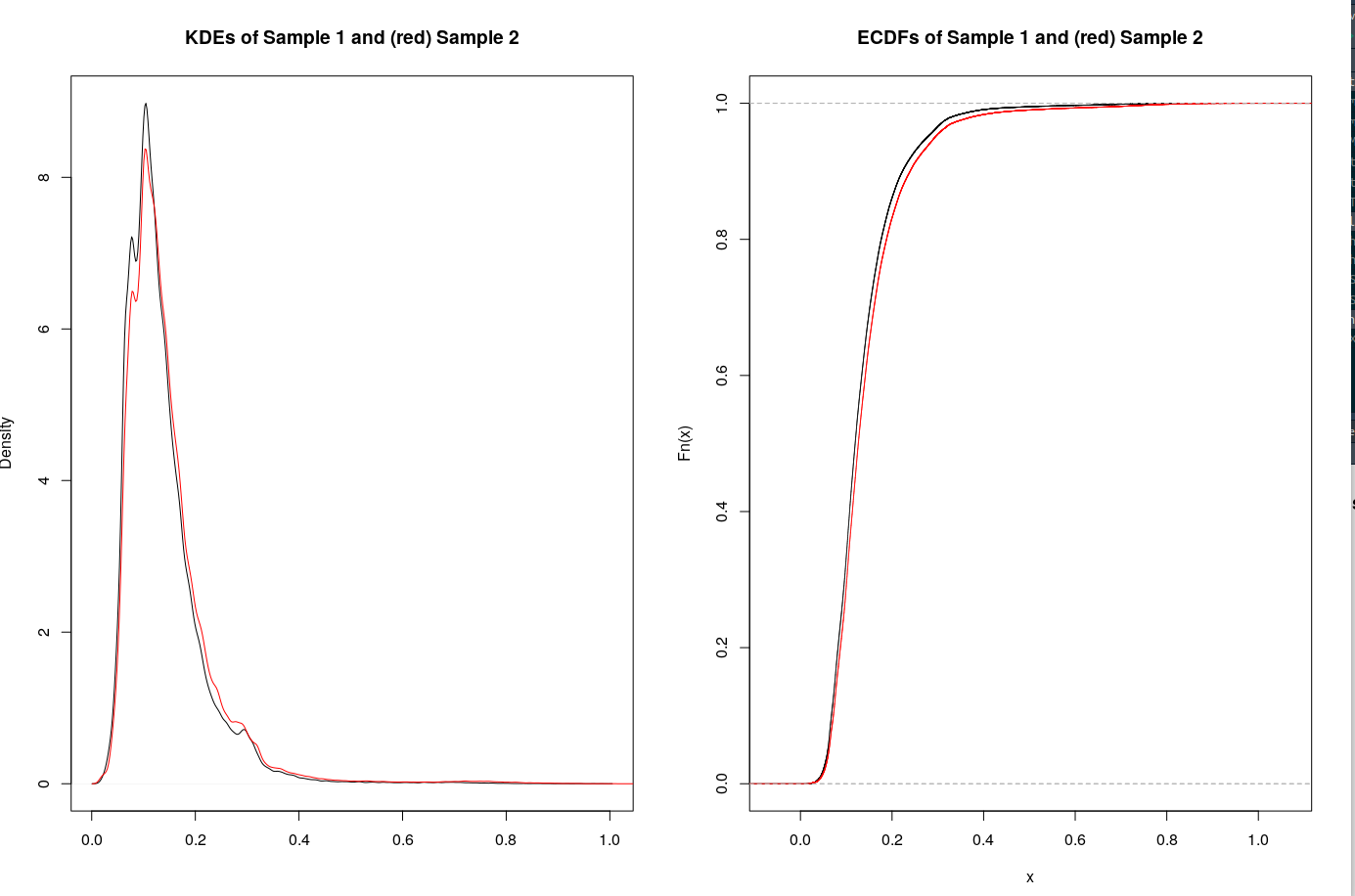

However if I plot the kernel approximation of the two different density functions and the CDF both of the samples appear to be from the same distribution. A copy of the plots is given below.

How is it possible that the two samples come from different distributions if they have the same data generating process? Am I missing interpreting the results from the KS test? Is there another test that I should be apply?

How is it possible that the two samples come from different distributions if they have the same data generating process? Am I missing interpreting the results from the KS test? Is there another test that I should be apply?