I'm dealing with binary events and I've got people guestimating the chance that they occur. I'd like to translate someone else's guestimate into a probability distribution representing my belief about the true probability. This is called a posterior distribution right? basic bayesian stats?

I imagine I want a distribution which looks roughly normal and fairly wide for a forecast of 0.5 but becomes increasingly skewed for forecasts closer to the tails.

At the moment I don't have data, I'm just doing exploratory simulations. I'm looking for an R function to that takes a probability forecast and outputs a probability distribution with reasonable parameters.

Added: For my purposes, even a very very rough approximation will do. Its perfectly fine if statistically literate people roll their eyes. But R code to get me started would be greatly appreciated.

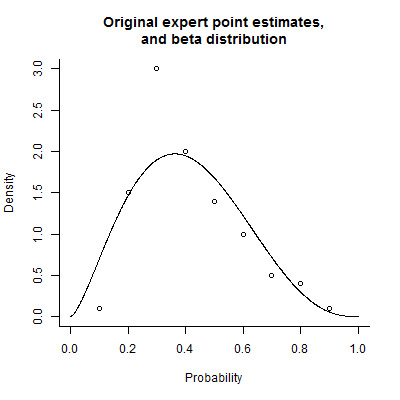

Added: I fear I still wasn't clear enough about my weird situation. My "expert" is actually only telling me their single best guess for the binary event occurring. I've seen (but not recorded) a bunch of the expert's past best guesses so I have an intuitive sense for what the true distribution of the probability of the events are conditional on an expert's best guess. So I guess I need to play around with beta distribution parameters. Find the parameters that I like for a 0.5 forecast, a 0.25 forecast, 0.1, 0.05 and 0, and then find some smooth functions to interpolate my guesses at what the parameters alpha and beta should be for the space between?