I am trying to fit a regression model in which the dependent variable is a continuous positive variable (costs, no zero costs). In literature I often read that considering the lack of negative values, a ordinary least square regression is not appropriate. Generalized linear models with for example a Gamma distribution is often recommended over OLS. This leads to the following questions

- To get unbiased regression estimates the assumptions of the OLS do not specify anything regarding the specification of the error distribution. Hence, even though the errors are clearly not normally distributed, an ordinary least square regression would still provide you with unbiased estimates. In case the sample is sufficiently large and the errors are homoscedastic (or use robust standard errors when they are not), why would one prefer a glm?

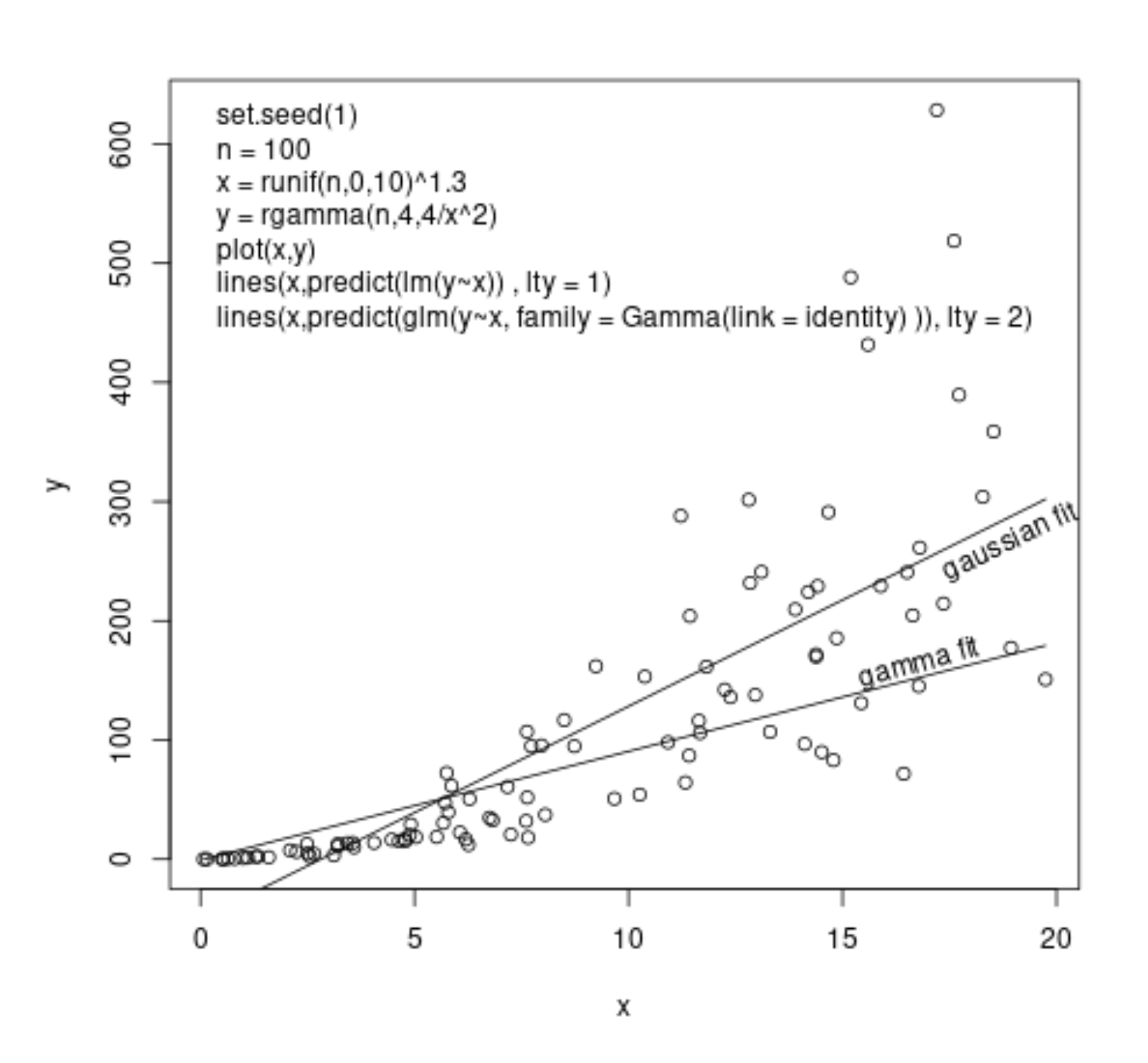

- I fitted a GLM with a gaussian family as well as with a Gamma distribution, with both the identity link function as well as the log link function. However, the regression estimates for the different families (with the same link function) are substantially different (even when considering robust standard errors). Given that both should give unbiased estimates why would this happen?

- Some papers say that fitting non negative data with an identity link function is inappropriate as it might lead to negative predictions. However, when given the regression coefficients negative predictions are impossible would this still be argument? I am asking as I am interested in the additive effect of my variables. Moreover, the AIC of the Gamma regression with the identity link is the lowest. The error plots for the gamma regression with the identity link also look superior compared to the others.