I am having trouble understanding if my data is cooked, and how bad, based on post-estimations for coxph. The regression and the cox.zph test is below. Based on the post-estimation, this looks bad because the values are significant and they are very different from 0.

However, I have over 2million observations. And this answer said that sometimes with lots of observations, the post-estimation is just significant because almost everything is statistically significant when you have 2million observations.

On the other hand, with 5001 events it's quite possible to find a statistically significant non-proportionality that is of little practical significance. As Therneau and Grambsch put it in Section 6.5 of their book:

A "significant" nonproportionality may make no difference to the interpretation of a data set, particularly for large sampIe sizes.

They go on to describe a study with 771 events, in which the cox.zph() test gave significant p values for 2 out of 3 predictors with Global p = 1.95e-09. This result might be taken to require time-dependent estimates of each coefficient, β^(t), instead of a time-independent estimate β. Examining plots of scaled Schoenfeld residuals over time, however, led to the following conclusion about the association between age and risk of death:

There is a profound effect of age on the risk of death, and the test shows the effect to be significantly nonproportional. However, the smoothed residual plot shows that the variation in β^(t) is small relative to β^.

So these are my results:

Call:

coxph(formula = Surv(matt_tmove_cen, matt_moved_cen) ~ matt_ncdem +

flood_risk_simple, data = matt_timeadd)

coef exp(coef) se(coef) z p

matt_ncdem 0.16587990 1.18043132 0.01716598 9.6633 < 0.000000000000000222

flood_risk_simple -0.18664060 0.82974189 0.01646413 -11.3362 < 0.000000000000000222

Likelihood ratio test=132.42 on 2 df, p=< 0.00000000000000022204

n= 2482803, number of events= 281028

matt_sfit0 %>% cox.zph()

chisq df p

matt_ncdem 21.2942 1 0.0000039392

flood_risk_simple 14.0987 1 0.00017347

GLOBAL 21.5385 2 0.0000210366

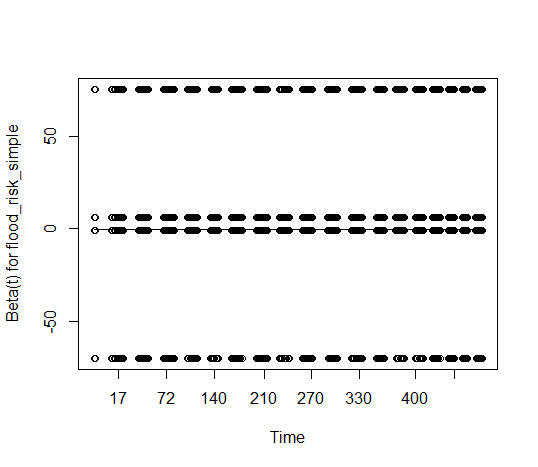

And here are the graphs I get from the following post-estimation code:

matt_sfit0 %>% cox.zph() %>% {zph_result <<- .} %>% plot(var=1, resid = TRUE)

matt_sfit0 %>% cox.zph() %>% {zph_result <<- .} %>% plot(var=2, resid = TRUE)

Making things a bit more complicated, when I turn on the resid option (which I don't actually know what this does), there's this weird split between the variables. I don't know if this is because the variables are binary (?), or really how I'm supposed to interpret all the dots sorting themselves in this way. Would love help interpreting both sets of plots.

matt_sfit0 %>% cox.zph() %>% {zph_result <<- .} %>% plot(var=1, resid = TRUE)

matt_sfit0 %>% cox.zph() %>% {zph_result <<- .} %>% plot(var=2, resid = TRUE)