The purpose of my study is to understand if changes in environment policy or changes in people concerns about climate change affects volatility or if they can help in the prediction of volatility. In this case I check the volatility of the Dow Jones from January 2003 to June 2018. In order to do it, I’m using a GARCH(1,1) model with the addition of a covariate. The covariates I chose are two indeces, one called EnvP, which measures the salience of US environmental policy, and the other one called Media climate change concerns, which captures unexpected increases in climate change concerns. I use the software gretl for my analysis.

Anyway, I got a lot of doubts about how to estimate this model.

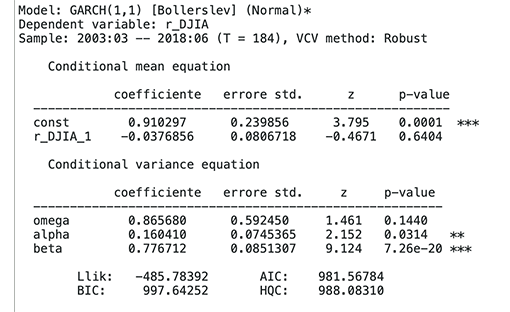

For a start, I estimate a first GARCH(1,1) to give an initial interpretation of the parameters and to use it as a sort of benchmark:

The first doubt I have is: do I have to insert a lag of the returns in the conditional mean equation of the GARCH?

In that case I’d have:

Is there any significant change? Is there a motive I should or shouldn’t insert this lag?

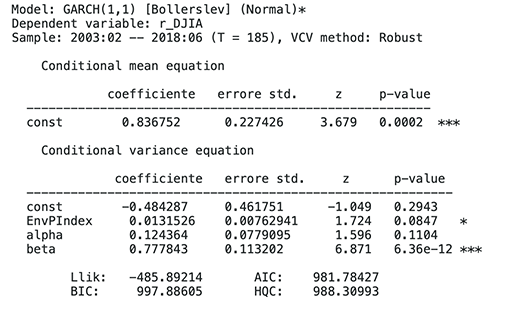

Now, I insert the covariate (EnvP) in the model:

Same model but with the returns lagged(1):

I need help understanding these outputs, to understand if it’s methodologically correct to insert those lags and, in general, if I can say something regarding the aim of my study.

Any help will be very appreciated.