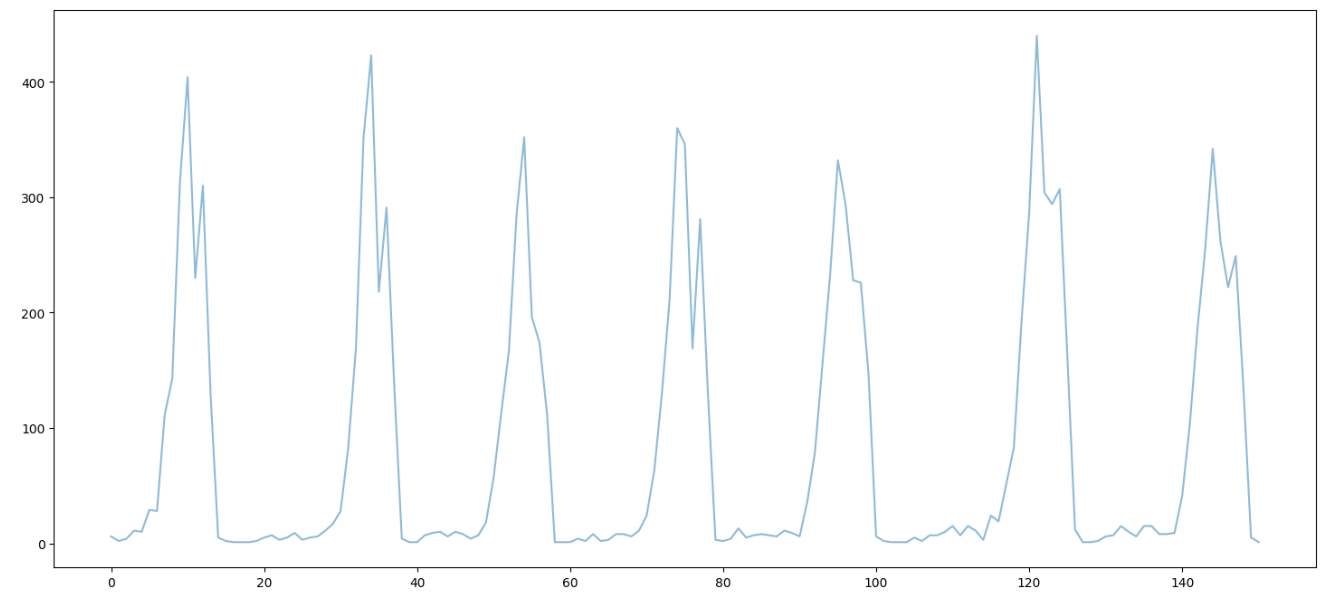

I have a time series which has sequence as follows

Upon eye balling this series , it sounds me a series which has 20 cycles where frequency/counts of event increase from 0 and then decrease after half of its cycle.

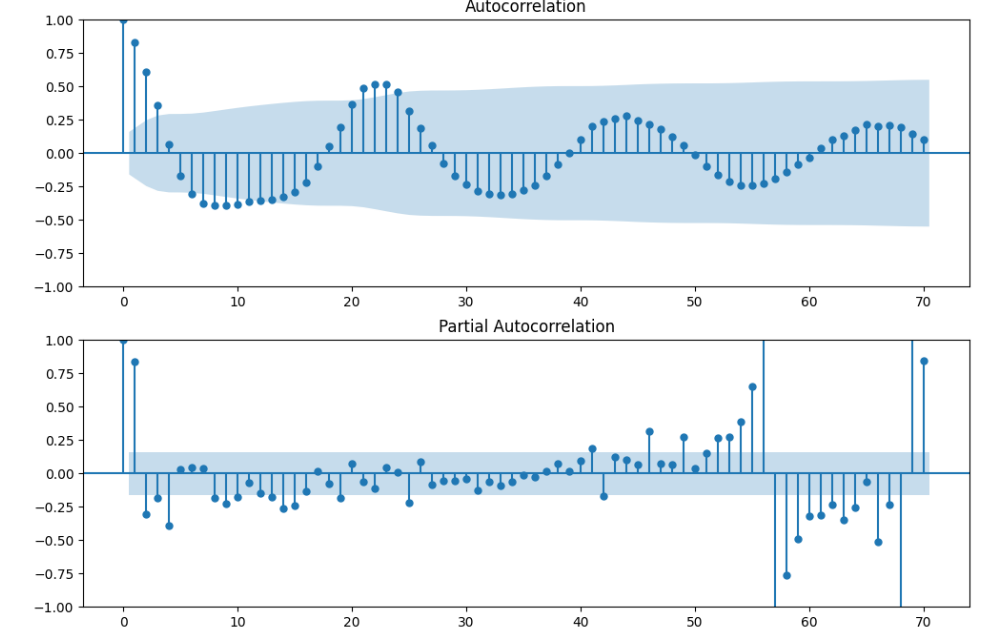

I generated ACF and PACF plot of this series without any transformation (log or differencing)

I am not getting any insights from this ACF and PACF plot for AR and MA order. However , based on my intuition I used 20 AR order for building model without any differencing and MA order

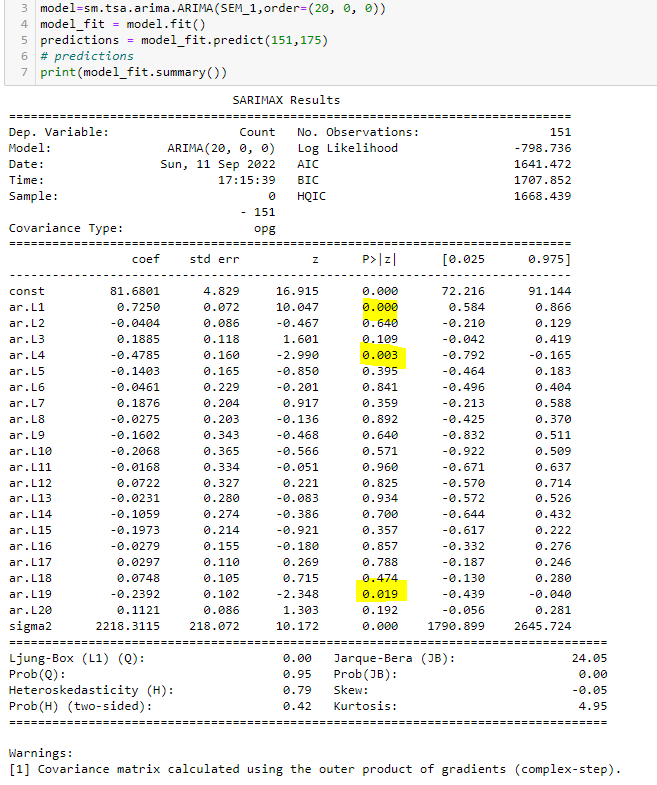

as in model summary lag 1, lag 4 and lag 19 are more significant as they have less than 0.05 value. However , I am going with all 20 lags and forecast for the next period from 151 to 175

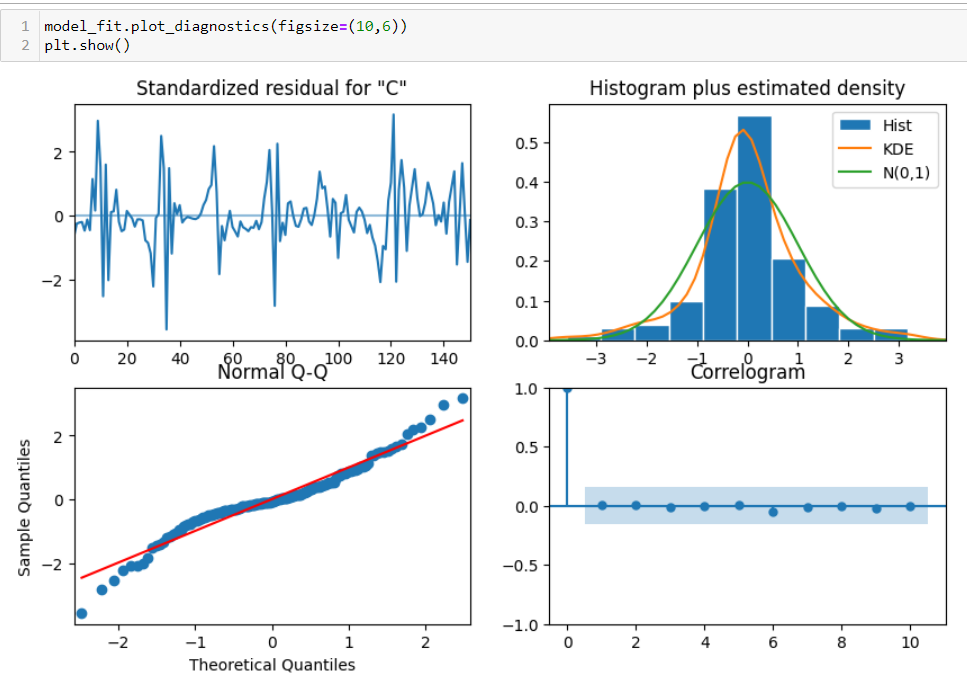

When I check residual plots autocorrelation 4th plot, it does not tell me there is any more improvement required for the model

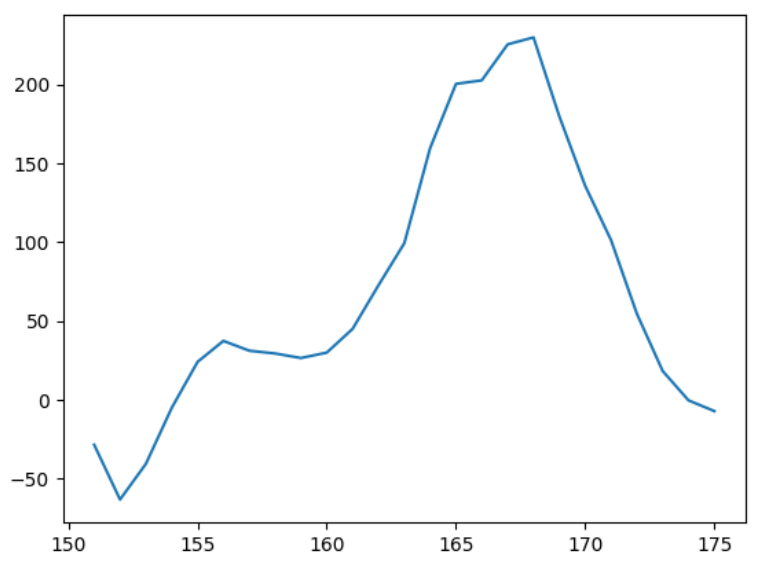

This model giving me almost same cycle and overall more or less same number counts estimated for this forecasted period from 151 to 175.

My confusions are

Can I go with this model for live deployment forecasting?

Why model does not give same number of forecasted counts upon reducing the number of lags, it works best with 20 but when I start to decrease from 20 to 15 or 10 then model forecasting is not expected what business wants?

How can I find AR and MA order for the model using PACF and ACF plot?