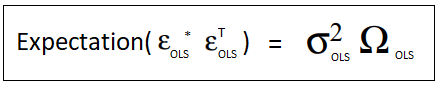

But from variance-covariance of OLS's error - we have already found the Ω.

This is dubious. The postulated model is

$$ \left\{\begin{align}\mathbf y &=\mathbf X\mathbf b +\boldsymbol\varepsilon,\\\mathbb E[\boldsymbol\varepsilon|\mathbf X]&= \mathbf 0,\\\mathbb E\left[\boldsymbol\varepsilon\boldsymbol\varepsilon ^\mathsf T |\mathbf X\right]&= \sigma^2\mathbf \Omega\end{align}\right\}.\tag{GLRM}

$$

One cannot know, in general, beforehand, what the structure of $\bf \Omega$ be. If it can be known, then very well. Otherwise, one must need additional assumptions and structures for estimating the unknown parameters.

If we already have Ω, then Why do we need to estimate Ω

We don't. It is hardly the case that $\mathbf\Omega$ is known; once in a blue moon do we have the complete knowledge of $\mathbf\Omega.$ In case, it is known, symmetric, positive definite, then GLS can be employed to reach the Aitken estimator

$$\hat{\boldsymbol\beta} =\left(\mathbf X^\mathsf T\mathbf \Omega^{-1}\mathbf X\right)^{-1}\mathbf X^\mathsf T\mathbf \Omega^{-1}\mathbf y.\tag 1 $$

(by running another regression as we do in WLS).

As I said, if $\bf\Omega$ is not known, we cannot apply $(1):

$ GLS is not feasible. The unknown parameters that it contains need to be estimated: since there are $n(n+1) /2$ unknown parameters and only $n$ observations, additional structure on the model has to be taken into consideration.