I run a standard GARCH (1,1) model and obtain the following results.

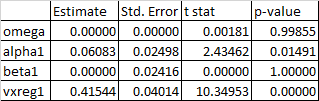

Thereafter, I add an external regressor in the same model and obtain the following results:

The GARCH coefficient (beta1) is zero and the p-value is 1. The coefficient of the external regressor (vxreg1) is 0.415 with p-value of 0.000.

I use the robust standard errors.

How to interpret the result? Should I concur that the external regressor reduces/removes volatility contemporaneously?