I am trying to understand the validity of bootstrap percentile confidence intervals and I have stumbled on the following from these slides:

Suppose we want to set a 95% confidence interval on $θ$, the true parameter value for the real population $f$ . And suppose we take $M = 1000$ bootstrap samples. The bootstrap method suggests that approximately 95% of the time, the true parameter value for $\hat{f}_n$ falls between the 2.5th percentile of the bootstrap samples and the 97.5th percentile. (Recall percentile definitions in Lecture 2.)

Since $\hat{f}_n$ converges to $f$ , the correct confidence interval for the true parameter for $\hat{f}_n$ should converge to the correct confidence interval on the true parameter for $f$ .

Since in boostrapping we assume that our (original) sample is a good approximation for the population, sampling with replacement from this samples allows us to approximate the theoretical sampling distribution. Nevertheless, for the bold statement to be true it must be the case that the 0.025th and 97.5th percentiles of the theoretical sampling distribution contain the true population parameter. Is this always true? It holds for sample mean but what about other statistics?

EDIT

I am adding the following figure to better express my confusion. The following section is only about the theoretical sampling distribution.

Theoretical sampling distribution

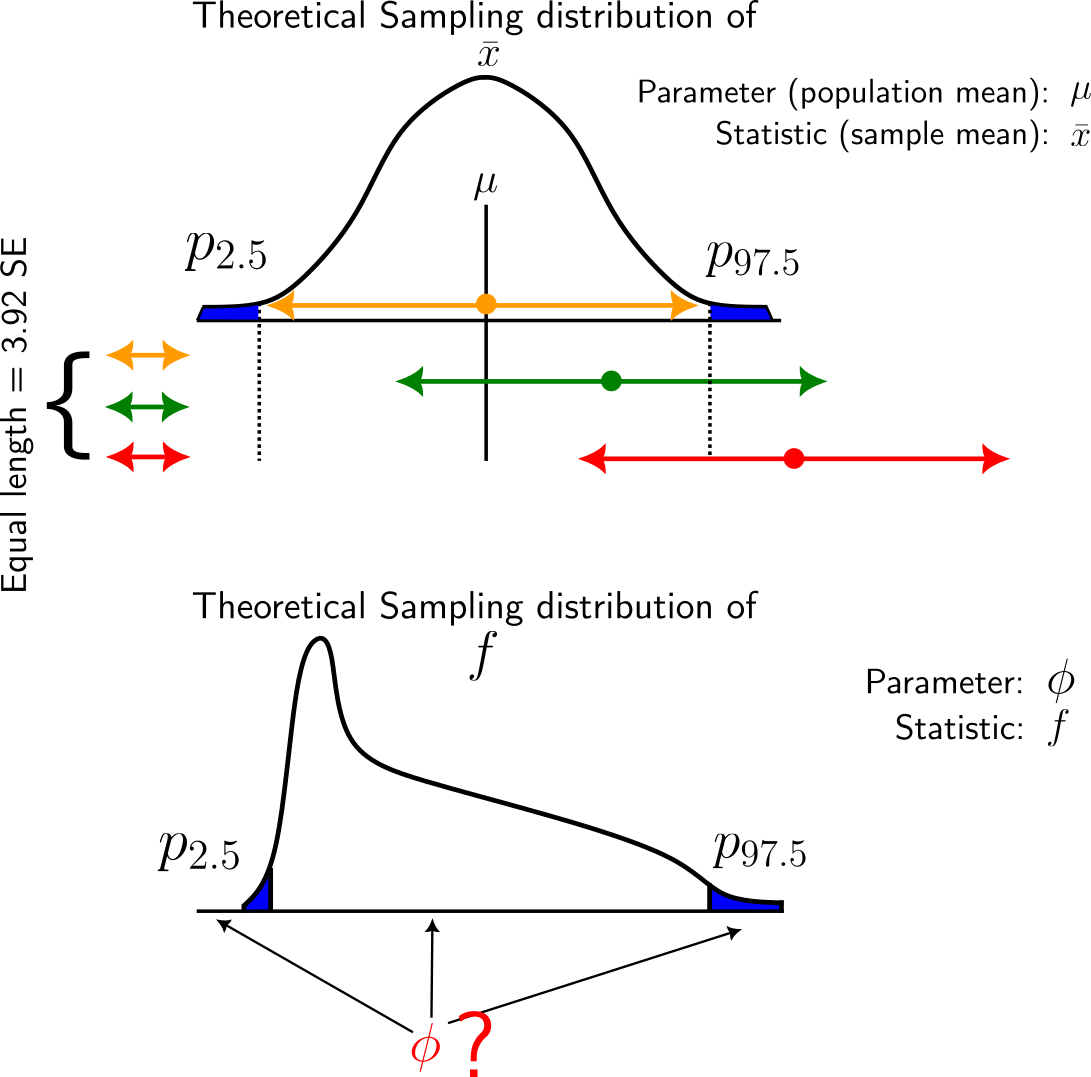

In top is the sampling distribution of the sample mean. In this case, the population mean $\mu \in [p_{2.5}, p_{97.5}]$, where $p_{2.5}$ and $p_{97.5}$ are the 2.5th and the 97.5th percentiles, respectively.

In bottom, is the sampling distribution of a statistic called $f$ (nothing specific, an arbitrary statistic).

- Is it necessary that the true population parameter $\phi \in [p_{2.5}, p_{97.5}]$? Could $\phi$ lie outside this interval, either left from $p_{2.5}$ or to the right of $p_{97.5}$?

Confidence intervals (CI)

Suppose we want to construct the 95% CI for the population mean. Well, we can sample from our population a sample $S = \{x_1, x_2, \ldots, x_n\}$ calculate the sample mean $\bar{x}$ and report the 95% CI as:

$$ \bar{x} \pm 1.96 \cdot \text{SE} \tag{1} $$

where SE is standard error (the standard deviation of the sampling distribution).

Of course, we don't have access to the standard deviation of the sampling distribution and as such we can approximate it with the standard deviation of the sample $s$ (wheter this is a good approximation or not is another story). Assuming that this approximation is valid, then the 95% CI:

$$ \bar{x} \pm 1.96\cdot s \tag{2} $$

If we repeat the same procedure ad infinitum, i.e. collect a sample, calculate its mean and standard deviation, and report the interval based on Equation 2 then, 95% of the times these intervals will contain the true population mean. For example, the interval constructed from the green sample contains the true population mean while the red doesn't.

Alternatively, we could also report as 95% CI the interval $[p_{2.5}, p_{97.5}]$. As said before, we don't have access to the sampling distribution, and as such we can approximate this interval with the percentile values from our sample.

Since we can report a confidence interval by just using our sample, why bootstrapping the sample at all? Is that because bootstrapping a sample gives a better approximation to the sampling distribution (assuming the sample is representative of the population)?

With regards to the bold statement: I understand that a 95% CI doesn't necessarily contain the true parameter. The 95 percent of them contain it while the other 5 percent don't. My confusion is the following: if the population parameter of interest can be outside $[p_{2.5}, p_{97.5}]$ of the sampling distribution (see bottom figure), how confidence intervals based on percentiles are valid at all?