How can I compress a time series so that any large % changes are compressed and so that all the values fall within a a specific range?

At the moment, I have built in a rule that caps the change at 0.05 or 0.25 whenever the absolute % change is greater than 0.25 or smaller than 0.05. Then, if the new adjusted result is still greater than my upper limit (0.2) or smaller than my lower limit (0.36), I fix the result at 0.2 or 0.36.

Is there a way I can do this using some kind of transformation function instead? Any resources or suggestions would be much appreciated.

Purpose: This is for a business use case. We want to use KPI A as a proxy for another KPI B that we cannot always track. KPI A is a lot more volatile than KPI B and we therefore want to try and reduce the volatility of KPI A according to our expectations for KPI B. (I appreciate that this is not the most scientific way of doing this but our business wants a quick solution (even if it is hacky).

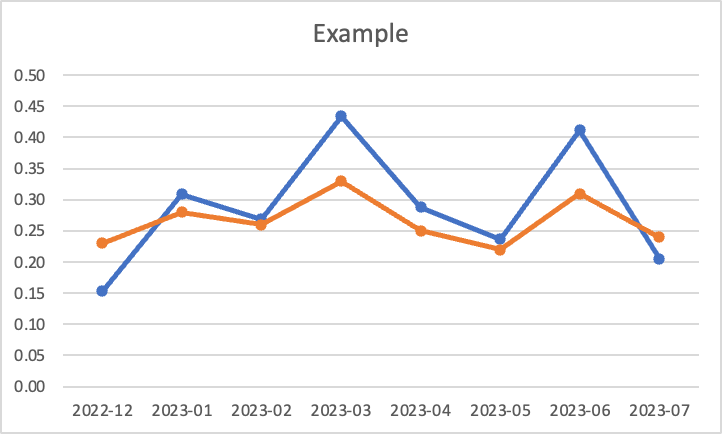

Example: I want the more volatile blue line to look more like the orange line.