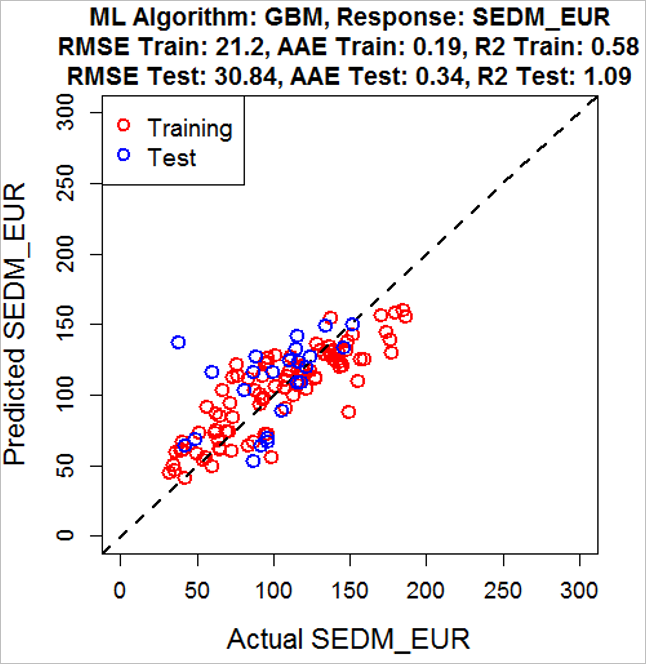

The big issue I see is that the paper reports $R^2>1$. Anyone can calculate anything they want and call it anything they want. However, $R^2$ has a somewhat standard meaning as a value that is capped at one, regardless of the multiple typical ways of calculating $R^2$, such as those discussed in my question here. That is, no matter which of those calculations discussed at the link that is used, the value cannot exceed one.

However, this article reports a value exceeding one. I see a few possibilities.

Simple typographical error: the paper contains the wrong value, perhaps because the intern typed $1.09$ instead of the $0.19$ the investigator meant to be reported

Coding error that results in a variable being called r2 yet being calculated in a way that is different from what is meant

Use of a non-standard calculation of $R^2$

From the remark that the author has computed R2 = SSR/SST, the third option seems to be the culprit.

As I show here, the total sum of squares $\overset{N}{\underset{i=1}{\sum}}\left(

y_i-\bar y

\right)^2$ can be decomposed.

$$

y_i-\bar{y} = (y_i - \hat{y_i} + \hat{y_i} - \bar{y}) = (y_i - \hat{y_i}) + (\hat{y_i} - \bar{y})

$$

$$

( y_i-\bar{y})^2 = \Big[ (y_i - \hat{y_i}) + (\hat{y_i} - \bar{y}) \Big]^2 =

(y_i - \hat{y_i})^2 + (\hat{y_i} - \bar{y})^2 + 2(y_i - \hat{y_i})(\hat{y_i} - \bar{y})

$$

$$

\sum_i ( y_i-\bar{y})^2 = \sum_i(y_i - \hat{y_i})^2 + \sum_i(\hat{y_i} - \bar{y})^2 + 2\sum_i\Big[ (y_i - \hat{y_i})(\hat{y_i} - \bar{y}) \Big]

$$

Let's write this more briefly as $

SSTotal=SSRes + SSReg + Other

$, better yet, as $SST = SSE + SSR + Other$.

When $Other = 0$, $SST - SSE = SSR$, and $1 - SSE/SST = SSR/SST$. However, it is often the case that $Other \ne 0$, and there is not even a requirement for a particular sign of $Other$. That is, $Other >0$ and $Other <0$ are both possibilities. Even using a linear regression with a least squares fit (the venerable "OLS"), out-of-sample, all bets are off about the sign of $Other$, even setting aside the particular $\bar y$ used in its calculation. Therefore, there is not a certain relationship between a reasonable $R^2$ calculation in $1 - SSE/SST$ and $SSR/SST$, and we could wind up with $SSR/SST > 1 > 1 - SSE/SST$ and report $R^2 = SSR/SST > 1$, despite the $SSR/SST$ lacking much motivation and lacking properties we want our $R^2$ value to have (such as being bounded above by one).

I think the authors noted the equivalence of $1 - SSE/SST$ and $SSR/SST$ in some cases and assumed it would hold in more generality than it does hold, using $SSR/SST$ as a shortcut to calculate $1 - SSE/SST$, only to have it turn out that their assumed equivalence does not hold.