For a discrete Brownian motion with an absorbing state we can express the distribution of the position as a linear sum of two binimial distributions as described here when the odds for +1 and -1 steps are 1:1, and here for the more general case when the odds are not equal.

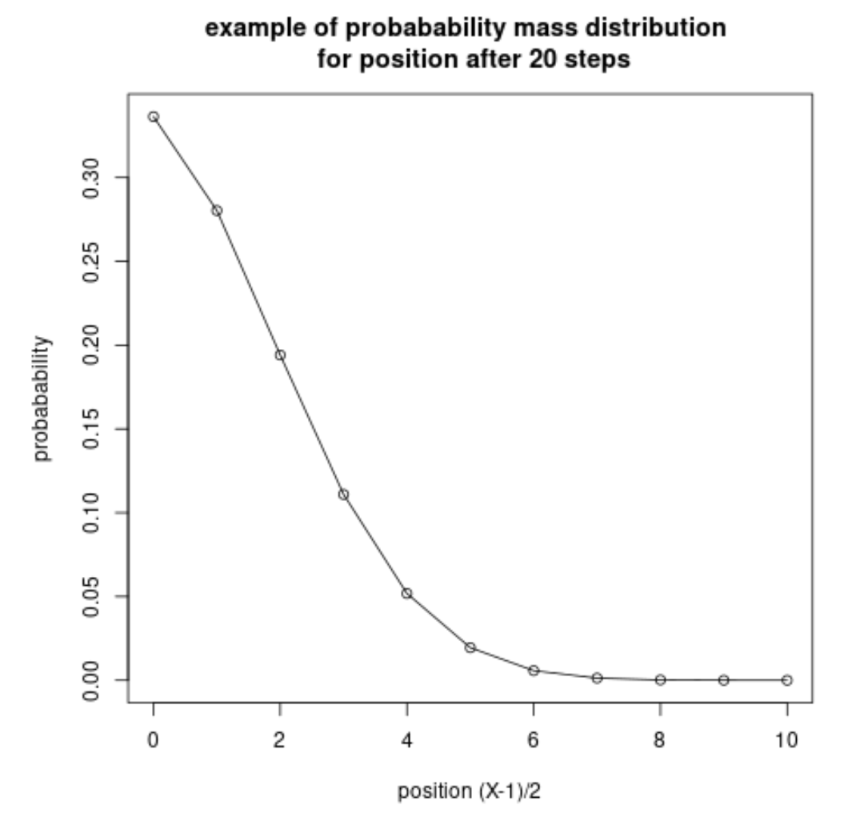

How is the situation for a discrete Brownian motion with a reflecting wall?

Say we describe the position at time $t$ as $X(t)$ with starting position $X(0) = 1$. With probabability $p$ we make a step forward $X(t+1) = X(t) + 1$ and with probabability $1-p$ we make a step backwards $X(t+1) = X(t) - 1$, except when $X(t) = 0$ in which case we always make a step forward.