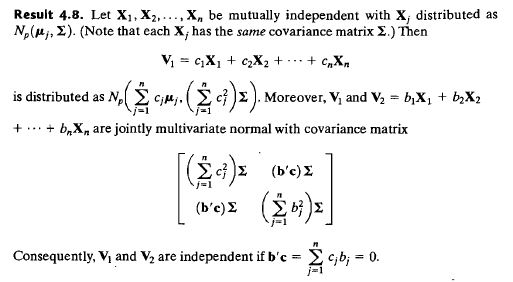

Let $X_1,...,X_4$ be independent $N_p(μ,Σ)$ random vectors. Let $V_1,V_2$ be such that $$V_1=(1/4)X_1-(1/4)X_2+(1/4)X_3-(1/4)X_4 $$ $$V_2=(1/4)X_1+(1/4)X_2-(1/4)X_3-(1/4)X_4 $$

I need to find the marginal distributions of $V_1$ and $V_2$ and the joint density. Since they are linear combinations of random vectors I do not know the theory behind it to solve this. Any answers will be much appreciated. Thanks