I've searched exhaustively on this forum and elsewhere, and have come across a lot of great material. However, I'm ultimately still confused. Here's a basic, concrete example of what I'd like to accomplish, my approach for doing so, and my questions.

I have a dataset sized 1000 x 51; 1000 observations, each with 50 numeric features and 1 binary response variable marked with either "0" or "1". "0" indicates a response of "not-early," and "1" indicates a response of "early." I'd like to build a single LASSO logistic regression model to predict, on a testing set that does not include response variables, whether each testing observations result in a classification of 0 or 1.

My approach uses the following steps:

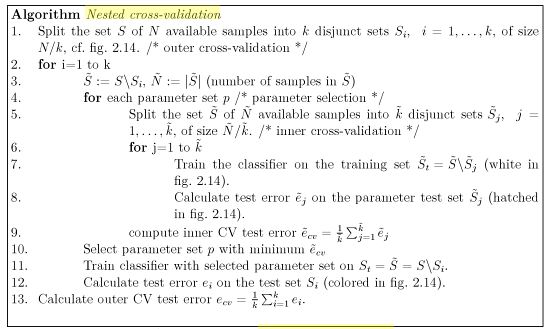

Partition the training data into k = 5 folds, each containing 200 observations. Let's label each fold data_1, data_2, data_3, data_4, data_5.

For k = 1, our train_set_k is comprised of data_1, data_2, data_3, and data_4, and will contain 800 observations. Our test_set_k is comprised of data_5, and will contain 200 observations.

For k = 2, our train_set_k is comprised of data_1, data_2, data_3, and data_5. Our test_set_k is comprised of data_4.

Etc.

For k = 1 to 5, partition train_set_k into k_i = 5 folds, each containing 800/5 = 160 observations. Cross-validate on these k_i = 5 folds to find the optimal setting for the hyper-parameter lambda for our LASSO logistic regression model. Lambda should be a floating point number between 0 and 1.

Question #1: I'm unclear as to what "cross-validate to find the optimal setting for the hyper-parameter lambda" actually entails. In R, I'm using the following code:

model.one.early <- cv.glmnet(x.early, y.early, family = "binomial", nfolds=5, type.measure="auc")..where nfolds = 5 pertains to the k_i = 5 above. In other words, each of the nfolds = 5 folds will contain 160 observations.

From this code, I'm able to output values for: "lambda.min" - the value of lambda that gives the minimum mean cross-validated error, which I assume to mean "gives the maximum mean cross-validated AUC," as I specified type.measure = "auc" above; "lambda.1se" - the largest value of lambda such that error is within 1 standard error of the minimum."

Question #2: What is the above line of code actually doing? How does it compute values of lambda.min and lambda.1se?

Question #3: Which value of lambda (lambda.min or lambda.1se) do I want to keep? Why?

Fit a LASSO logistic regression model to the 800 observations in this fold using hyper-parameter lambda.min (or lambda.1se) as obtained above. Use this model to predict on the remaining 200 observations, using a piece of code like this:

early.preds <- data.frame(predict(model.one.early, newx=as.matrix(test.early.df), type="response", s="lambda.min"))Compute an AUC for these predictions.

Once the above loop finishes, I should have a list of k = 5 lambda.min (or lambda.1se) values, and a list of 5 corresponding AUC values. To my understanding, by taking an average of these k = 5 AUC values, we can obtain an "estimation of the generalisation performance for our method of generating our model." (-Dikran Marsupial, linked here)

This is where I'm confused. What do I do next? Again, I'd like to make predictions on a separate, un-labeled testing set. From what I've read, I must ultimately fit my LASSO logistic regression model with all available training data, using some code like this:

final_model <- glmnet(x=train_data_ALL, y=data_responses, family="binomial")Question #4: Is this correct? Do I indeed fit one single model on ALL of my training data?

Then, I'd simply using this model to predict on my testing set, using some code like this:

finals_preds <- predict(final_model, newx=test_data_ALL, type="response", lambda=?)In my nested cross-validation employed in steps 1 through 5, I've obtained a list of 5 values of lambda and 5 corresponding AUC values.

Question #5: Which value of lambda do I choose? Do I select the value of lambda that gave the highest AUC? Do I average the k = 5 values of lambda, and then plug this average into the above line of code for lambda = ?.

Question #6: In the end, I just want one LASSO logistic regression model, with one unique value for each hyper-parameter ... correct?

Question #7: If the answer to Question #5 is yes, how do we obtain an estimate for the AUC value that this model will produce? Is this estimate equivalent to the average of the k = 5 AUC values obtain in Step 5?