Your model can be written as arima model, or to be precise MA(2) model:

$$y_t= z_t+\alpha_1 z_{t-1}+\alpha_2 z_{t-2},$$

ARIMA models are usualy postulated with coefficient $1$ for $z_t$, because you can always move the multiplicative constant to the variance of the disturbances.

So your model

$$y_t= \theta_0x_t+\theta_1 x_{t-1}+(1-\theta_0-\theta_1) x_{t-2}$$

becomes MA(2) model

$$y_t= z_t+\frac{\theta_1}{\theta_0} z_{t-1}+\frac{1-\theta_0-\theta_1}{\theta_0} z_{t-2}$$

with $z_t=\theta_0x_t$.

So you can estimate MA(2) model and then recover $\theta_0$ and $\theta_1$ from $\alpha_1$ and $\alpha_2$:

$$\theta_0=\frac{1}{1+\alpha_1+\alpha_2},\quad \theta_1=\frac{\alpha_1}{1+\alpha_1+\alpha_2}$$

Here is the example in R:

set.seed(1001)

x<-rnorm(10000)

y<-filter(x,c(0.5,0.3,0.2),sides=1)

mod<-arima(y,order=c(0,0,2),include.mean=FALSE)

> mod

Call:

arima(x = y, order = c(0, 0, 2), include.mean = FALSE)

Coefficients:

ma1 ma2

0.6060 0.3874

s.e. 0.0093 0.0093

sigma^2 estimated as 0.2495: log likelihood = -7246.14, aic = 14498.28

> cf <- coef(mod)

> 1/(1+sum(cf))

[1] 0.500497

> cf[1]/(1+sum(cf))

ma1

0.3007687

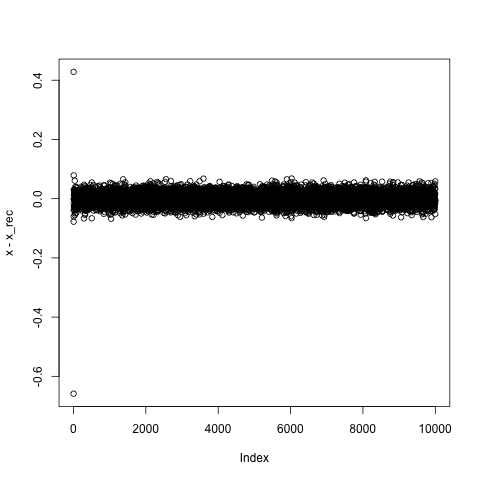

You can recover $x_t$ as residuals of the arima model:

x_rec<- as.numeric(residuals(mod)*(1+sum(cf)))

plot(x-x_rec)

As you see the procedure recovered coefficients with the precision of 3 decimal places. The recovered $x_t$ is also recovered to similar precision. The difference is the initialisation. ARIMA model assumes that the process is infinite, but the data is never infinite, so each estimation procedure must assume some initialisation. As evidenced from the plot the first few elements of recovered $x_t$ have the biggest error, but then the error stabilizes.

Since ARIMA models are estimated via Kalman filter procedure, you could implement it yourself with the proper intialisation. Note that in this example I used quite a big sample of 10000 elements. Less data would result in worse precision, you should run some tests to see the extent of the impact of sample size to the precision of recovery.