Can somebody please provide a simple (lay person) explanation of the relationship between Pareto distributions and the Central Limit Theorem (e.g. does it apply? Why/ why not?)? I am trying to understand the following statement:

$\begingroup$

$\endgroup$

$\endgroup$

Add a comment

|

3 Answers

$\begingroup$

$\endgroup$

5

The statement is not true in general -- the Pareto distribution does have a finite mean if its shape parameter ($\alpha$ at the link) is greater than 1.

When both the mean and the variance are finite ($\alpha>2$), the usual forms of the central limit theorem - e.g. classical, Lyapunov, Lindeberg will apply

See the description of the classical central limit theorem here

The quote is kind of weird, because the central limit theorem (in any of the mentioned forms) doesn't apply to the sample mean itself, but to a standardized mean (and if we try to apply it to something whose mean and variance are not finite we'd need to very carefully explain what we're actually talking about, since the numerator and denominator involve things which don't have finite limits).

Nevertheless (in spite of not quite being correctly expressed for talking about central limit theorems) it does have something of an underlying point -- if the shape parameter is small enough, the sample mean won't converge to the population mean (the weak law of large numbers doesn't hold, since the integral defining the mean is not finite).

As kjetil rightly points out in comments, if we're to avoid the rate of convergence being terrible (i.e. to be able to use it in practice), we need some kind of bound on "how far way"/"how quickly" the approximation kicks in. It's no use having an adequate approximation for $n> 10^{10^{100}}$ (say) if we want some practical use from a normal approximation.

The central limit theorem is about the destination but tells us nothing about how fast we get there; there are, however, results like the Berry-Esseen theorem theorem which do bound the rate (in a particular sense). In the case of Berry-Esseen, it bounds the largest distance between distribution function of the standardized mean and the standard normal cdf in terms of the third absolute moment, $E(|X|^3)$.

So in the case of the Pareto, if $\alpha\gt 3$, we can at least get some bound on just how bad the approximation might be at some $n$, and how quickly we're getting there. (On the other hand, bounding the difference in cdfs isn't necessarily an especially "practical" thing to bound -- what you're interested may not relate especially well to a bound on the difference in tail area). Nevertheless, it is something (and in at least some situations a cdf bound is more directly useful).

-

3$\begingroup$ But if the variance just barely exists, that is $\alpha > 2$ but very close, the central limit theorem, while applying in principle, may lead to very bad approximations. To have some control over the quality of approximation you need something like the Berry-Esseen theorem, which requires third moments, that is, $\alpha > 3$. $\endgroup$ Commented Jan 27, 2016 at 10:01

-

1$\begingroup$ @kjetil quite so; in practice you need more than just second moments because convergence can be uselessly slow. $\endgroup$– Glen_bCommented Jan 27, 2016 at 10:28

-

2$\begingroup$ Some distributions that do not follow the central limit theorem can be standardized to converge to a stable law. $\endgroup$ Commented Apr 23, 2017 at 16:49

-

$\begingroup$ Great discussion here. Wish stackexchange had a way to follow people's answers/comments ;) $\endgroup$ Commented Jun 15, 2019 at 19:07

-

1$\begingroup$ Better on meta, but here goes: While Stackexchange isn't a social media site (it's designed around Q&A, not people; e.g. you can follow a question), there's a few things you can do. 1. If there's a user whose answers or comments are of interest to you, you can go to their profile page, get on the Activity tab (and sort the answers section by "Newest" perhaps). For comments, see their 'All actions' tab. 2. There's an RSS feed for every user, at the bottom of that same page. 3. There are some apps for doing this kind of thing -- e.g. see here $\endgroup$– Glen_bCommented Jun 16, 2019 at 0:52

$\begingroup$

$\endgroup$

5

I will add an answer showing how bad the approximation from the central limit theorem (CLT) can be for the Pareto distribution, even in a case where the assumptions for CLT is fulfilled. The assumption is that there must be a finite variance, which for the Pareto means that $\alpha > 2$. For a more theoretical discussion of why this is so, see my answer here: What is the difference between finite and infinite variance

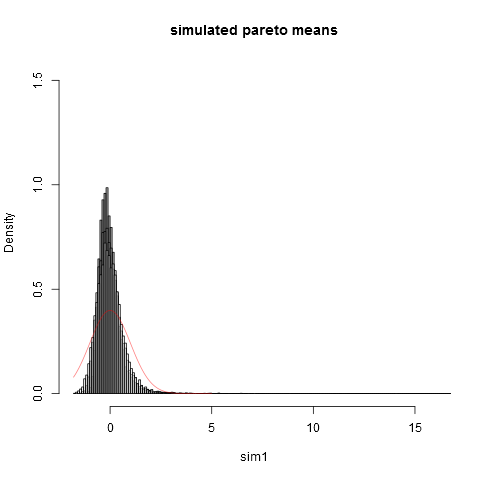

I will simulate data from the Pareto distribution with parameter $\alpha=2.1$, so that the variance "just barely exists". Redo my simulations with $\alpha=3.1$ to see the difference! Here is some R code:

### Pareto dist and the central limit theorem

###

require(actuar) # for (dpqr)pareto1()

require(MASS) # for Scott()

require(scales) # for alpha()

# We use (dpqr)pareto1(x,alpha,1)

#

alpha <- 2.1 # variance just barely exist

E <- function(alpha) ifelse(alpha <= 1,Inf,alpha/(alpha-1))

VAR <- function(alpha) ifelse(alpha <= 2, Inf,

alpha/((alpha-1)^2 * (alpha-2)))

R <- 10000

e <- E(alpha)

sigma <- sqrt(VAR(alpha))

sim <- function(n) {

replicate(R, {x <- rpareto1(n,alpha,1)

x <- x-e

mean(x)*sqrt(n)/sigma },simplify=TRUE)

}

sim1 <- sim(10)

sim2 <- sim(100)

sim3 <- sim(1000)

sim4 <- sim(10000) # do take some time ...

### These are standardized so have all

### theoretically variance 1.

### But due to the long tail, the empirical variances are

### (surprisingly!) much lower:

sd(sim1)

sd(sim2)

sd(sim3)

sd(sim4)

### Now we plot the histograms:

hist(sim1, prob=TRUE, breaks="Scott", col=alpha("grey05",

0.95), main="simulated Pareto means", xlim=c(-1.8,16))

hist(sim2, prob=TRUE, breaks="Scott", col=alpha("grey30",

0.5), add=TRUE)

hist(sim3, prob=TRUE, breaks="Scott", col=alpha("grey60",

0.5), add=TRUE)

hist(sim4, prob=TRUE, breaks="Scott", col=alpha("grey90",

0.5), add=TRUE)

plot(dnorm, from=-1.8, to=5, col=alpha("red", 0.5), add=TRUE)

And here is the plot:

One can see that even at sample size $n=10000$ we are far away from the normal approximation. That the empirical variances are so much lower than the true theoretical variance $\sigma^2=1$ is due to the fact that we have a very large contribution to the variance from parts of the distribution in the extreme right tail that do not show up in most samples. This is to be expected always, when the variance "just barely exists". A practical way to think about that is the following. Pareto distributions is often proposed to model distributions of income (or wealth). The expectation of income (or wealth) will have a very large contribution from the very few billionaires. Sampling with practical sample sizes will have a very small probability of including any billionaires in the sample!

answered Jan 27, 2016 at 12:49

-

1$\begingroup$ In the example, the convergence is mostly bad/slow due to the standard deviation being so large due to some large values of which there are only a few (these large values in the tails say little about the shape of the density in the middle). When you scale the distribution based on something like the interquartile range then the convergence is faster. $\endgroup$ Commented Nov 21, 2021 at 13:33

-

$\begingroup$ @SextusEmpiricus: Not so, the standardization in the simulation uses the theoretical mean and standard deviation, not estimates! $\endgroup$ Commented Sep 7, 2023 at 0:00

-

$\begingroup$ Whether you use the theoretical values or the estimated values is not relevant, the point is that using the standard deviation (no matter what way) is problematic. If you use the CLT with a different scaling* then the CLT approximation is much better and the error mostly occurs for a fraction of a percent of the tails. The shape of the approximation is good for the central portion, but it is the scale that doesn't match. $$^*\text{for example:}\quad \frac{\bar{X} - \mu}{a_n} \\ \text{with $a_n$ something different than $\sqrt{n} \sigma$}$$ $\endgroup$ Commented Sep 7, 2023 at 6:23

-

$\begingroup$ So what I meant is: “The histogram in your figure still very much resembles a normal distribution”. It's just that it has long tales which mess up the scale (and these tails are not always sampled as your emperical sd's show) and that is why it doesn't match with the CLT approximation. (The problem is not the error in the SD estimates. Your observed sd estimate is so low because sampling from the heavy tails is very unlikely, but if you would have a sample that happens to match the SD=1, e.g. large R, then you would still not get a good match between the approximated curve and the histogram) $\endgroup$ Commented Sep 7, 2023 at 7:00

-

$\begingroup$ @SextusEmpiricus: Thanks, I will add to the answer $\endgroup$ Commented Sep 7, 2023 at 11:37

$\begingroup$

$\endgroup$

I like already given answers but think they are bit too technical for a "lay person explanation" so I will try something more intuitive (starting by an equation ...).

The mean of density $p$ is defined as: $$ \mu = \int x \cdot p(x) dx $$ So grossly speaking, the mean is the "sum over $x$" of the product between the density at $x$ and $x$ itself. When $x$ tends to infinity the density at $p(x)$ must vanish sufficiently so that the product $x \cdot p(x)$ does not go to infinity (and as a result the sum also). When $p(x)$ does not vanish sufficiently, the product goes to infinity, the integral goes to infinity, $\mu$ does not exist and, finally, $p$ has no mean. This is the case of Pareto for certain parameter values.

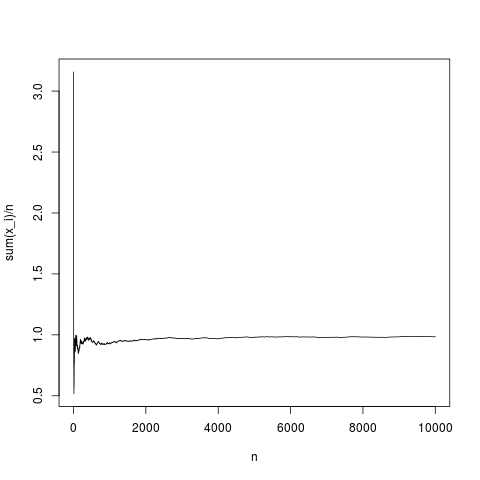

Then, the central limit theorem establishes a distribution of the distance between the empirical mean $\bar{x}=\frac{1}{n} \sum_i x_i$ and the mean $\mu$ as a function of the variance of $p$ and $n$ (asymptotically with $n$). Let see how the empirical mean $\bar{x}$ behaves as a function of the number of $n$ for a Gaussian density $p$:

N=10000;

x=rnorm(N,1,1);

y=rep(NA,N);

for(index in seq(1,N))

{

y[index]=mean(x[1:index])

}

png('~/Desktop/normalMean.png')

plot(y,type='l',xlab='n',ylab='sum(x_i)/n')

dev.off()

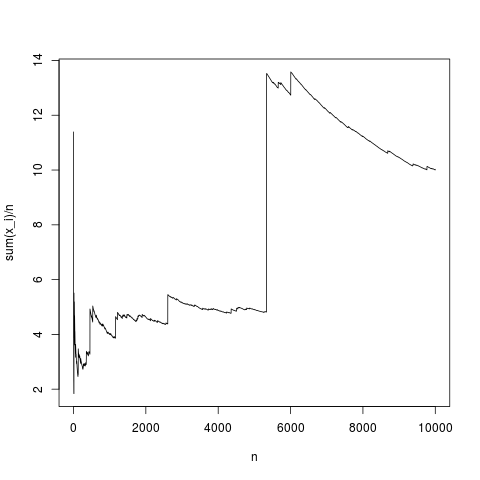

This is a typical realization, the sample mean converges to the density mean quite properly (and in average in the way given by the central limit theorem). Let do the same for a pareto distribution with no mean (substituing rnorm(N,1,1); by pareto(N,1.1,1);)

This is a also a typical simulation, time to time, the sample mean deviates strongly simply because as explained using the integral formula, in the product $p(x) \cdot x$, the frequency of high values of $x$ is no small enough to compensate the fact that $x$ is high. So mean does not exists and the sample mean does not converge to any typical value and the central limit theorem has nothing to say.

Finally, notice that the central limit theorem relates empirical mean, mean, sample size $n$ and variance. So variance $\int (x-\mu)^2 p(x) dx$ must also exists (see kjetil b halvorsen answer for details).