You want to study the correlation between self-harm and aggression, but thinks that this might be dependent upon depressive symptoms. One could possibly construct a model for conditional correlation, but I would rather start with some visualization of the data (if you can post a link to data I can include one here).

You have only 170 patients, so the obvious idea of stratification (on depressive symptoms) is difficult to apply. But an extension of that idea to local correlation is possible, effectively using overlapping strata (via weights, as in local regression).

But I would start with visualization: a conditioning plot. There is an R function for that, coplot, and an example of use can be seen here: How do I create and interpret an interaction plot in ggplot2?

(the solution you propose yourself in the last paragraph do not give meaning: You cannot estimate the correlation for each patient (that makes $n=1$), but to estimate a local correlation is an extension/bettering of that idea. It is a variant on the idea of local regression)

I will simulate some data, a bivariate random vector $(X,Y)$ which is bivariate normal, but with a correlation which depends on a third variable $Z$. Such a random vector $(X,Y,Z)$ cannot have a multivariate normal distribution, because then the conditional correlation will be constant. This can be seen using formulas in https://en.wikipedia.org/wiki/Multivariate_normal_distribution#Conditional_distributions.

We need some (inverse) link function mapping an unrestricted variable $z$ to the interval $(-1, 1)$ of possible correlation values. I will use

$$ \rho(z) = \frac{e^z-1}{e^z+1}$$(another possibility is Fisher's z transform). Then $Z$ will be standard normal, and $(X,Y) | Z=z$ will be binormal with zero expectation, and covariance matrix $\left(\begin{smallmatrix} 1&\rho(z) \\ \rho(z)&1 \end{smallmatrix}\right)$. Some code for the simulation (R):

library(MASS)

set.seed(7*11*13) # my public seed

n <- 1000

z <- rnorm(n) # standard normal

rho <- function(z) (exp(z)-1)/(exp(z)+1) #inverse link function for correlation

Sigma <- function(z) matrix( c(1.0, rho(z), rho(z), 1.0), 2, 2)

xy <- matrix( rep(0.0, 2*n), n,2 )

for (i in 1:n) {xy[i,] <- MASS::mvrnorm(1, mu=rep(0.0,2), Sigma(z[i]))}

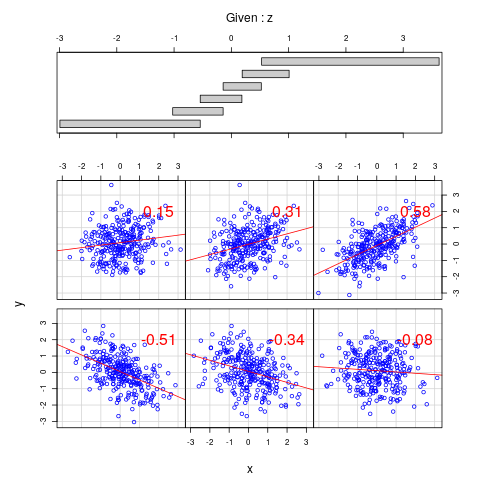

We can show this as a conditioning plot:

The plot should be read starting from the bottom left (order of increasing $z$). Overplotted is a regression line and the Pearson correlation in red. Code for the plot:

mypanel <- function(x, y, ...) { r <- cor(x,y) ; points(x,y, ...) ; abline(lm(y ~ x), col="red") ; graphics::text(2.0, 2.0, label=round(r,2), col="red", cex=2.0) }

coplot(xy[,2] ~ xy[,1] | z , col="blue", panel=mypanel, xlab="x", ylab="y")

We can show with a hypothesis test that the data is not multinormal:

library(MVN) # (on CRAN)

xyz <- data.frame(x=xy[,1], y=xy[,2], z=z)

> MVN::mvn(xyz, mvnTest="energy", univariateTest="SW", univariatePlot="qq", multivariatePlot="qq")

$multivariateNormality

Test Statistic p value MVN

1 E-statistic 2.884006 0 NO

$univariateNormality

Test Variable Statistic p value Normality

1 Shapiro-Wilk x 0.9987 0.6646 YES

2 Shapiro-Wilk y 0.9986 0.6357 YES

3 Shapiro-Wilk z 0.9979 0.2621 YES

(plots not shown).

As a continuation, we could ask if we can formulate a statistical model to estimate a conditional correlation. I have only found explicit references to such ideas in the context of time series, see Dynamic Conditional Correlation (DCC) model yields unexpected sign of fitted correlations. But it is possible to define a model similar to generalized linear models. This is implemented in the R package VGAM (on CRAN), with the family function binormal(). But so far I didn't try it, and will not give examples here. (VGAM can still give the feeling of an experimental, very ambitious project).