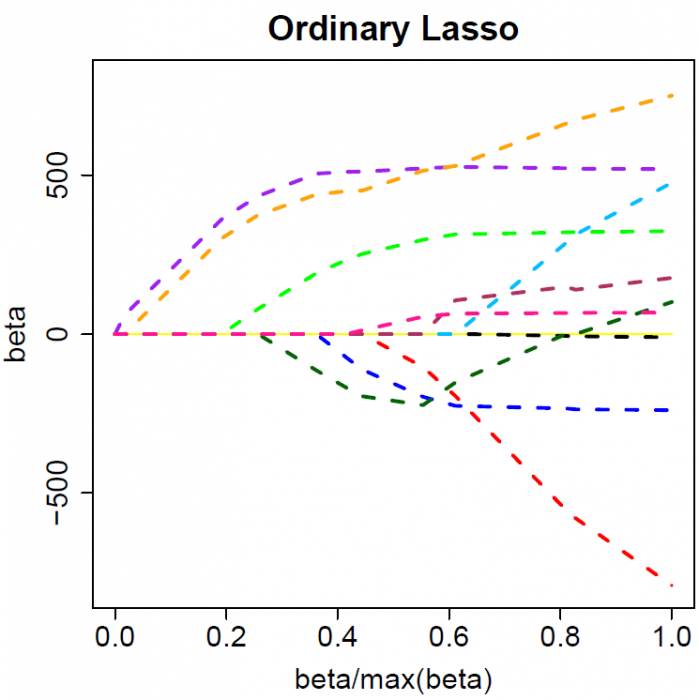

I'm looking at this example for LASSO regression in R: http://machinelearningmastery.com/penalized-regression-in-r/.

It mentions "step size" and "best_step". And, the documentation here also mentions this idea of a "step".

I have never heard of a step size being applied to LASSO regression. Can someone please help me understand where this is coming from?