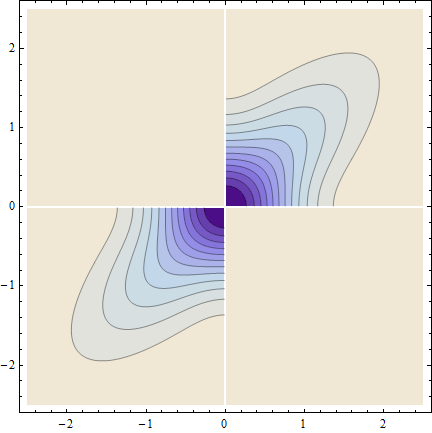

I am not sure in the terminology, so I will simply try to explain the situation that I would like to model as I see it. Suppose there is a set of random variables. The variables are correlated in such a way that they deviate from their expected values into the same direction all together. By this I mean that they can be either all together larger then their expectation or all together lower. Is it possible to model such a dependency with a multivariate normal random variable $\mathbf{X} \sim \mathcal{N}(\mathbf{\mu}, \mathbf{\Sigma})$, assuming the knowledge about the marginal distributions of the components $\mathbf{X}_i \sim \mathcal{N}(\mu_i, \sigma^2_i)$? How to construct $\mathbf{\Sigma}$ is this situation? Thank you.

Best wishes, Ivan