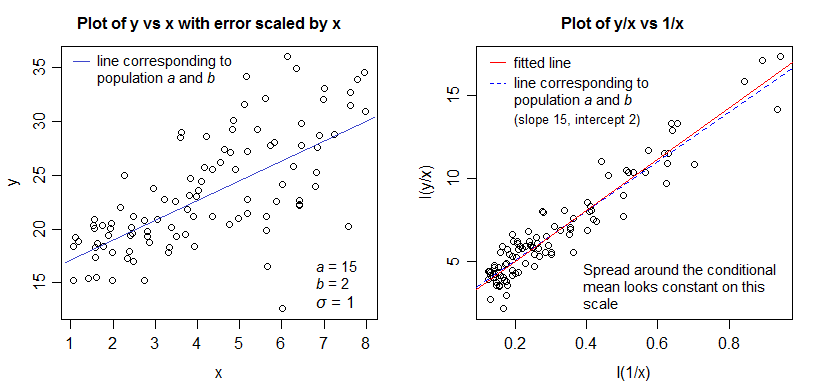

I want to estimate this model $$ y_t = a + b x_t + \sigma x_t\epsilon_t $$ where we have an error with heteroskedasticity (it depends on $x_t$).

Suppose I estimate this model with OLS so, assuming that the error is homoskedastic. In particular, I'am assuming that the model is

$$

y_t = a + b x_t + \epsilon_t

$$

with $\epsilon_t$ ~ $N(0,\eta^2)$. I get $\hat{a}, \hat{b}$ and a set of residuals $\hat{\epsilon}_t$.

Now I want to estimate $\sigma$. I can set up another regression $$ \log(\epsilon_t) = \log(\sigma)+\log(x_t)+\epsilon_t. $$ But it seems to me that there is an inconsistency in doing this. How can I do this correctly?