Here is an example: suppose $X_1,X_2,\cdots, X_n$ are iid samples from $\mathcal N(\mu,\sigma^2)$, where you do not know $\mu,\sigma^2$ and you want to estimate them. The natural estimator of $\mu$ is $\hat \mu=\bar X= \frac1n \sum X_i$.

It is less immediately obvious what to use to estimate $\sigma^2$ but you might expect to use some fraction of $\sum(X_i-\bar X)^2$, which has mean $(n-1)\sigma^2$ and variance $2(n-1)\sigma^4$, so $\frac1k\sum(X_i-\bar X)^2$ has mean $\frac{n-1}{k}\sigma^2$ and variance $\frac{2(n-1)}{k^2}\sigma^4$. Not using a fraction of $\sum(X_i-\bar X)^2$ might lead to some of the inefficiencies in the "silly estimates" in your question.

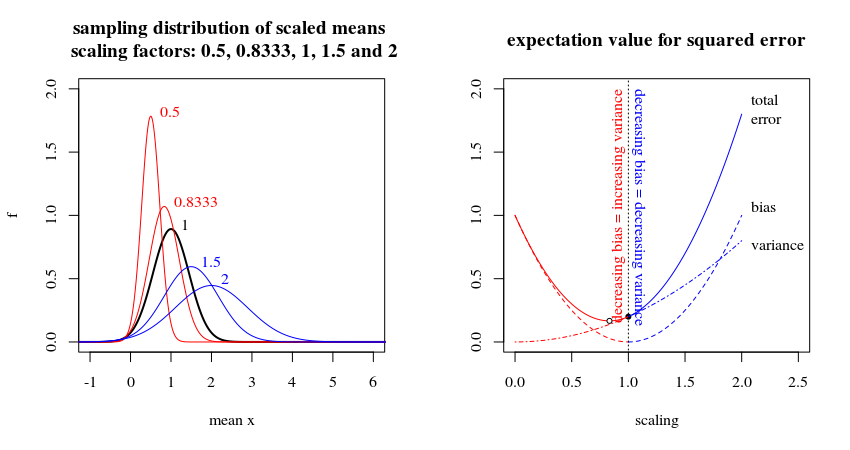

This means that (the square of) the bias increases as $k$ moves away from $n-1$, while the variance reduces as $k$ increases. Reducing $k$ below $n-1$ tends to increase both so it is presumably unwise, but increasing $k$ above $n-1$ leads to a tradeoff with the square of the bias increasing and the variance reducing.

Here is an chart, with the square of the bias in red, the variance in blue and the expected mean-square-error in black (it uses $n=6$ but this makes little difference). This illustrates:

the unbiased estimator $\frac1{n-1}\sum(X_i-\bar X)^2$ has expected mean-square-error of $\frac{2}{n-1}\sigma^4$; lower values of $k$ perform worse

the maximum likelihood estimator $\frac1{n}\sum(X_i-\bar X)^2$ has expected mean-square-error of $\frac{2n-1}{n^2}\sigma^4$, which is smaller despite a biased estimator

expected mean-square-error is minimised with $k=n+1$ i.e. with $\frac1{n+1}\sum(X_i-\bar X)^2$ when it is $\frac{2}{n+1}\sigma^4$, while for higher values of $k$ the smaller variance fails to offset the larger square of the bias.