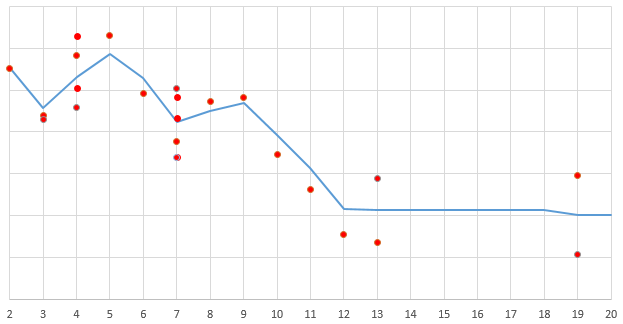

Every day $t$ we observe several (independent) realizations of a variable $X_t$. This variable is the sum of a time dependent mean value and white noise:

$$X_t=\mu_t+\epsilon_t$$

You can assume $\epsilon_t$ has a fixed variance over time, is Gaussian and independent of everything. The underlying time series $\mu_t$ could be forecasted with usual time-series methods.

But $\mu_t$ is not directly observable. Instead we observe:

- $a_t$ the average observed value for $X_t$ over day $t$

- $n_t$ the number of observations for this day

The number $n_t$ can vary very much. The goal is not to forecast it but to take it into account to forecast $\mu_t$. Typically, when $n_t$ is small, we observe a noisy average. When $n_t$ is big, $a_t$ is very close to $\mu_t$ (the standard deviation of $a_t-\mu_t$ is $\frac{\sigma}{\sqrt n_t}$)

Do you know/think of a way to take $n_t$ into account when using forecasting methods? (Possibly very simple ones: assuming $\mu_t$ is just a random walk)