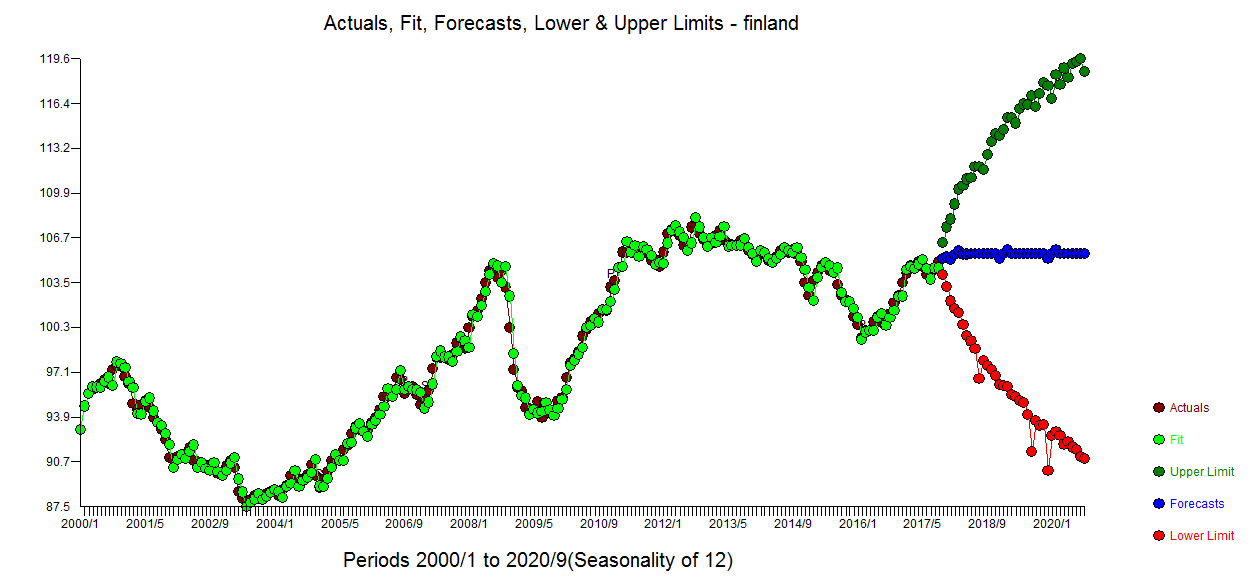

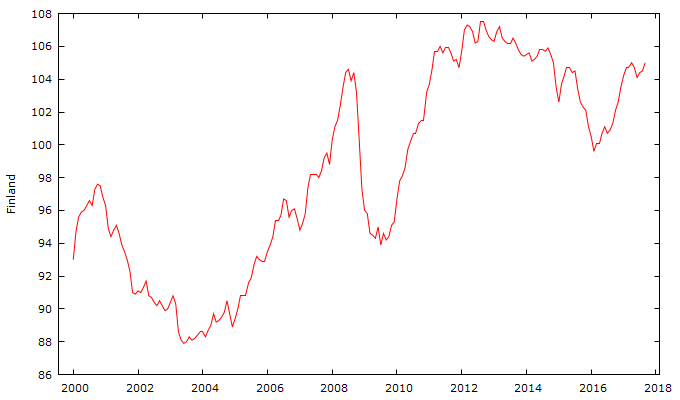

I'm studying methods for time series analysis, using gretl. I have this time series.

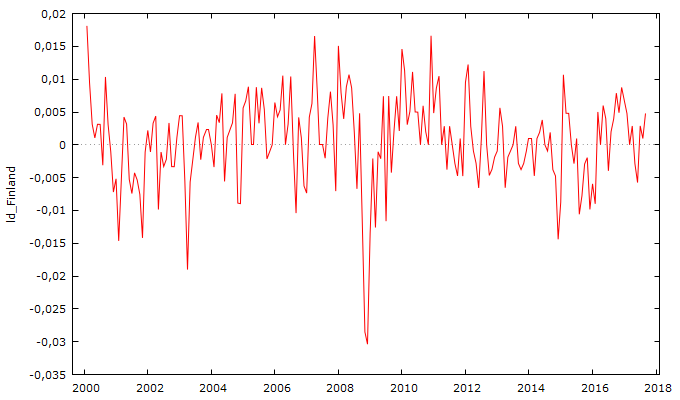

I used TRAMO and X12-ARIMA to detect probable outlier, but I found nothing. So I used difference-log of first order to make the serie stationary, and I had this:

I used TRAMO and X12-ARIMA to detect probable outlier, but I found nothing. So I used difference-log of first order to make the serie stationary, and I had this:

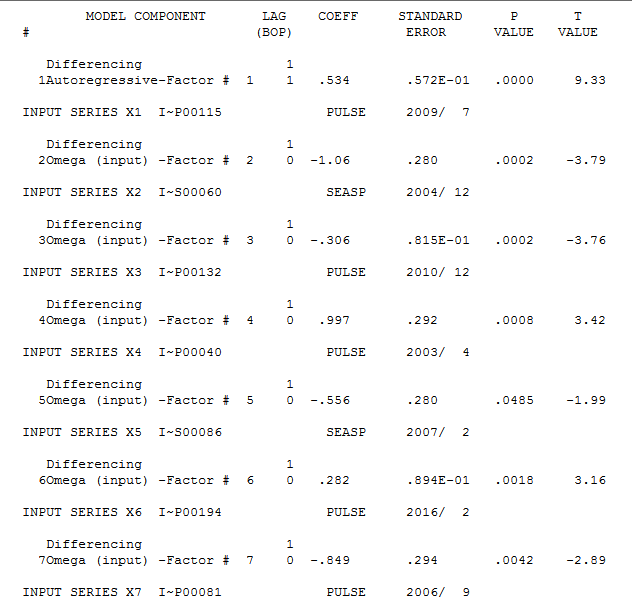

It seems that there is something in the end of 2008. Infact TRAMO found a temporary change on November 2008

It seems that there is something in the end of 2008. Infact TRAMO found a temporary change on November 2008

106 TC (11 2008)

First question: Is it possible that the series before being differentiated had no outlier and after yes?

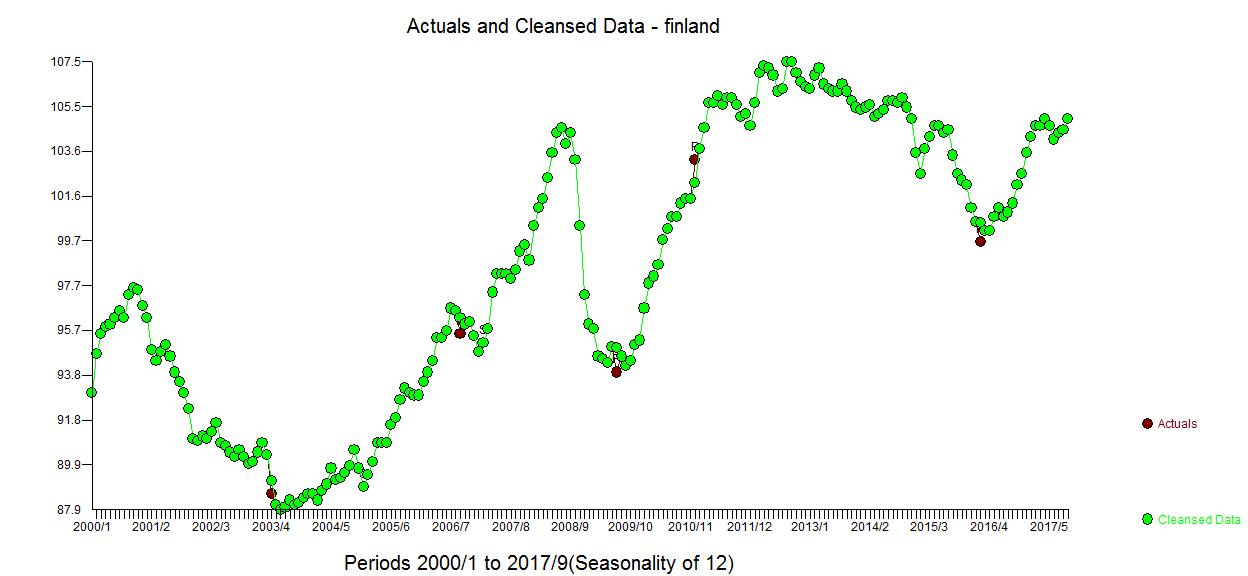

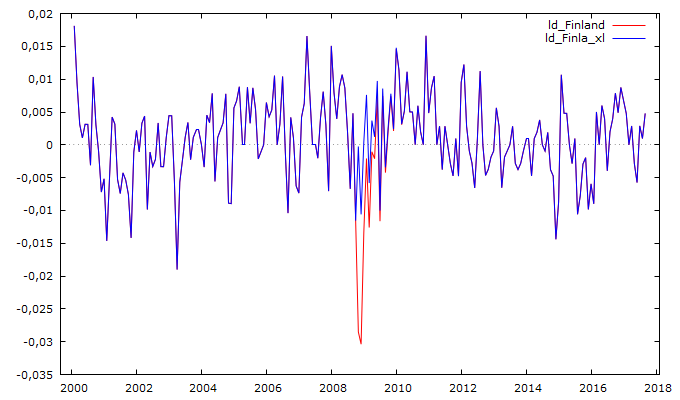

I continued the analysis, linearizing the serie, obtaining

So I can begin to study the ACF and PACF

So I can begin to study the ACF and PACF

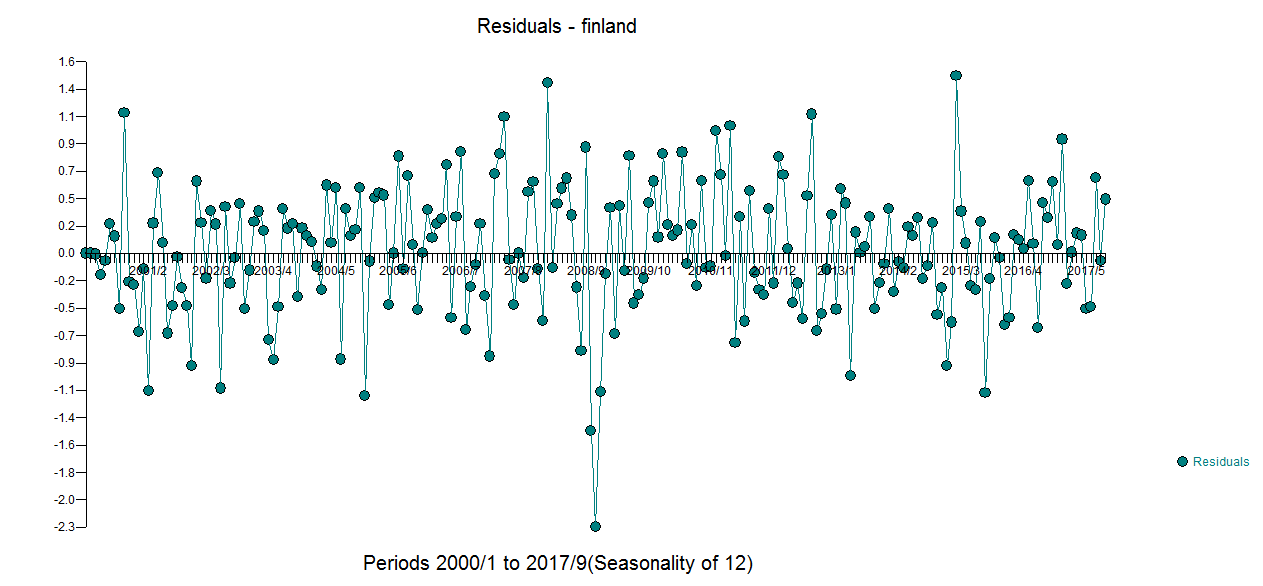

TRAMO suggested me to use ARIMA(1,0,0)(0,1,1), but I found that a simple AR(1) give the same result. These are the ACF-PACF of ARIMA(1,0,0)(0,1,1) residuals:

TRAMO suggested me to use ARIMA(1,0,0)(0,1,1), but I found that a simple AR(1) give the same result. These are the ACF-PACF of ARIMA(1,0,0)(0,1,1) residuals:

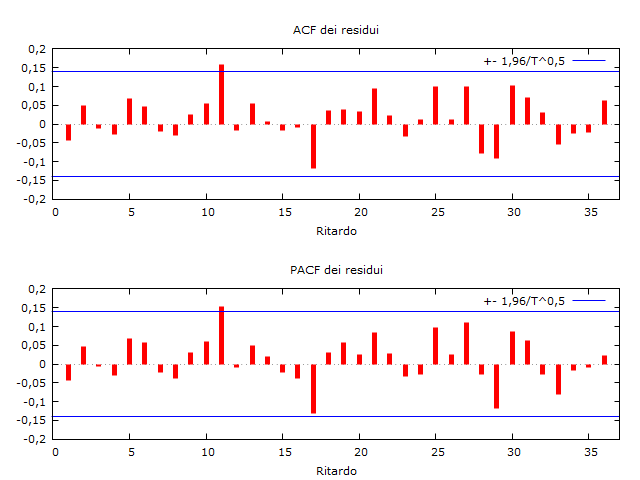

and these of AR(1) residuals

and these of AR(1) residuals

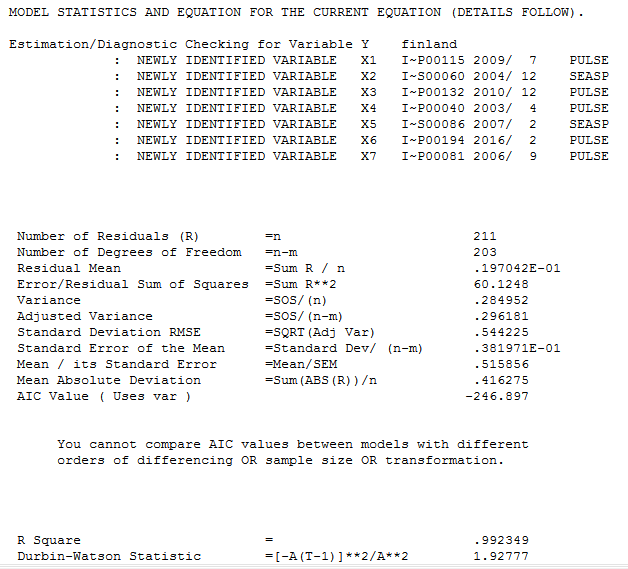

Comparing AIC and BIC, theory suggests to choose the AR(1). This is the output for the ARIMA

Comparing AIC and BIC, theory suggests to choose the AR(1). This is the output for the ARIMA

Modello 3: ARIMA, usando le osservazioni 2001:03-2017:09 (T = 199)

Stimato usando il metodo BHHH (MV condizionale)

Variabile dipendente: (1-Ls) ld_Finla_xl

coefficiente errore std. z p-value

------------------------------------------------------------

const 7,67509e-05 0,000137004 0,5602 0,5753

phi_1 0,307572 0,0671470 4,581 4,64e-06 ***

Theta_1 −0,765016 0,0511360 −14,96 1,33e-050 ***

Media var. dipendente 0,000170 SQM var. dipendente 0,008292

Media innovazioni 0,000046 SQM innovazioni 0,006505

Log-verosimiglianza 719,6341 Criterio di Akaike −1431,268

Criterio di Schwarz −1418,095 Hannan-Quinn −1425,937

Note: SQM = scarto quadratico medio; E.S. = errore standard

Reale Immaginario Modulo Frequenza

-----------------------------------------------------------

AR

Radice 1 3,2513 0,0000 3,2513 0,0000

MA (stagionale)

Radice 1 1,3072 0,0000 1,3072 0,0000

-----------------------------------------------------------

this for the AR model

Modello 1: ARMA, usando le osservazioni 2000:03-2017:09 (T = 211)

Stimato usando i minimi quadrati (MV condizionale)

Variabile dipendente: ld_Finla_xl

coefficiente errore std. z p-value

--------------------------------------------------------

const 0,000623196 0,000402829 1,547 0,1219

phi_1 0,312608 0,0644261 4,852 1,22e-06 ***

Media var. dipendente 0,000935 SQM var. dipendente 0,006078

Media innovazioni 0,000000 SQM innovazioni 0,005776

Log-verosimiglianza 789,1005 Criterio di Akaike −1574,201

Criterio di Schwarz −1567,497 Hannan-Quinn −1571,491

Note: SQM = scarto quadratico medio; E.S. = errore standard

Reale Immaginario Modulo Frequenza

-----------------------------------------------------------

AR

Radice 1 3,1989 0,0000 3,1989 0,0000

-----------------------------------------------------------

Second question: TRAMO suggests to use seasonale difference, but from the ACF/PACF it seems that it's not necessary. I know that seasonal difference is requested when there is no stationary caused by the seasonal component. Is it true?