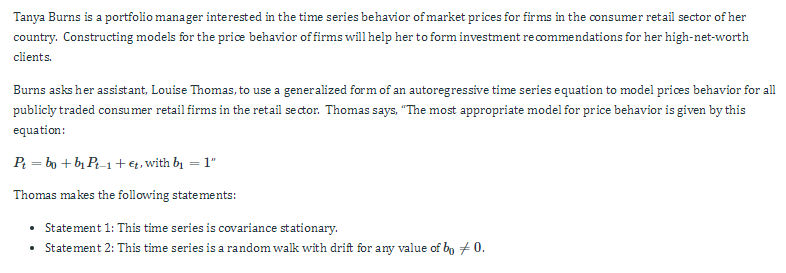

I don't know how to determine the truth of the following statements regarding this time series model. I know a covariance stationary time-series has properties that don't change over time, but I don't know how to find out if that's true. I also don't know how to determine if a particular series is a random walk with or without a drift.