I am learning so bear with me.

Aim: I am trying to figure out if my data fit the criteria for multiple linear regression.

Context: My model has two numeric and four categoric variables.

kiva_model <- lm(lender_count ~

loan_usd+ #Numeric

sector+ #Categoric 11 levels

term_in_months+ #Numeric

borrower_genders+ #Categoric 5 levels

repayment_interval+ #Categoric 3 levels

country_code, #Categoric 59 levels

data=kiva_omit)

Sample size is 504,528.

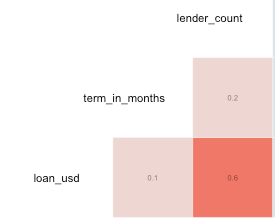

I checked the correlation between the three numeric variables as follows:

loan_usd is a strong predictor or lender_count.

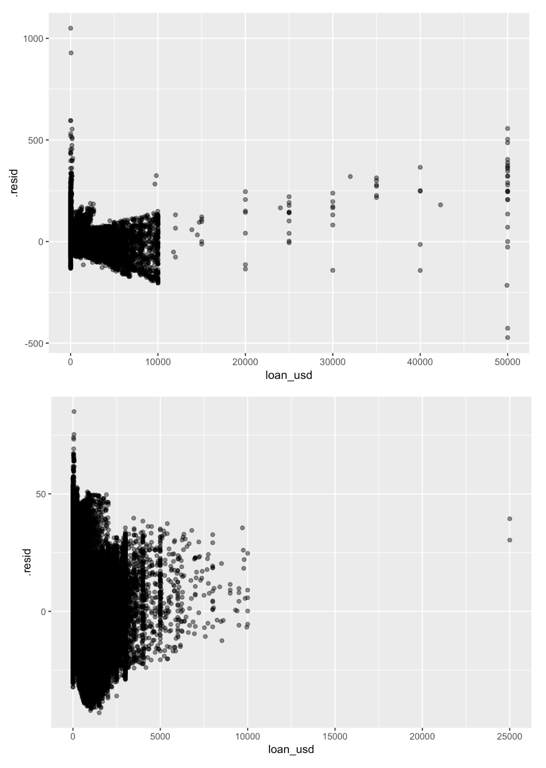

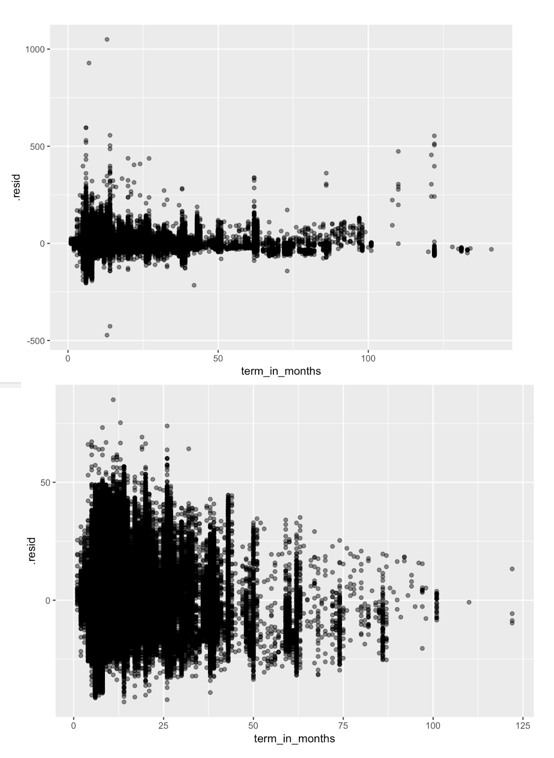

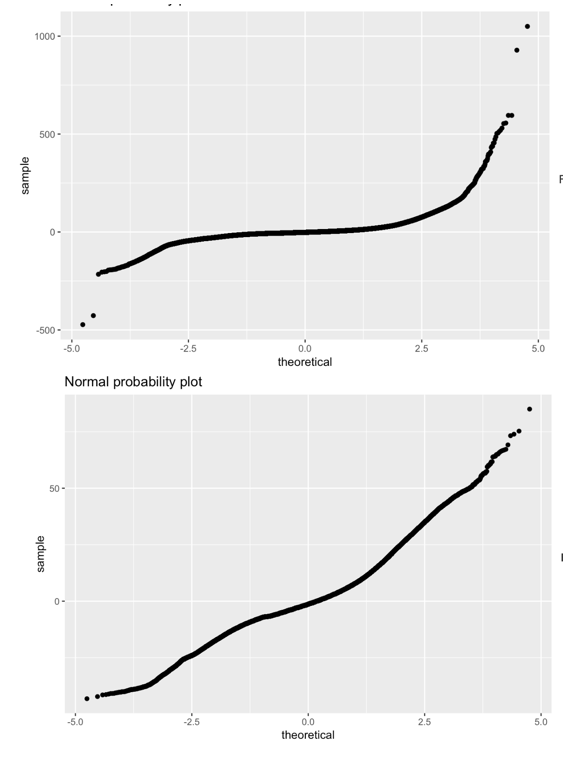

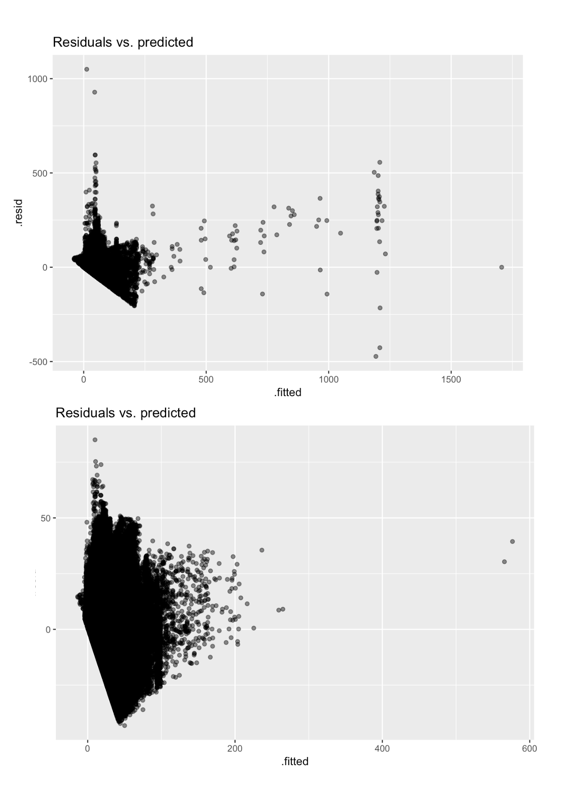

I have made plots to assess: a) Linearity of numerical variables b) nearly normal residuals c) constant variability.

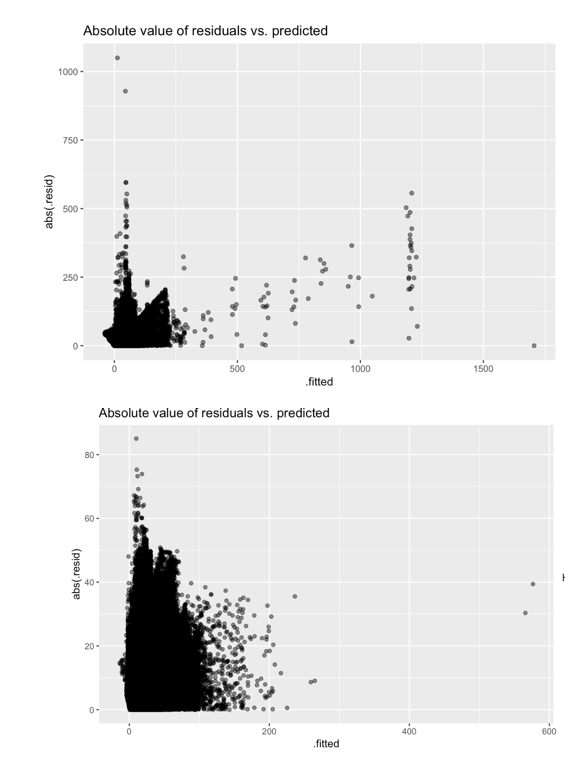

The images show the before (above) and after (below) of outlier removal using cooks_distance<4/n.

I cannot figure out if this is acceptable enough to proceed with my analysis or if I have to further manipulate the data prior the final regression.

To summarise my main concerns:

- Conical shape in

term_in_monthsvs. residuals. - Slight S-shape in Normal probability plot.

- Strong line in Residuals vs. predicted.

a) Linearity of numerical variables

b) Nearly normal residuals

c) Constant variability

Residuals vs. predicted

Absolute value of residuals vs. predicted