Hello stats community,

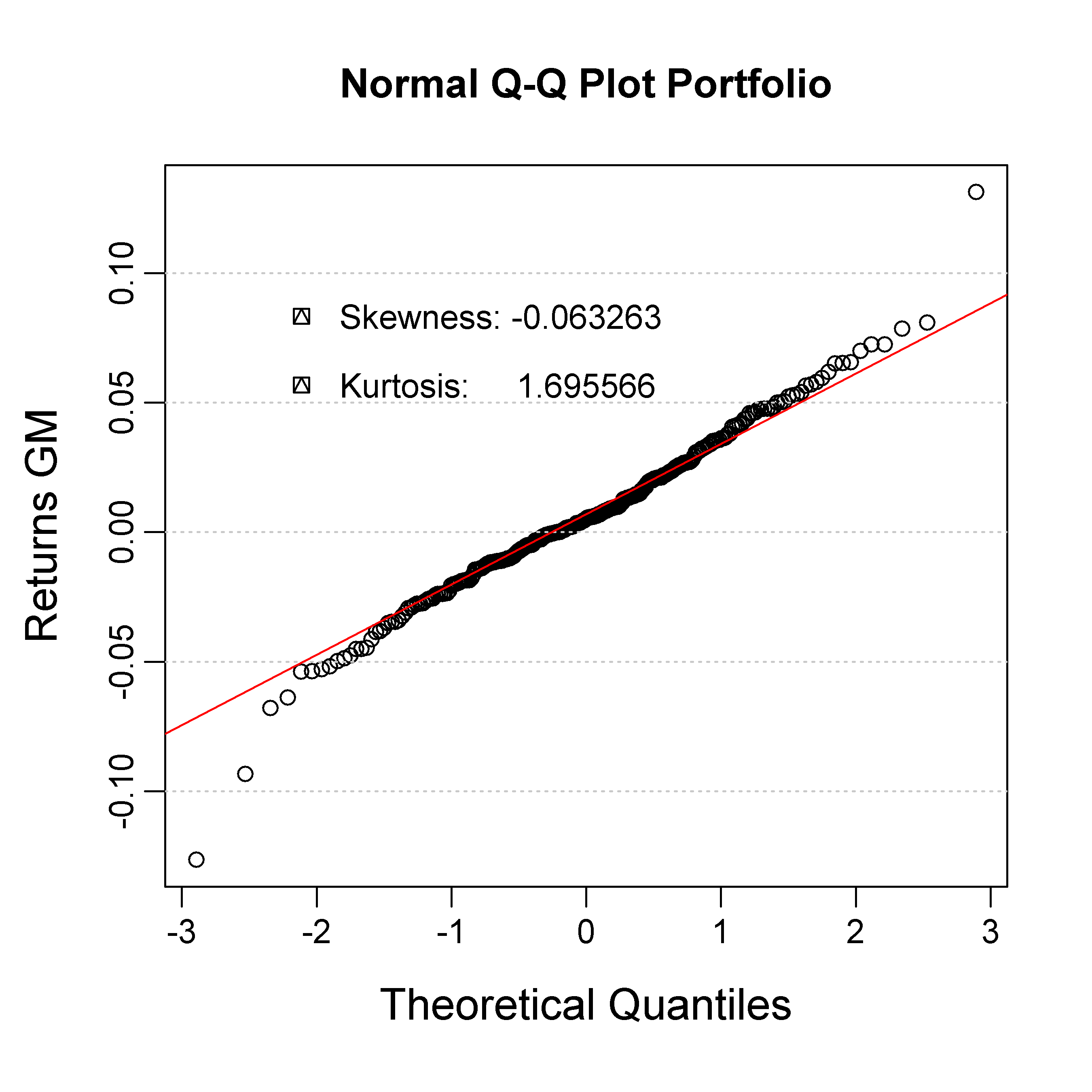

I have a Q-Q plot for my stock returns with a sample of n=262. I drew the plot with qqnorm and qqline(qtype=8). Most of the returns, except for 3 outliers, tend to follow the normal line.

However, when I perform the Shapiro Wilk test, I get a p-value of 0.003197, telling me that I can reject the null-hypothesis that my returns are drawn from a normal distribution.

Test Results:

STATISTIC:

W: 0.983

P VALUE:

0.003197

Am I missing something? Should I follow my observations or trust the SW test?